Close-up of a dental implant with titanium post, abutment, and ceramic crown on a clean medical background with blurred dental office

Dental Implant Cost With Insurance and Without

Content

Content

Missing teeth affect more than just your smile. They impact how you eat, speak, and feel about yourself. Dental implants offer a permanent solution, but the price tag often catches patients off guard. Understanding what you'll actually pay—whether your insurance helps or you're covering everything yourself—makes the difference between moving forward with confidence or putting off treatment indefinitely.

Most people assume their dental coverage will handle implants the same way it covers fillings or crowns. That assumption leads to sticker shock when they discover implants fall into a different category entirely. The reality is more nuanced than a simple yes-or-no answer about coverage.

How Much Does a Dental Implant Cost Without Insurance

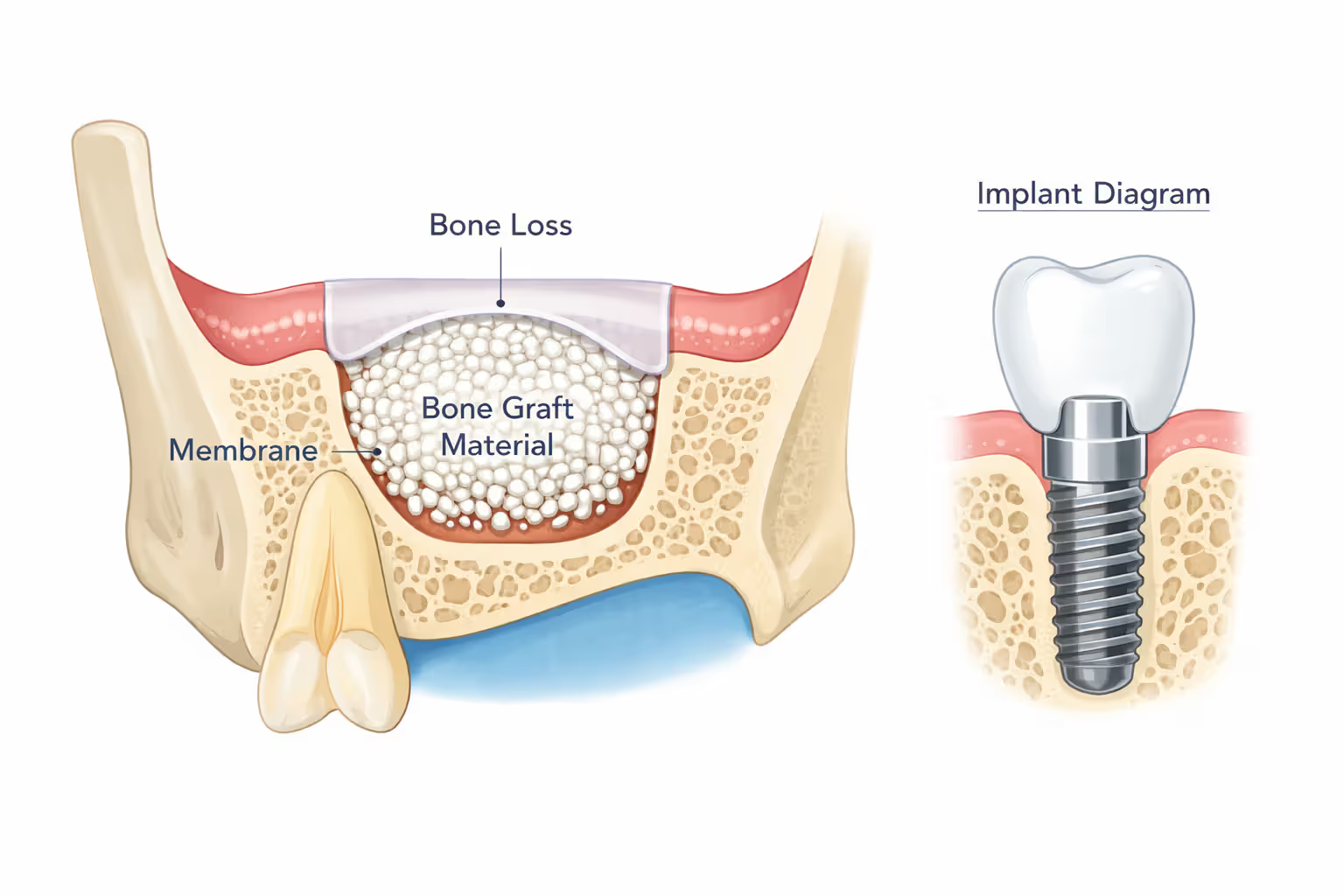

When you pay out of pocket for a dental implant, you're covering several distinct procedures. The total cost breaks down into three main components: the implant post (titanium screw placed in your jawbone), the abutment (connector piece), and the crown (visible tooth replacement). Each piece carries its own price.

A single tooth implant typically runs between $3,500 and $6,500 in most U.S. markets. That range reflects significant regional variation. Urban centers like New York, San Francisco, and Boston push toward the higher end, with some practices charging $7,000 or more. Smaller cities in the Midwest or South often land closer to $3,000 for the complete procedure.

The implant post itself costs $1,500 to $2,500. This surgical component requires precise placement and represents the foundation of your new tooth. The abutment adds another $500 to $1,000, while the crown ranges from $1,500 to $3,000 depending on materials and customization.

Multiple implants create economies of scale in some ways but multiply costs in others. Two separate implants might cost $6,000 to $12,000, but an implant-supported bridge replacing three teeth could run $5,000 to $15,000. Full-arch restoration using four to six implants per jaw ranges from $20,000 to $45,000.

Additional procedures inflate the baseline price. About 60% of implant patients need bone grafting because their jawbone has deteriorated from tooth loss. Bone grafts add $300 to $3,000 depending on the extent of reconstruction needed. Sinus lifts for upper jaw implants cost $1,500 to $3,000. Tooth extractions, if necessary before implant placement, run $150 to $650 per tooth.

Author: Tyler Grant;

Source: ladylesliebelize.com

Geographic location affects pricing beyond just cost of living. States with higher concentrations of dental specialists see more competitive pricing. A patient in Phoenix might pay $4,200 for the same implant that costs $6,800 in Manhattan. Rural areas sometimes charge less but may require travel to specialists, adding hidden costs.

Dentist experience and credentials also influence pricing. A general dentist who places implants occasionally might charge $3,500, while a periodontist or oral surgeon with advanced training and a dedicated implant practice might charge $5,500 for identical materials. You're paying for expertise that reduces complication risks.

How Dental Insurance Covers Implants

Dental insurance treats implants differently than routine procedures because of how benefits are structured. Most plans categorize services into three tiers: preventive (cleanings, exams), basic (fillings, simple extractions), and major (crowns, bridges, dentures). Implants fall into major services when covered at all, but many plans exclude them entirely.

The fundamental issue is how insurers classify implants. Traditional dental insurance was designed decades ago when implants were experimental. Many policies still label them as cosmetic or elective procedures, similar to teeth whitening. This classification allows insurers to deny coverage even when implants are medically necessary to restore function.

When a plan does cover implants, expect 50% reimbursement after you meet your deductible. Some newer plans offer up to 80% coverage, but these remain uncommon and typically carry higher monthly premiums. The percentage applies only up to your annual maximum benefit, which ranges from $1,000 to $2,000 for most plans. That maximum covers all dental work in a calendar year, not just implants.

Here's where the math gets frustrating. If your plan covers implants at 50% with a $1,500 annual maximum, and your implant costs $5,000, the insurance pays $1,500—not $2,500 (50% of $5,000). You're responsible for the remaining $3,500. Many patients mistakenly calculate coverage as a percentage of total cost without factoring in the annual cap.

Author: Tyler Grant;

Source: ladylesliebelize.com

Waiting periods create another barrier. Plans that cover implants typically impose 12 to 24-month waiting periods for major services. If you enroll in January 2026, you might not receive implant benefits until January 2027 or 2028. Insurers use waiting periods to prevent people from signing up only when they need expensive work.

Pre-authorization requirements add administrative hurdles. Most insurers demand X-rays, clinical notes documenting medical necessity, and detailed treatment plans before approving coverage. They want proof that an implant is the only viable option, not just the patient's preference over a bridge or partial denture.

Some plans cover implant components differently. They might approve the crown at 50% because crowns are standard major services, but deny the implant post and abutment entirely. This partial coverage leaves patients confused about what they'll actually pay.

The biggest misconception patients have is assuming 'covered' means 'paid for.' When I tell someone their insurance covers implants, they often think that means minimal out-of-pocket cost. In reality, between annual maximums, waiting periods, and percentage limitations, most patients with coverage still pay 70% to 85% of the total bill themselves

— Dr. Michelle Torres

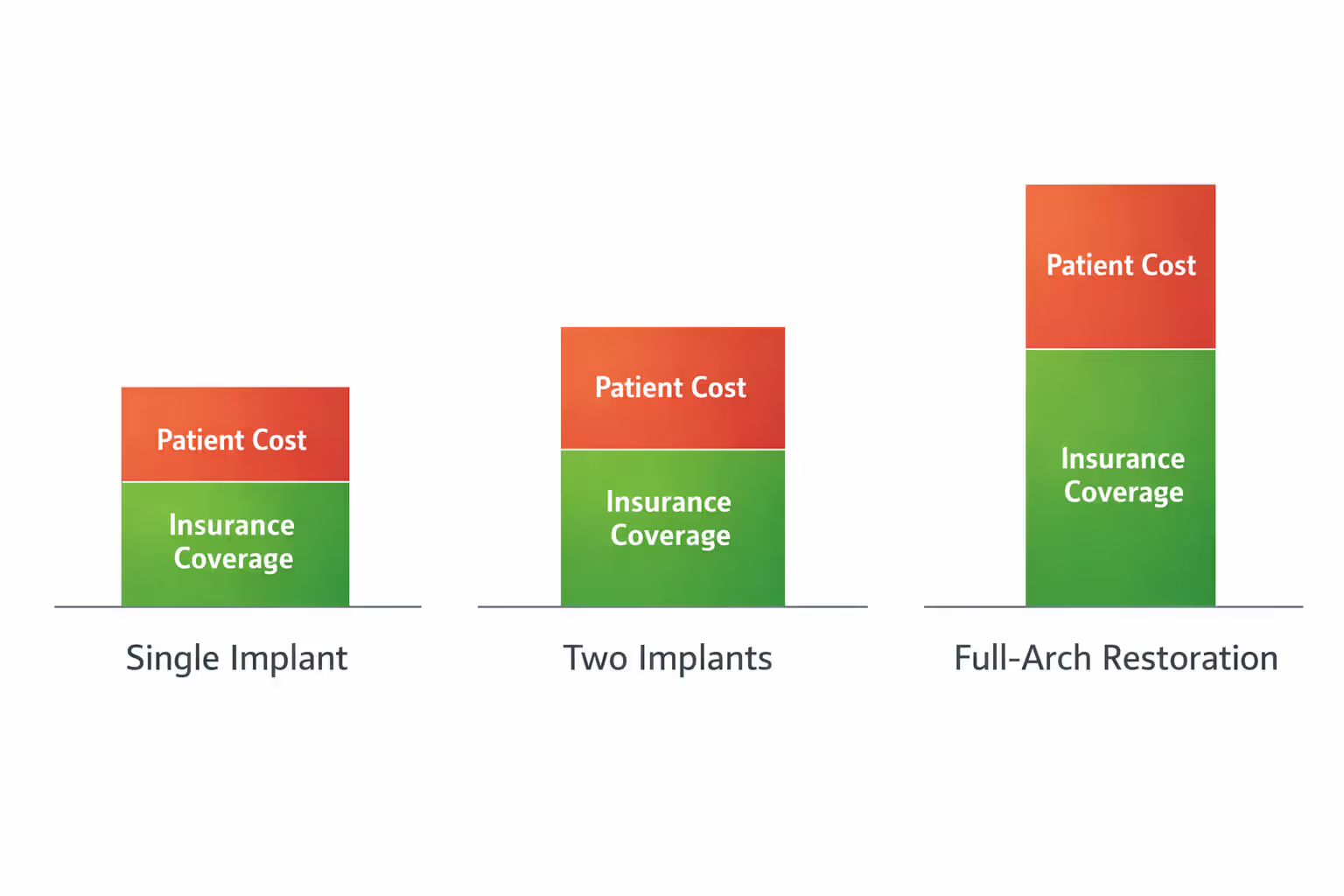

Average Cost of Dental Implants With Insurance Coverage

Insurance changes your out-of-pocket expense, but rarely as dramatically as patients hope. The actual savings depend on your specific plan's coverage percentage, annual maximum, and deductible structure.

Consider a standard single implant costing $5,000. With a plan offering 50% coverage on major services, a $50 deductible, and a $1,500 annual maximum, here's the real math: You pay the $50 deductible first. The insurance calculates 50% of the remaining $4,950, which equals $2,475. But your annual maximum caps their payment at $1,500. Your final out-of-pocket cost is $3,550—not the $2,500 you might have expected from "50% coverage."

Better plans with higher maximums improve the equation. A plan with 50% coverage and a $2,500 annual maximum on that same $5,000 implant would pay $2,475 (limited by the percentage, not the maximum). You'd pay $2,525 plus the deductible.

The following table illustrates realistic scenarios:

| Procedure Component | Cost Without Insurance | With 50% Coverage ($1,500 Max) | With 80% Coverage ($2,000 Max) | Your Out-of-Pocket (50%) | Your Out-of-Pocket (80%) |

| Consultation & X-rays | $300 | $150 | $240 | $150 | $60 |

| Implant Post | $2,000 | $1,000 | $1,600 | $1,000 | $400 |

| Abutment | $800 | $400 | $640 | $400 | $160 |

| Crown | $2,200 | $1,100 | $1,760 | $1,100 | $440 |

| Bone Graft (if needed) | $1,500 | $750 | $1,200 | $1,500* | $1,500* |

| Total | $6,800 | $3,400 | $5,440 | $5,300 | $4,800 |

*Bone graft often exceeds annual maximum after other procedures, leaving full cost to patient

The table assumes the annual maximum applies across all procedures. In reality, if you've already used $800 of your $1,500 maximum on other dental work that year, only $700 remains for your implant.

Timing procedures across benefit years helps maximize coverage. If you need bone grafting before implant placement, scheduling the graft in December and the implant in January spreads costs across two annual maximums. A patient with a $1,500 annual maximum could effectively access $3,000 in benefits by splitting a $6,000 treatment across two calendar years.

Multiple implants strain even generous coverage. Three implants costing $15,000 total with 50% coverage would theoretically generate $7,500 in insurance payments, but the $1,500 annual maximum means you still pay $13,500. Spreading three implants across three years maximizes benefits but delays completing your treatment.

Author: Tyler Grant;

Source: ladylesliebelize.com

Which Dental Insurance Plans Cover Implants

Not all insurance types treat implants equally. The plan structure determines whether coverage exists and how accessible it is.

PPO plans (Preferred Provider Organizations) offer the best chance of implant coverage. These plans typically cover 50% of major services and allow you to see any dentist, though staying in-network reduces costs. About 35% of PPO plans now include some implant coverage, up from 20% five years ago. Look for plans explicitly listing "implant placement" or "endosteal implants" in the benefits summary.

HMO plans (Health Maintenance Organizations) rarely cover implants. These plans focus on preventive care and basic services, requiring you to see network dentists exclusively. When HMOs do cover implants, they often require extensive documentation proving medical necessity—such as implants needed after cancer treatment or traumatic injury.

DHMO plans (Dental Health Maintenance Organizations) function similarly to HMOs with even more restrictions. They might cover implants at a reduced copay rather than a percentage, but only through specific network providers with long waiting lists.

Discount dental plans aren't insurance at all. You pay an annual membership fee ($100 to $350) for access to reduced rates at participating dentists. These plans might offer 20% to 40% discounts on implants, which helps but doesn't compare to actual insurance coverage. They work well as supplements to insurance with low maximums.

Employer-sponsored plans vary wildly. Large companies sometimes negotiate enhanced benefits including implant coverage, while small business plans often exclude them to keep premiums affordable. Review your Summary of Benefits and Coverage (SBC) document—the section on "prosthodontics" or "major services" will specify implant coverage.

Medicare doesn't cover dental implants except in rare circumstances where they're part of reconstructive surgery following an accident or disease. Medicare Advantage plans sometimes include dental benefits, but implant coverage remains uncommon.

Medicaid coverage depends entirely on your state. Most states exclude implants for adults, though some cover them for children with congenital conditions or after trauma. States with more comprehensive adult dental Medicaid programs (like California's Denti-Cal) might cover implants when medically necessary.

Waiting periods for implant coverage typically range from 12 to 24 months. Some plans impose no waiting period if you're enrolling during an employer's open enrollment and had prior coverage elsewhere. Individual plans purchased through healthcare marketplaces almost always include the full waiting period.

Medical necessity requirements force you to prove why an implant is essential rather than elective. Acceptable justifications include: inability to wear dentures due to severe gag reflex or bone loss, implants needed to support radiation therapy for oral cancer, or replacement of teeth lost in a documented accident. Wanting a permanent solution instead of a bridge usually doesn't qualify.

How to Maximize Your Dental Implant Insurance Benefits

Getting the most from your coverage requires strategy, not just hoping your claim gets approved.

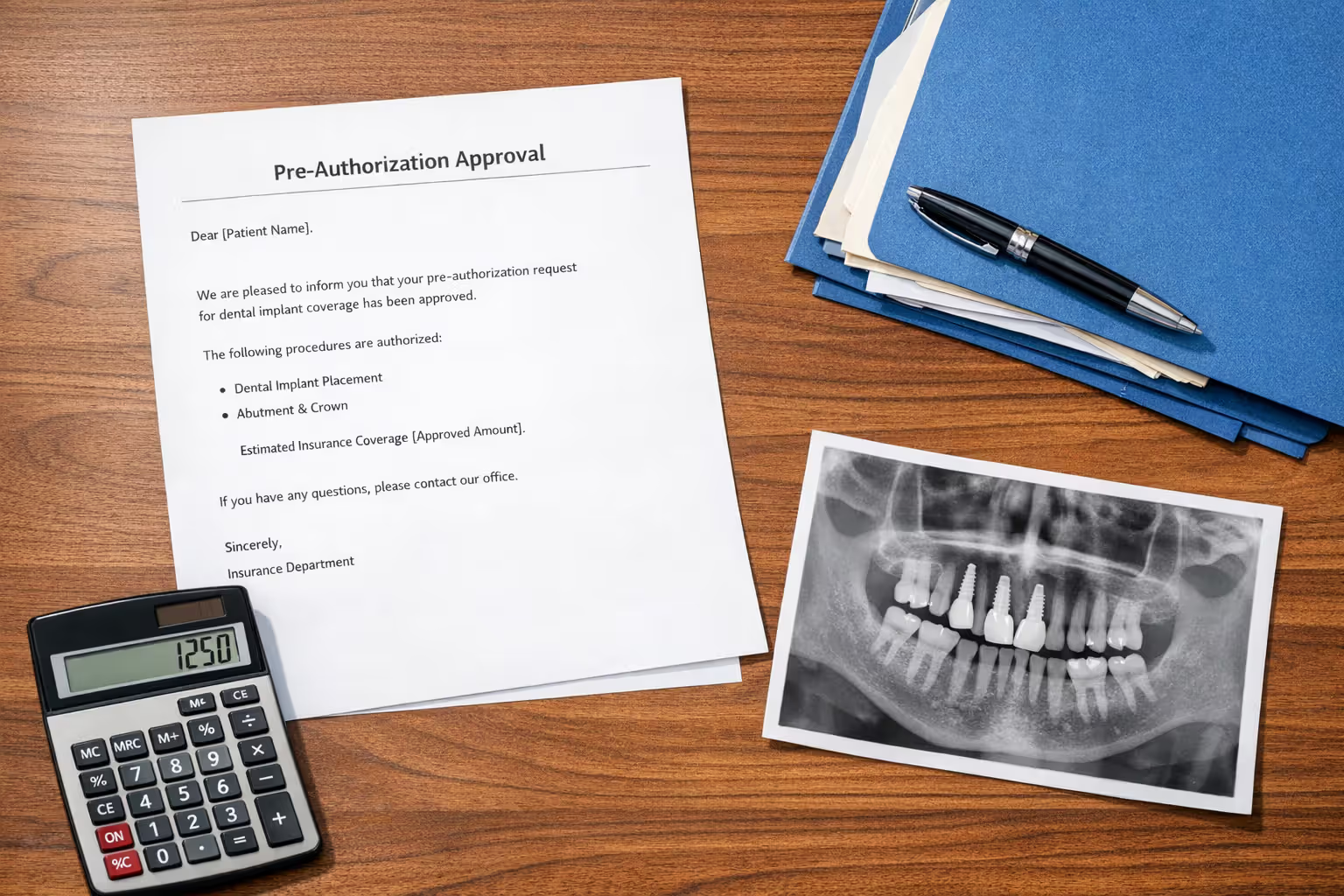

Pre-authorization is non-negotiable. Submit a detailed treatment plan with X-rays and clinical notes before starting any work. Pre-authorization doesn't guarantee payment, but it clarifies what the insurer will cover and prevents surprises. The process takes two to four weeks, so plan accordingly.

Request a predetermination of benefits in writing. This formal estimate shows exactly what the insurance will pay based on your current benefits and remaining annual maximum. Keep this document—it's your leverage if the insurer later denies coverage they initially approved.

Time procedures strategically across benefit years. If you need an implant in November and your annual maximum is exhausted, wait until January when it resets. For multiple implants, schedule one per year to access fresh annual maximums. Yes, this delays treatment, but it could save thousands.

Appeal denials immediately. About 40% of initial denials get overturned on appeal when patients provide additional documentation. Common successful appeal strategies include: letters from your dentist explaining medical necessity, photos showing functional impairment from missing teeth, and documentation of failed alternative treatments like bridges or dentures.

Use flexible spending accounts (FSAs) or health savings accounts (HSAs) to pay out-of-pocket costs with pre-tax dollars. If you're paying $4,000 out of pocket and you're in the 25% tax bracket, using an FSA effectively saves you $1,000. Max out these accounts during open enrollment if you're planning implant work.

Consider supplemental dental insurance if you're planning expensive work. Some companies allow you to purchase additional coverage that stacks with your primary plan, increasing your annual maximum. These policies usually require 12-month waiting periods, so they work only if you're planning ahead.

Coordinate benefits if you have dual coverage (through your employer and a spouse's plan). Primary and secondary insurance can cover different portions of the cost, though combined payments rarely exceed 100% of the bill. File with your primary insurer first, then submit the explanation of benefits to your secondary insurer for additional coverage.

Document everything. Keep copies of all correspondence, pre-authorization letters, treatment plans, and receipts. Insurance companies make mistakes, and you'll need documentation to contest incorrect denials or underpayments.

Author: Tyler Grant;

Source: ladylesliebelize.com

Alternative Payment Options When Insurance Won't Cover Implants

When insurance falls short or doesn't cover implants at all, other financing strategies can make treatment accessible.

In-house payment plans offered by dental practices let you spread costs over 6 to 24 months, often interest-free if you complete payments within the promotional period. A $5,000 implant becomes $208 per month over 24 months with no interest. These plans typically require a down payment of 10% to 30%.

Third-party healthcare financing through companies like CareCredit, LendingClub, or Alphaeon Credit provides loans specifically for medical and dental procedures. Approval depends on your credit score. Interest rates range from 0% promotional rates (if paid within 12-24 months) to 17% to 27% for longer terms. Read the fine print—deferred interest plans charge retroactive interest on the full original balance if you don't pay off the loan before the promotional period ends.

Dental savings plans function like Costco memberships for dental care. You pay $100 to $350 annually for access to discounted rates at participating dentists. Savings on implants typically range from 20% to 40%. Unlike insurance, there are no waiting periods, annual maximums, or claim forms. These plans make sense if you're paying entirely out of pocket and need work done quickly.

Author: Tyler Grant;

Source: ladylesliebelize.com

Health savings accounts (HSAs) and flexible spending accounts (FSAs) let you use pre-tax money for dental implants. HSAs have no annual limit on contributions (though there's a maximum you can contribute each year—$4,300 for individuals in 2026), and funds roll over year to year. FSAs typically cap at $3,200 annually and follow use-it-or-lose-it rules, though some employers allow small carryovers.

Dental schools offer implant placement by supervised students at 30% to 50% of private practice costs. A $5,000 implant might cost $2,000 to $3,000 at a university dental clinic. Treatment takes longer because students work more slowly and faculty must approve each step, but the quality is generally high. Major dental schools in every state offer these programs.

Medical tourism attracts patients to countries like Mexico, Costa Rica, and Thailand where implants cost 50% to 70% less than U.S. prices. A $5,000 U.S. implant might cost $2,000 in Cancun or $1,800 in Bangkok. Factor in travel costs, time away from work, and risks like limited recourse if complications arise. Some patients successfully combine dental work with vacation, but others face expensive corrective procedures back home.

Dental grants and charitable programs help low-income patients or those with special circumstances. Organizations like the Dental Lifeline Network, Cosmetic Dentistry Grants, and various state dental associations offer limited assistance. Competition for these programs is intense, and they typically prioritize patients with medical conditions or severe functional impairment.

Frequently Asked Questions About Dental Implant Insurance Coverage

Dental implants represent a significant financial commitment whether you have insurance or not. Understanding the real costs and realistic coverage expectations helps you plan effectively rather than facing unexpected bills mid-treatment.

If your insurance covers implants, maximize those benefits through pre-authorization, strategic timing, and appeals when necessary. If you're paying entirely out of pocket, explore payment plans, dental savings programs, and tax-advantaged accounts to reduce the financial burden.

The investment in implants extends beyond dollars. Patients consistently report improved quality of life, better nutrition from restored chewing function, and increased confidence compared to removable alternatives. When you understand the true costs upfront and plan accordingly, you can move forward with treatment that restores both function and peace of mind.

Start by requesting a detailed cost estimate from your dentist and a predetermination of benefits from your insurer. These two documents give you the concrete numbers you need to make an informed decision about timing, financing, and whether to proceed with treatment now or plan for it strategically over the next year or two.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.