Patient sitting in a modern dental chair looking surprised while dentist shows a treatment cost estimate on a tablet screen

Dental Insurance Benefits Explained for US Consumers

You're sitting in the dentist's chair when the hygienist mentions you'll need a crown. "No problem," you think, "I have insurance." Then comes the estimate: $1,200, and your portion is $650. Wait—what happened to your coverage?

This scenario plays out in dental offices daily. About 77% of Americans have some form of dental coverage, yet few understand how it actually functions until they're handed a bill that doesn't match expectations.

Let's fix that. Here's everything you need to know about how dental benefits actually work in practice.

What Are Dental Insurance Benefits?

Think of dental insurance as a shared cost arrangement. You (or your employer) pay a monthly fee to an insurance company. In return, they agree to shoulder part of your dental expenses according to a pre-set schedule.

Here's where it gets tricky: dental coverage operates nothing like your medical insurance. While health plans can pay out hundreds of thousands for cancer treatment or surgery, dental plans cap their annual contribution—typically somewhere between $1,000 and $2,000 per person. Hit that limit in June? You're paying full price for everything else until next January.

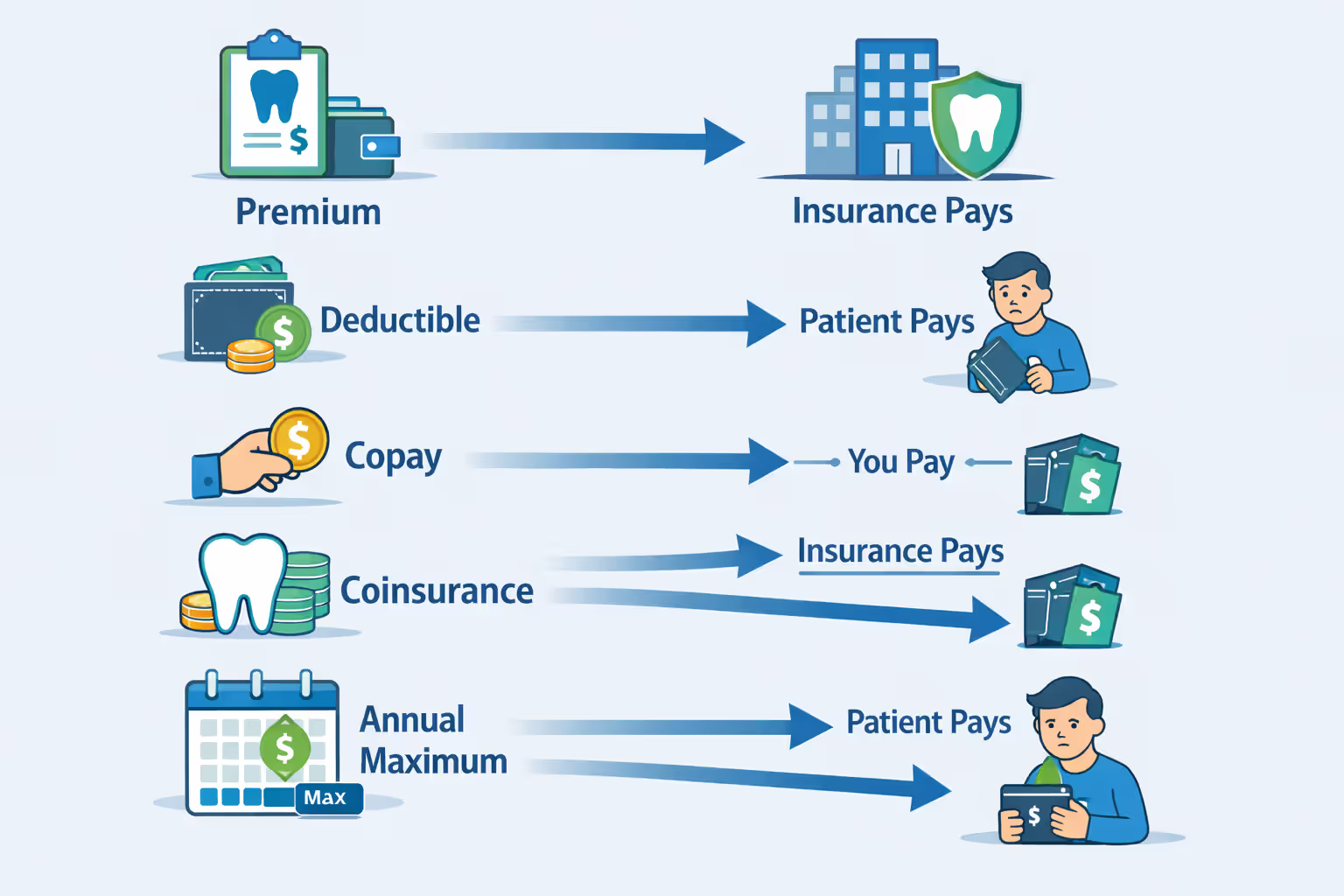

The terminology can trip you up:

Premium: Your monthly payment that keeps the policy active. You pay this whether you see a dentist or not. Most employer plans cover 50-80% of this cost; you pay the rest.

Deductible: The portion you must cover yourself before your insurer contributes anything. Here's the good news—insurers usually don't apply this to preventive visits. You'll typically see deductibles between $50-$150 per person each year.

Copay: You pay a set dollar amount for certain services. Think "$20 per visit" regardless of what happens during that appointment. Dental plans use this less frequently than medical ones.

Coinsurance: Here's where math enters the picture. Your plan might cover 80% of a filling's cost; you handle the other 20%. Unlike copays (which stay constant), coinsurance changes based on the procedure's total price.

Annual Maximum: This is your insurer's yearly spending cap. Most plans reset this limit on January 1st, though some restart on your enrollment anniversary date instead.

One more crucial distinction: dental and medical insurance live separate lives. Different networks, different claim systems, different rules. Your excellent medical coverage tells you nothing about your dental benefits.

Author: Ashley Whitford;

Source: ladylesliebelize.com

How Does Dental Insurance Coverage Work?

The journey starts at enrollment—either when your employer offers coverage during their annual sign-up period, or when you purchase an individual plan directly.

Once you're enrolled, those monthly premiums start flowing to keep your coverage active. Now comes the important part: using it.

You schedule an appointment. Your first decision matters more than most people realize: choosing an in-network versus out-of-network dentist. In-network providers have signed contracts agreeing to charge specific amounts for procedures. They've essentially promised, "We won't charge more than $X for a crown." Out-of-network dentists? They can charge whatever they want.

For expensive work—crowns, bridges, root canals—your dentist's office will usually submit what's called a pre-treatment estimate. This isn't a payment guarantee (your benefits could change, or you might not meet requirements). But it shows what the insurer expects to pay based on your current plan status. Smart patients request these before committing to major procedures.

After your appointment, the real paperwork begins. Your dentist files a claim detailing what they did and what they charged. The insurance company examines this against your specific plan terms: Have you met your deductible yet? What percentage applies to this procedure type? Do you have enough annual maximum left?

Payment typically goes straight to your dentist if you've signed an "assignment of benefits" form. Otherwise, the check comes to you, and you're responsible for paying the dentist separately.

Then arrives the Explanation of Benefits (EOB)—often weeks later. This document shows the submitted charge, the "allowed amount" (what your insurer deems reasonable), what they paid, and what you owe. Read these carefully. They're confusing, but they're also your record of what actually happened financially.

The network question deserves more attention. In-network dentists accept the allowed amount as full payment. Period. If the allowed amount for a crown is $900 and they originally quoted $1,100, they eat that $200 difference. Out-of-network dentists have no such restriction. They can bill you for the gap between their fee and what insurance considers "usual, customary, and reasonable" (UCR) for your zip code. That gap can hit several hundred dollars for major work.

What Does Dental Insurance Typically Cover?

Insurance companies sort procedures into tiers, each with its own payment level. You'll often hear this called the "100-80-50 structure," though your specific percentages might vary.

Preventive Care Coverage

Preventive services usually get covered at 100%, and your deductible doesn't apply. This includes:

- Cleanings twice yearly (some plans limit this to "every six months," which isn't quite the same)

- Regular checkup exams, typically two per year

- X-rays at varying intervals—bitewings annually or semi-annually, full-mouth series every three to five years

- Fluoride treatments, though many plans restrict these to patients under 19

- Sealants on children's permanent molars

The logic is simple: catch problems early, pay less later. A cavity spotted during a routine exam might cost $180 to fill. Wait until it hurts? You're looking at a root canal ($800-$1,500) plus a crown ($1,000-$1,500).

But "100% covered" has limits. Need a third cleaning because of gum disease? Most plans won't cover it unless you have specific periodontal coverage. You'll pay the full cleaning fee out of pocket.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Basic Procedures Coverage

Basic work typically gets covered at 70-80% once you've satisfied your deductible. You'll find these procedures in this category:

- Fillings, both metal amalgam and tooth-colored composite

- Simple tooth extractions

- Root canals on front teeth (incisors and canines)

- Periodontal therapy like scaling and root planing

- Emergency treatment for acute pain

Example: Your filling costs $230. You've already met your $50 deductible earlier in the year. Your plan covers 80% of basic work. You'll pay $46; insurance covers $184.

Watch out for material restrictions. Some plans cover composite fillings at full percentage only on front teeth where appearance matters. Want tooth-colored fillings on your molars? You might pay the cost difference between composite and amalgam, even though your dentist uses composite.

Major Procedures Coverage

Major work gets 50% coverage after your deductible. This category includes the expensive stuff:

- Crowns, onlays, and inlays

- Bridges and full or partial dentures

- Root canals on molars and premolars

- Gum surgery and other periodontal procedures

- Dental implants—though many plans specifically exclude these

A $1,300 crown with 50% coverage means you're paying $650 plus whatever deductible you haven't met. String together several crowns and you'll blow through your annual maximum fast. Once you do, you're covering 100% of remaining costs until your benefit year resets.

Major procedures almost always require pre-authorization. Your dentist submits treatment details and supporting X-rays before starting work. Skip this step and you risk having claims denied completely—leaving you with the full bill.

Orthodontic Coverage

Orthodontic benefits appear less frequently and often cost extra through an additional rider on your base plan. When included, you'll typically see 50% coverage up to a lifetime maximum of $1,000-$2,000 for dependent children. Adult braces? Coverage becomes much rarer.

That "lifetime maximum" is crucial. Blow through your $1,500 orthodontic benefit and it's gone forever—not just for this year, but permanently. Braces generally take 18-24 months, with insurance paying a percentage of each monthly installment rather than a lump sum upfront.

Understanding Your Dental Plan Details

Your plan's Summary of Benefits and Coverage (SBC) document contains the details that determine what you'll actually pay. Most people never read it until they're disputing a bill.

Waiting Periods control when you can access certain benefits after enrolling. A standard structure looks like:

- Zero waiting period for preventive services

- Three to six months for basic procedures

- Twelve months for major procedures

Enroll in March and need a crown in May? If your plan has a 12-month major work waiting period, you're paying full freight. Employer-sponsored plans frequently waive these waiting periods, but individual plans impose them almost universally to prevent people from enrolling only when expensive treatment looms.

Annual Maximums reset on schedule—usually January 1st, but sometimes on your specific enrollment anniversary. Picture this: your maximum is $1,500 and you've used $1,350 by mid-November. You have $150 left until the reset. Need $800 worth of work? Wait until January and you'll save $650 by using a fresh benefit year.

Coverage Limitations dictate how frequently you can receive specific treatments:

- Crowns on the same tooth only once every five to seven years

- Denture replacements every five to ten years

- Cleanings twice per rolling 12-month period (not twice per calendar year—there's a difference)

- Bitewing X-rays once per year; full-mouth series once every three to five years

These restrictions prevent overtreatment abuse and control insurer costs. But they can frustrate you if a crown fails after four years and you need replacement.

Exclusions list what never receives coverage under any circumstances:

- Purely cosmetic procedures like whitening, veneers for aesthetics alone, or cosmetic bonding

- Dental implants on many plans

- Treatment for injuries (your medical insurance should cover this instead)

- Procedures started before your coverage began

- Services the insurer deems not medically necessary

Some plans exclude composite fillings on molars entirely, or they'll only pay what amalgam would cost, leaving you to cover the difference for tooth-colored material.

Pre-authorization Requirements apply to expensive treatment. Your dentist submits a detailed treatment plan before touching your teeth. The insurer reviews it for medical necessity and coverage eligibility. Pre-authorization isn't a payment guarantee—your benefits might change, or you could leave the plan—but it provides reasonable cost certainty before committing.

Your Explanation of Benefits (EOB) shows up after treatment. It lists the submitted charge, the allowed amount (what the insurer considers reasonable), the insurance payment, and your responsibility. If your dentist charged $1,100, the allowed amount is $850, and your plan covers 50%, insurance pays $425. What you owe—whether it's the remaining $425 or the full $675—depends on network status. In-network dentists must accept the allowed amount as full payment. Out-of-network dentists can bill you for their full charge.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Common Dental Insurance Mistakes to Avoid

People with coverage make predictable errors that cost them money or create billing surprises:

Skipping Preventive Appointments: Your plan covers two cleanings yearly at 100%. Skip them and you're wasting benefits you've prepaid through premiums. Beyond the financial waste, you're missing the chance to catch small problems before they become expensive ones.

Assuming Network Participation: "We accept insurance" doesn't mean "We're in your specific network." Every insurer has different networks. Always confirm your dentist's network status before scheduling—especially for procedures costing over $500. An out-of-network crown might cost you $850 instead of $600 for identical work.

Ignoring Annual Maximum Timing: Scheduling multiple crowns in December after you've already used $1,300 of your $1,500 maximum means you're paying nearly full price for most of that work. Split procedures across the benefit year boundary and save potentially thousands.

Misunderstanding Waiting Periods: Enrolling in November when you already know you need root canals and crowns, then trying to schedule in December, results in denied claims if waiting periods apply. You can't game the system this way. Plan your enrollment timing around anticipated needs when possible.

Skipping Pre-Authorization: Moving forward with major work without pre-authorization invites disputes about medical necessity and coverage eligibility. A simple pre-treatment estimate from your dentist's office prevents $1,000+ surprises.

Choosing Materials Without Cost Checking: Requesting premium crown materials or tooth-colored fillings for molars without understanding your plan's material limitations can double your out-of-pocket expense. Ask your dentist's billing staff to verify coverage before selecting materials.

Forgetting Out-of-Network Consequences: Your friend raves about their dentist, so you book an appointment without checking network status. That cleaning costs you $45 instead of $0. That crown costs you $900 instead of $600. Network status matters tremendously.

Understanding Dental Insurance Terminology

| Term | Definition |

| Premium | Your monthly payment that maintains active coverage, whether or not you visit a dentist that month |

| Deductible | What you must pay yourself before your insurer contributes to covered services (commonly $50-$150 yearly) |

| Copay | A set dollar amount you pay for specific services regardless of actual cost (less common in dental coverage) |

| Coinsurance | Your percentage of costs after satisfying the deductible (you pay 20% while insurance covers 80%, for example) |

| Annual Maximum | The total dollar amount your insurer will pay for covered services during a benefit year (usually $1,000-$2,000) |

| Waiting Period | Required time between enrollment and when you can access certain benefits (often 6-12 months for major work) |

| EOB (Explanation of Benefits) | A detailed statement showing what was charged, what the insurer paid, and what you must pay |

| UCR (Usual, Customary, and Reasonable) | What an insurer considers an appropriate charge for specific services in your geographic region |

How to Maximize Your Dental Insurance Benefits

Strategic thinking about dental benefits can save you hundreds or thousands annually.

Split Major Work Across Benefit Years: Need $3,200 in dental work and your annual maximum is $1,500? Schedule half in November-December and half in January-February. This approach uses two years' maximums for one treatment plan. Many dentists familiar with insurance will proactively suggest this timing.

Exhaust Preventive Benefits Annually: Those two cleanings and exams cost you nothing out-of-pocket but deliver real value. They catch problems when they're small. A cavity detected at your routine cleaning might cost $170 to fill. Wait until it causes pain and you're facing a $1,300 root canal plus $1,200 crown.

Calculate In-Network Savings: The difference between in-network and out-of-network costs can reach 30-50% for major procedures. If your longtime dentist is out-of-network, run actual numbers. Sometimes the relationship value justifies higher costs. Often it doesn't—you're just paying more for the same clinical outcome.

Combine with FSA/HSA Accounts: Flexible Spending Accounts and Health Savings Accounts let you pay dental costs with pre-tax dollars. Anticipating $2,000 in dental expenses? Contributing that amount to an FSA effectively gives you a 22-35% discount (depending on your tax bracket) on top of insurance coverage.

Prioritize Treatment Strategically: Need three crowns but can't afford all three this year? Ask your dentist which tooth poses the most clinical risk. Address that one now, then space the others across future benefit years. This spreads costs while maximizing your annual maximums.

Review Alternatives During Open Enrollment: Most people auto-renew the same dental plan annually without comparing options. If you're anticipating major work, a plan with a $2,000 annual maximum (even with $15/month higher premiums) might save you $800 overall compared to your current $1,500 maximum plan.

Discuss Treatment Options with Cost in Mind: Some problems have multiple solutions with different coverage implications. A damaged tooth might be savable with a crown or extractable for replacement with a bridge. Coverage percentages differ significantly, and your dentist can explain both the clinical and financial trade-offs.

I've watched patients leave thousands of dollars on the table simply because they didn't understand their benefits before treatment. Dental insurance has strict yearly caps and coverage tiers that require advance planning. The patients who review their Summary of Benefits before scheduling major procedures avoid financial surprises and make informed decisions about their oral health. I recommend every patient request a pre-treatment estimate for any procedure costing over $300

— Dr. Jennifer Martinez

Frequently Asked Questions About Dental Insurance Benefits

Dental insurance operates on principles entirely different from medical coverage. Annual maximums cap insurer spending at $1,000-$2,000. Coverage divides into tiers with different payment percentages. Prevention receives heavy emphasis. Understanding these mechanics—how deductibles, coinsurance percentages, and annual maximums interact—puts you in control of both oral health and financial decisions.

The key insight: dental insurance is a cost-sharing tool, not comprehensive coverage. Annual maximums won't cover extensive reconstructive work. But they substantially reduce costs for routine care and moderate procedures. Strategic treatment timing, full use of preventive benefits, and staying in-network maximize the value you extract from premiums you're already paying.

Before scheduling any work costing over $500, take three steps: review your plan documents to understand remaining annual maximum, confirm your dentist's network status with your insurer directly, and request a pre-treatment estimate showing expected coverage. These tasks take thirty minutes but prevent billing surprises that can hit four figures.

Your dentist's office staff can help interpret benefits and suggest timing strategies optimizing coverage. They handle insurance daily and know the common pitfalls.

Dental insurance delivers maximum value when you understand its limitations and structure your care accordingly. Regular preventive visits catch problems early. Strategic scheduling of major procedures maximizes annual benefit usage. Informed material choices prevent unnecessary out-of-pocket expenses. Combined, these approaches ensure you receive full value from coverage while maintaining optimal oral health.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.