Dental crown placed on a dentist tray next to dental instruments and a blurred insurance document in a clean clinical setting

How Much Is a Dental Crown with Insurance?

Here's what most people don't realize: that "50% coverage" your insurance company loves to advertise rarely means you'll pay exactly half. Between annual caps that run out halfway through the year, fee schedules that bear zero resemblance to what dentists actually charge, and enough fine print to wallpaper your bathroom, calculating your real cost feels like solving a calculus equation blindfolded.

The difference between your expected cost and your actual bill often hits $300-$700. Sometimes more. Let's break down where that gap comes from and what you'll actually pay when you sit down in that chair.

What Does Dental Insurance Typically Cover for Crowns

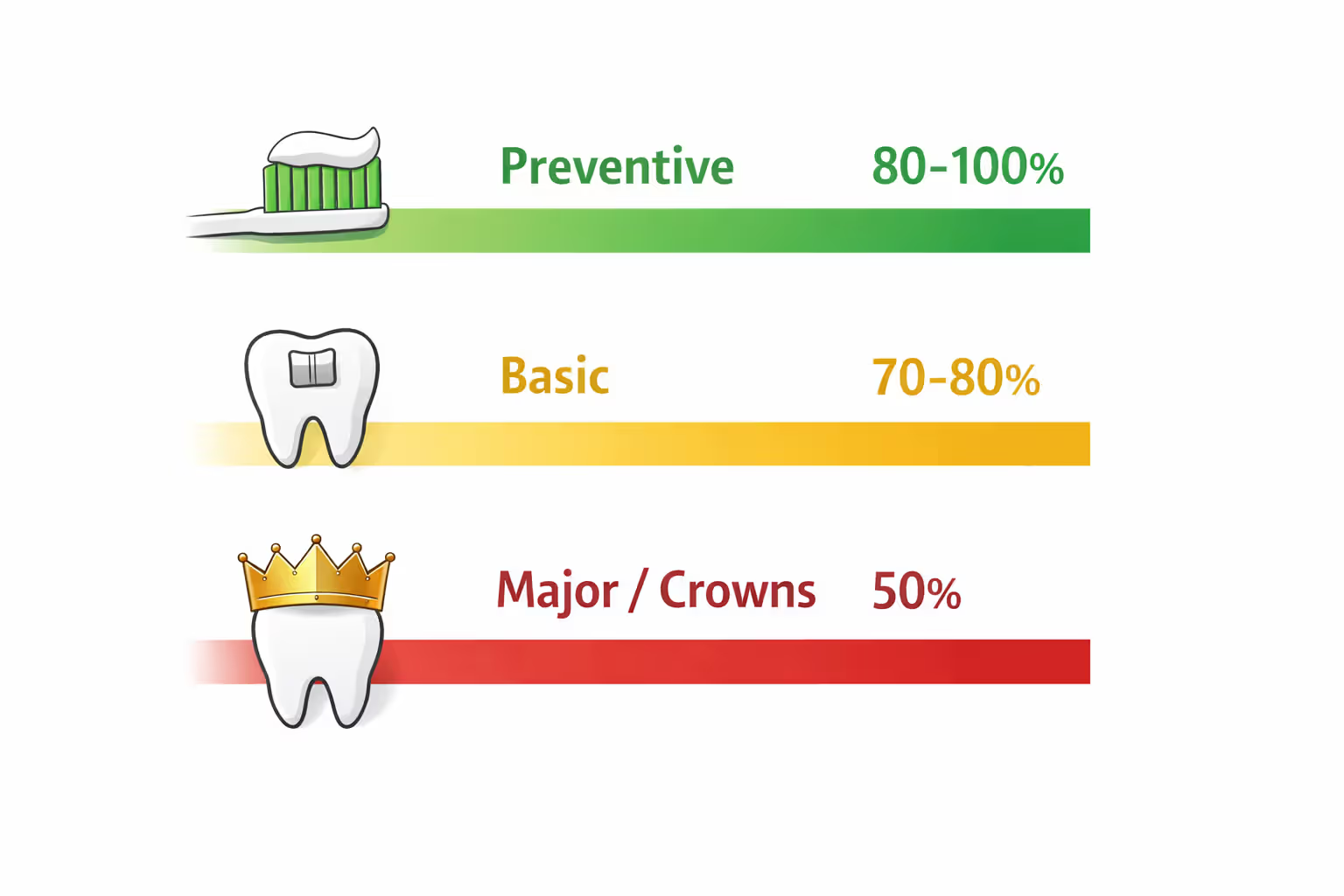

Here's the basic framework: insurance companies sort dental work into three buckets. Preventive stuff like cleanings? They'll cover 80-100%. Basic work like fillings? You're looking at 70-80%. Major procedures—including crowns—drop down to 50% coverage after your deductible.

That's the standard model. Budget plans sometimes bottom out at 40% for major work. High-end employer plans occasionally bump up to 60%, though you'll need a pretty generous benefits package to see that.

Now add the annual maximum—the total dollar amount your insurance will pay in a calendar year. For most plans, that ceiling sits around $1,500 to $2,000. Sounds reasonable until you do the math. Let's say you've already burned through $900 on a root canal and some fillings. Your crown costs $1,400, and your insurance would normally pay 50% ($700). But you've only got $600 left before hitting your annual max. Guess who's covering that extra $100? Plus your $700 copay. Your total: $800 instead of the $700 you calculated.

New to your insurance plan? You're probably facing a waiting period. Most insurers make you wait 6-12 months before they'll cover major procedures. Sign up in September, crack a tooth in December, and you're paying the full freight yourself—coverage won't kick in until the following September at the earliest. The emergency room can't even help you bypass this rule.

Insurance types matter more than most people think. PPO plans let you see any dentist, though staying in-network saves you money. HMO plans lock you into specific providers but typically charge lower premiums. Then there are "discount plans"—these aren't insurance at all. You pay a yearly membership fee, and participating dentists knock 20-30% off their normal rates.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Watch out for replacement restrictions. Try to get a new crown on the same tooth within five years of the last one, and your claim will likely get rejected. The only exceptions? You'll need to prove the crown fractured, fell out due to faulty bonding, or failed because of defective materials. If it just wore down from normal chewing, you're stuck waiting or paying yourself.

Most plans also require pre-authorization. Your dentist sends over X-rays and treatment notes before you schedule anything. The insurance company reviews everything to make sure you actually need a crown versus, say, a large filling. This process eats up 1-3 weeks and can end in approval, partial approval, or a flat rejection.

Average Out-of-Pocket Costs for Dental Crowns with Insurance

Here's where things get messy. Your dentist charges one price. Your insurance pays based on a completely different number.

Example: Your dentist's fee for a porcelain crown is $1,400. Your insurance company decides the "allowable charge" for that crown is $1,000. They pay 50% of what they think it should cost—not what it actually costs. So they send $500. You're on the hook for their $500 portion plus the $400 difference between real price and allowed price. Total damage: $900, not the $700 you expected.

Cost by Crown Material Type

The material you choose affects both the total price and what insurance will actually pay.

Porcelain-fused-to-metal crowns run about $800-$1,500. These blend a metal base with a porcelain coating. Insurance generally approves them for any tooth location. After 50% coverage, you'll pay somewhere between $550-$650 out of pocket—assuming your dentist's fee matches the insurance fee schedule.

All-ceramic or all-porcelain crowns cost $900-$2,000. They look fantastic—totally natural. Insurance companies like them for front teeth where people can see them. For back molars? They might only approve payment at the porcelain-fused-to-metal rate, telling you to pay the upgrade difference yourself. Expect to pay $600-$1,000 after insurance chips in.

Gold and metal alloy crowns range from $900-$2,500. They last forever but look like, well, metal teeth. Insurance treats them the same as porcelain-fused-to-metal, so figure on $550-$900 as your share.

Zirconia crowns represent newer technology—super strong like metal but tooth-colored. Price tag: $1,000-$2,500. Some insurance companies call these "cosmetic upgrades" and only pay what they'd pay for regular porcelain. The difference comes out of your pocket, pushing your cost to $650-$1,200.

CEREC same-day crowns get milled by a computer right in the office during your appointment. One visit, done. Cost: $1,000-$2,000. Insurance usually pays the same as traditional crowns, though a few plans reduce benefits for "premium" technology. You'll pay $600-$1,100.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Regional Price Variations

Where you live completely changes the game. Coastal cities charge 30-50% more than rural areas in the Midwest or South.

In Manhattan or San Francisco, that porcelain crown might cost $2,000-$2,500. But insurance still uses their fee schedule—let's say $1,200. Their 50% coverage gives you $600. You're stuck with $1,400-$1,900 as your portion.

Rural areas in Oklahoma or Arkansas? Same crown costs $800-$1,100. Insurance allows maybe $900, pays $450, and you cover $350-$650.

Mid-sized cities—think Denver, Charlotte, or Phoenix—land in the middle ground: $1,100-$1,600 total cost, with your share running $600-$900 after insurance pays up.

How Much Does a Dental Crown Cost Without Insurance

No insurance means you're negotiating with your dentist's full price list. Typical range: $800-$2,500 depending on what material you choose and where you live.

Here's the breakdown for uninsured patients:

- Metal crowns: $900-$1,400

- Porcelain-fused-to-metal: $900-$1,500

- All-porcelain: $1,000-$2,000

- Zirconia: $1,200-$2,500

- Gold: $1,200-$2,500

Those numbers only cover the crown itself. Need a root canal first? Add $800-$1,500. If your tooth needs structural rebuilding (called a core buildup), tack on another $150-$400. Post and core placement costs $250-$600.

Many dentists knock 10-20% off for cash-paying patients who settle the bill immediately. Dental schools offer treatment for 30-50% below market rates—you're getting work done by students under faculty supervision, so appointments take longer and require more visits.

Payment plans through CareCredit or LendingClub offer promotional 0% interest periods, usually 6-24 months. Sounds great until you read the fine print. Miss one payment or don't pay off the balance before the promo period ends, and they hit you with deferred interest—20-30% APR calculated back to your original purchase date. That $1,500 crown suddenly costs $1,900.

| Crown Type | Average Total Cost | Insurance Typically Pays (50%) | Your Cost With Insurance | Your Cost Without Insurance |

| Metal | $900-$1,400 | $450-$700 | $450-$700 | $900-$1,400 |

| Porcelain-fused-to-metal | $900-$1,500 | $450-$750 | $550-$800 | $900-$1,500 |

| All-porcelain | $1,000-$2,000 | $500-$800* | $600-$1,200 | $1,000-$2,000 |

| Zirconia | $1,200-$2,500 | $500-$900* | $700-$1,600 | $1,200-$2,500 |

| Gold | $1,200-$2,500 | $600-$1,000 | $600-$1,500 | $1,200-$2,500 |

*Insurance might only pay the porcelain-fused-to-metal rate; you cover the material upgrade difference

Factors That Affect Your Dental Crown Insurance Coverage

A bunch of variables determine whether your claim gets approved and how much money actually shows up.

In-network versus out-of-network dentists: In-network providers have signed contracts agreeing to reduced fees in exchange for being on the insurance company's preferred list. Let's say an in-network crown costs $1,000 and your plan covers 50%. You pay $500, done. Take that same crown to an out-of-network dentist who charges $1,600. Insurance still only pays $500 (their 50% of the allowed $1,000 in-network rate). You're covering the remaining $1,100.

Medical necessity documentation: Insurance won't pay for cosmetic upgrades. Your dentist needs to prove the crown prevents further damage or restores normal function. Acceptable reasons include large fractures, decay too extensive for filling, protecting a tooth after root canal treatment, or replacing a failed filling that's been patched too many times. "I want prettier teeth" gets rejected immediately.

Pre-existing conditions: Tooth already cracked before you signed up for coverage? Still within your waiting period? That's a denial. Some plans specifically exclude anything that existed before your enrollment date.

Crown replacement timing rules: Got a crown three years ago and need a new one now? Insurance typically says no. Standard policies require 5-7 years between replacements on the same tooth. You can override this if the crown fractured, fell off due to bonding failure, or you suffered facial trauma in an accident. Regular wear from chewing doesn't count.

Annual maximum exhaustion: Hit your yearly benefit limit in August? Every claim you submit from September through December gets automatically denied. The calendar flips to January, your maximum resets, and claims get approved again. Timing matters enormously.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Alternative treatment clauses: Some policies only cover the cheapest option. Insurance might argue a big filling would work instead of a crown. They'll pay filling rates even though your dentist recommends a crown. The difference comes out of your wallet.

Missing diagnostic materials: Insurance companies want specific X-rays, sometimes periodontal measurements, occasionally clinical photos. Submit incomplete documentation, get denied.

What to Do If Your Dental Insurance Denied Your Crown

Rejections happen all the time. Knowing why and what to do next can flip many denials to approvals.

Why claims get rejected:

- Waiting period still running: You haven't been enrolled long enough for major coverage to activate. Fix: Double-check your start date and waiting period terms. If you're close to the end date, ask your dentist whether treatment can wait a few weeks.

- Insurer says it's not medically necessary: They think a filling or something cheaper would work fine. Fix: Have your dentist send additional X-rays, photos, and detailed notes explaining exactly why other options won't work.

- Too soon for replacement: Your previous crown was placed within the policy's timeline restrictions. Fix: Document how the crown failed—photos of the fracture, notes from clinical examination. If an accident caused damage, send accident reports and dates.

- Annual maximum already exhausted: You've used up this year's benefits. Fix: Wait until January 1st when your benefits reset, or pay out of pocket now.

- Out-of-network provider issues: Your plan doesn't cover non-network dentists or severely limits reimbursement. Fix: Find an in-network dentist for the procedure or accept the higher costs.

- Pre-authorization wasn't obtained: Your dentist did the work without getting advance approval. Fix: Submit everything after the fact with complete documentation. Some insurance companies won't budge on this requirement—read your policy carefully.

How to appeal:

Start with a first-level appeal to the insurance company's review department. Your dentist should write a detailed letter explaining medical necessity—include clinical findings, X-rays, and photos. Point to sections in your policy that support approval.

File appeals within whatever deadline appears in your denial letter (usually 30-180 days). Make sure you list your member ID, the claim reference number, and service dates. Copy everything before you send it.

First appeal rejected? Request a second-level review. Depending on your state, insurers might have to provide external review from independent dental consultants who don't work for the company. This takes 30-60 days typically.

The majority of crown denials happen because the paperwork is incomplete—not because coverage doesn't exist. When dentists submit thorough clinical documentation with clear imaging that shows why the crown is necessary for function or preventing tooth loss, approval rates jump dramatically

— Dr. Patricia Chen

Other options if appeals fail:

- In-house payment plans: Most dental offices let you spread payments over 6-12 months with no interest

- HSA or FSA funds: Use pre-tax money from Health Savings Accounts or Flexible Spending Accounts, effectively reducing your cost by 20-30% through tax savings

- Dental discount plans: Pay $100-$200 annually for membership that gets you 20-40% discounts at participating offices

- Dental schools: Students supervised by licensed faculty perform treatment at 30-50% below regular fees (expect longer appointments and multiple visits)

- Charitable clinics: Free or sliding-fee care based on income—wait lists can stretch for months

How to Maximize Your Dental Insurance Benefits for Crown Treatment

Smart planning cuts your out-of-pocket expenses and eliminates billing surprises.

Timing strategy across calendar years: Need multiple crowns? Split them between December and January. You're tapping two separate years of annual maximums. Instead of one $1,500 limit, you've got $3,000 total to work with.

Always get pre-treatment estimates: Ask your dentist to submit the treatment plan for pre-authorization before scheduling work. Insurance responds with exactly what they'll pay—no surprises when the bill arrives.

Learn to read EOB statements: Explanation of Benefits documents spell out what insurance paid, what you owe, and the reasoning behind it. Check them carefully. Common mistakes include charges applied to wrong calendar year, deductible calculations that don't match your records, or incorrect coverage percentages. Catch errors fast and dispute them immediately.

Material selection strategy: If insurance only pays porcelain-fused-to-metal rates, upgrading to zirconia means covering the $200-$500 difference yourself. For back molars nobody sees, accepting the fully-covered option saves significant money.

Dual coverage coordination: Have insurance through your employer plus your spouse's plan? Coordinate benefits. The primary insurance pays first, secondary insurance might cover some remaining balance. Done right, your out-of-pocket drops close to zero—though combined payments can't exceed 100% of the total bill.

Use in-network dentists: The fee gap between in-network and out-of-network dentists often hits $400-$800 per crown. If your regular dentist isn't in-network, switching providers for major work makes financial sense.

Time major work before job changes: COBRA continuation coverage runs $400-$600 monthly. Switching employers? Schedule needed crowns before your current coverage ends. Beats paying COBRA rates or sitting through a new waiting period.

Ask about alternative materials: If insurance denies your preferred material, ask whether they'd approve something else. Sometimes switching from zirconia to porcelain-fused-to-metal gets immediate approval.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Frequently Asked Questions About Dental Crown Insurance Coverage

What you'll actually pay for a crown with insurance depends on way more than the coverage percentage printed in your benefits booklet. Annual maximums, material upgrade charges, replacement timing rules, and in-network requirements all slice away at that advertised coverage figure.

Most insured patients end up paying $450-$1,200 out of pocket per crown. Without insurance, costs range from $800-$2,500. The gap shows insurance provides real value—but only when you understand how to work the system.

Get pre-authorization before scheduling treatment. Stick with in-network providers when possible. Time expensive work around calendar years to maximize benefits. When claims get denied, fight back with detailed documentation and persistence through the appeals process.

Your first crown or your fifth, knowing these cost factors and coverage rules means you control both your dental health and your checking account balance. No more surprise bills three weeks after the appointment.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.