Wallet with dollar bills next to a dental mirror and tooth model on a blurred dental office background

Why Is Dental Insurance So Bad?

You've probably experienced this frustration: you pay monthly premiums for dental insurance, only to discover your plan covers almost nothing when you actually need a crown, root canal, or implant. Meanwhile, your medical insurance—despite its own flaws—doesn't cap coverage at an arbitrary $1,500 per year. What's going on?

Dental insurance operates under a fundamentally different model than medical coverage, one that hasn't evolved much since the 1960s. The result is a system that functions more like a discount coupon than true insurance, leaving millions of Americans to pay thousands out-of-pocket for necessary care. Understanding why dental insurance works this way requires looking at historical decisions, industry economics, and structural limitations that persist decades later.

How Dental Insurance Became Separate from Health Insurance

The separation between dental and medical coverage wasn't based on science or patient need—it was an accident of history and labor negotiations.

Employer-sponsored health insurance became widespread in the United States during World War II, when wage freezes pushed companies to compete for workers through benefits instead of salaries. Medical coverage emerged as the primary benefit, but dental care wasn't initially included. At the time, dentistry was seen as less critical than hospital and physician services, and most dental work consisted of extractions rather than the restorative procedures common today.

Dental insurance didn't appear as a standalone product until the early 1960s. Unions began negotiating for dental benefits separately, and insurance carriers developed plans with built-in cost controls that medical insurance lacked. These plans were designed to cover routine preventive care and share costs on basic procedures—not to protect against catastrophic dental expenses the way medical insurance protects against hospital bills.

This historical split created two parallel systems with different philosophies. Medical insurance evolved into a risk-pooling mechanism meant to protect against unpredictable, expensive events. Dental insurance remained a prepayment plan for predictable maintenance, with strict limits to keep premiums low.

The Affordable Care Act reinforced this separation by requiring medical coverage but treating dental as optional for adults. Pediatric dental became an essential health benefit, but adult dental care remained outside the regulatory framework that governs medical insurance. This means dental plans face fewer requirements around coverage limits, out-of-pocket maximums, and benefit design.

The Annual Maximum Problem: Why Coverage Stops at $1,000–$2,000

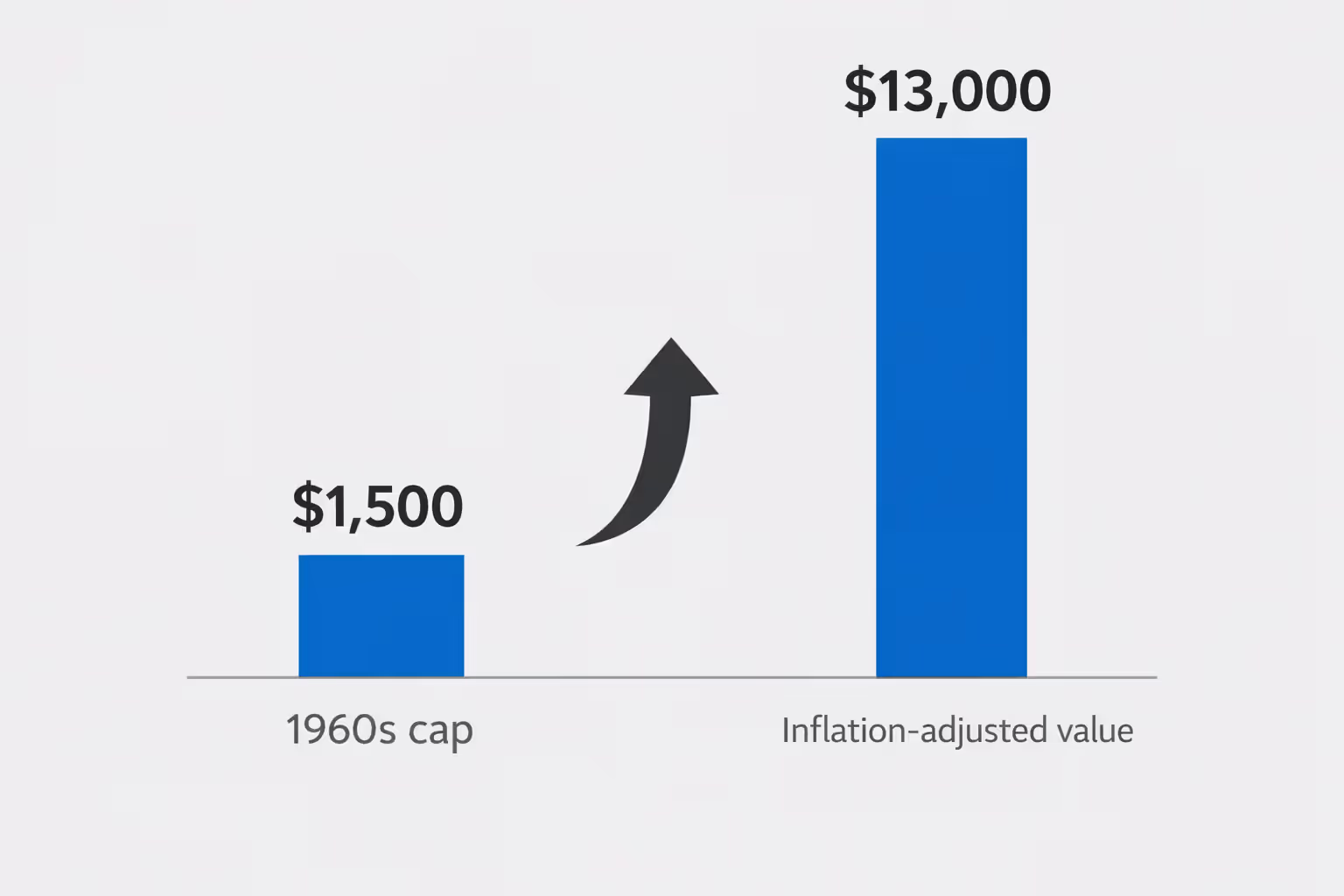

Here's a startling fact: the typical dental insurance annual maximum in 2026 is $1,500 to $2,000—almost identical to the caps set when these plans first appeared in the 1960s. If dental maximums had kept pace with inflation, they would be $12,000 to $15,000 today.

Why haven't these limits increased? Insurance carriers have little incentive to raise them. Employers shopping for dental plans typically prioritize low premiums over comprehensive coverage, since dental is viewed as a supplemental benefit rather than essential protection. Plans with higher maximums cost more, and most HR departments aren't willing to pay the difference.

Author: Ashley Whitford;

Source: ladylesliebelize.com

From the insurer's perspective, low annual maximums reduce risk and keep premiums affordable—usually $20 to $50 per month for individual coverage. But this creates a fundamental mismatch: a single dental implant costs $3,000 to $5,000, while your annual maximum might be $1,500. One procedure exhausts your entire year's benefit.

This cap structure means dental insurance doesn't actually insure you against major dental expenses. If you need multiple crowns, a bridge, or extensive periodontal work, you'll hit your maximum quickly and pay the rest yourself. A patient requiring $8,000 in restorative work might receive $1,500 from insurance and owe $6,500 out-of-pocket—hardly the protection most people expect from "insurance."

The annual maximum resets each calendar year, which creates perverse incentives. Dentists often recommend splitting treatment across two years to maximize insurance benefits, delaying care that should happen sooner. A patient needing four crowns might get two in December and two in January, not because it's clinically optimal, but because it's the only way to use two years of benefits.

What Dental Insurance Actually Covers and What It Doesn't

Dental insurance divides procedures into three categories, each with different coverage levels:

| Category | Typical Coverage | Examples | Annual Limit |

| Preventive | 100% | Cleanings (2×/year), exams, X-rays, fluoride | Applies to maximum |

| Basic | 70–80% | Fillings, extractions, root canals, periodontal maintenance | Applies to maximum |

| Major | 50% | Crowns, bridges, dentures, implants (if covered) | Applies to maximum |

This tiered structure—often called "100-80-50" coverage—sounds reasonable until you realize all categories count toward the same annual maximum. Two cleanings and an exam might use $300 of your $1,500 limit, leaving $1,200 for everything else that year.

The 100-80-50 Coverage Structure Explained

The percentage coverage is misleading because it doesn't apply to what your dentist actually charges—it applies to the "allowed amount" or "usual and customary rate" the insurance company decides is appropriate.

Here's how it works in practice: Your dentist charges $1,200 for a crown. Your insurance company's allowed amount is $800. Your plan covers 50% of major procedures, so they pay $400. You owe the remaining $800—the $400 copay plus the $400 difference between the actual charge and allowed amount. You thought you had 50% coverage, but you're actually paying two-thirds of the bill.

This gap between actual and allowed amounts varies by location and insurance carrier, but it's rarely explained clearly in plan documents. Patients discover it only when they receive their bill.

Why Implants and Advanced Procedures Aren't Covered

Dental implants—the gold standard for replacing missing teeth—are excluded or severely limited by most dental plans. Insurance companies classify implants as elective or cosmetic, even though they're often the most durable and functionally superior option.

The real reason for exclusion is cost control. A single implant with crown costs $3,000 to $5,000, and many patients need multiple implants. If insurance covered these at even 50%, it would quickly exceed annual maximums and drive up premiums. Plans that do cover implants typically require premium tiers that cost significantly more per month.

Some plans cover the crown portion of an implant (the visible tooth) but not the surgical implant post, creating confusing partial coverage. Others cover implants only if tooth loss occurred while you were insured, excluding congenitally missing teeth or losses that happened before your coverage started—the "missing tooth clause."

Advanced procedures like full-mouth reconstruction, TMJ treatment, or orthodontics for adults face similar exclusions. These are either carved out entirely or subject to separate lifetime maximums (common with orthodontics, which might have a $1,500 lifetime limit).

Author: Ashley Whitford;

Source: ladylesliebelize.com

Waiting Periods and Coverage Limitations That Delay Care

Most dental plans impose waiting periods before you can access benefits for anything beyond preventive care:

- Preventive care: No waiting period (immediate coverage)

- Basic procedures: 3 to 6 months

- Major procedures: 6 to 12 months

These waiting periods exist to prevent "adverse selection"—people buying insurance only when they know they need expensive work, then canceling after treatment. But they create real hardship for people who need immediate care.

If you enroll in a new plan and discover you need a root canal and crown, you might wait six months for the root canal coverage and twelve months for the crown. Delaying necessary treatment can worsen dental problems, leading to more extensive (and expensive) procedures later.

The missing tooth clause adds another barrier. Many plans won't cover replacement of teeth that were missing before your coverage started. If you lost a tooth five years ago and now want an implant or bridge, your current insurance may deny the claim entirely, even if you've been paying premiums for years.

Pre-existing condition exclusions—prohibited in medical insurance since 2014—remain perfectly legal in dental plans. An insurer can deny coverage for treatment of a condition that existed before you enrolled, even if you weren't aware of it.

Why Dental Work Costs So Much Even With Insurance

The sticker shock of dental bills surprises people who assume their insurance provides meaningful protection. Several factors explain why costs remain high:

Fee schedules don't reflect actual prices. Insurance companies set allowed amounts based on regional averages from years past, not current market rates. A dentist in a high-cost urban area might charge $1,500 for a crown because that's what it costs to run a practice there, but insurance allows only $900. The patient pays the $600 difference plus their copay.

Out-of-network providers have no contracted rates. If you see a dentist outside your plan's network, you'll pay the full difference between their charges and your insurance's allowed amount. These "balance bills" can be substantial—sometimes 40% to 60% of the total cost.

Diagnostic and preparatory work adds up. Before major procedures, you often need X-rays, exams, and sometimes additional diagnostics. Each service counts toward your annual maximum. A patient budgeting for a $1,200 crown might not account for the $200 in pre-treatment costs, pushing them closer to their limit.

The annual maximum is a hard stop. Once you've exhausted your benefit, every additional dollar comes from your pocket. A patient needing $5,000 in care will pay roughly $3,500 themselves after a typical $1,500 maximum, assuming the insurance pays its share before the cap.

Dental insurance was never designed to cover major restorative work. It's a maintenance plan with a benefits cap that hasn't changed in 50 years. Patients expect it to function like medical insurance, but it's fundamentally different—and that gap between expectations and reality causes enormous frustration

— Dr. Rebekah Lucier Pryles

Is Dental Insurance Worth Keeping?

Whether dental insurance makes financial sense depends on your specific situation, but for many people, the math doesn't add up.

When dental insurance makes sense: - Your employer pays most or all of the premium - You use preventive care regularly (two cleanings per year at $150 each = $300 value) - You anticipate needing one or two basic procedures annually - You prefer predictable copays over negotiating cash prices

When you might skip it: - You're paying the full premium yourself (often $400–$600 annually for individual coverage) - You have excellent oral health and rarely need more than cleanings - You need major work that will exceed the annual maximum anyway - You have access to a dental school or low-cost clinic

Run the numbers: If you pay $50/month ($600/year) in premiums, use two cleanings ($300 value), and need one filling ($200 insurance benefit after copay), you've received about $500 in value for $600 in premiums. You're behind financially, though you've gained some price certainty.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Alternatives to traditional dental insurance:

Dental discount plans charge an annual fee ($100–$200) for access to negotiated rates, typically 10% to 60% off standard prices. There's no annual maximum, no waiting periods, and no claims process—you just pay the discounted rate at time of service. These work well for people who need major work or want flexibility.

Health Savings Accounts (HSAs) let you set aside pre-tax money for dental expenses if you have a high-deductible health plan. You control the funds, there's no "use it or lose it" deadline, and you can accumulate savings for expensive procedures.

Cash-pay negotiation is increasingly common. Many dentists offer 5% to 15% discounts for payment in full at time of service, since they avoid insurance paperwork and delayed payments. For major work, ask about payment plans—many practices offer interest-free financing for 6 to 12 months.

Dental tourism has become viable for extensive work. Traveling to Mexico, Costa Rica, or Colombia for implants or full-mouth reconstruction can save 50% to 70% even after travel costs, though it requires careful research to find qualified providers.

Frequently Asked Questions

Dental insurance's limitations aren't accidental—they're baked into a system designed in the 1960s that has barely evolved since. The combination of frozen annual maximums, restrictive coverage tiers, waiting periods, and missing tooth clauses means dental insurance functions more like a discount coupon than real financial protection.

For people with employer-subsidized coverage who use preventive care regularly, dental insurance provides modest value. But if you're paying full premiums yourself or need major restorative work, the math often doesn't work in your favor. Understanding these structural limitations helps you make informed decisions about whether to keep your plan, explore alternatives like discount plans or HSAs, or negotiate cash rates directly with your dentist.

The gap between what people expect from dental insurance and what it actually delivers creates frustration across millions of American households each year. Until the industry fundamentally restructures—raising annual maximums, expanding coverage for major procedures, and eliminating arbitrary waiting periods—patients will continue paying thousands out-of-pocket despite having "insurance." Knowing how the system works at least lets you plan accordingly and avoid unpleasant financial surprises.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.