Close-up of a teenager smiling with metal braces on teeth, dental insurance document and pen on a table in a bright orthodontic office

Dental Insurance That Covers Braces Guide

Shopping for dental insurance that covers braces feels like navigating a maze blindfolded. You're looking at a potential $6,000 bill, hoping your insurance will shoulder some of that burden. Maybe you're planning ahead for your 10-year-old's future orthodontic needs, or you're an adult finally ready to fix that crowded smile.

Here's what most people discover too late: their dental plan doesn't cover orthodontics at all. Others find out their "coverage" amounts to maybe $1,000 toward a $5,500 treatment. That's a brutal surprise when you're already sitting in the orthodontist's chair.

About 40% of dental insurance policies sold today completely exclude braces. Another chunk includes coverage so limited it barely makes a dent. The gap between what you expect insurance to pay and what it actually pays can hit $3,500 or more.

We're going to walk through which plans actually deliver meaningful coverage, how the whole orthodontic benefits system really works, and what your options look like when insurance comes up short.

Does Dental Insurance Cover Braces?

Sometimes yes, often no, and when they do—expect hoops to jump through.

Insurance companies split orthodontic treatment into two buckets. One bucket holds medically necessary corrections. The other? Cosmetic improvements they won't touch with a ten-foot pole.

The medical necessity hurdle shapes everything about your coverage approval. Let's say your kid has a severe underbite that's messing with their ability to chew properly. That's getting approved. But slightly crooked front teeth that function fine? The insurer calls that cosmetic and denies your claim.

Your orthodontist becomes your advocate here, submitting documentation that proves functional problems exist. They'll send X-rays, photographs of the teeth from multiple angles, and a detailed letter explaining why this isn't just about looking better in photos. Insurance reviewers scrutinize every word.

Age creates another brick wall. Scan through most policies and you'll find coverage that stops dead at age 18, maybe 19. The insurance industry still operates on this 1970s assumption that only kids need braces, ignoring the reality that millions of adults get orthodontic treatment annually.

Watch out for these common exclusions:

- Any treatment you started before your coverage kicked in

- Replacing retainers you lost at a restaurant

- Round two of braces after previous orthodontic work

- Adjustments that serve purely aesthetic goals

- Specific appliance types—some policies reject lingual braces or clear aligner systems outright

Your policy documents bury the orthodontic section in weird places. I've seen it listed under "Specialized Services," "Additional Coverage Options," or even lumped into a miscellaneous category. Don't just skim the main benefits summary.

How Dental Insurance Coverage for Braces Works

Orthodontic benefits operate on a completely different planet than your regular dental coverage. Your cavity fillings and cleanings reset each January 1st. Braces coverage? That's a one-and-done lifetime maximum that never replenishes.

Here's how the money actually flows:

The deductible question trips people up constantly. Most orthodontic benefits skip the deductible entirely—you don't pay that $50 or $100 upfront before coverage starts. But I've seen policies that force you to satisfy your annual dental deductible first. You need to verify this specific detail in writing.

Coverage percentages land anywhere from 25% to 50% of total treatment costs. The 50% rate shows up most often in solid employer plans covering kids. Adult coverage, assuming it exists at all, typically maxes out around 30% or 35%.

Pre-authorization isn't optional—it's mandatory. Your orthodontist submits the entire treatment plan to your insurance company before placing a single bracket. The insurer reviews whether treatment meets their medical necessity standards, then either approves your claim with a specific dollar amount or denies it outright. Jump the gun and start treatment without this approval? You've just voided your coverage completely.

The payment schedule varies wildly between insurers. Some pay your orthodontist directly in monthly or quarterly installments throughout your 18-month treatment. Others reimburse you after you've already paid the orthodontist yourself. This second scenario means fronting thousands of dollars while waiting for reimbursement checks.

Author: Daniel Mercer;

Source: ladylesliebelize.com

Waiting Periods and Eligibility Requirements

Here's where timing becomes critical. Most policies with orthodontic benefits force you to wait anywhere from six months to two full years before you can file a claim. Insurance companies built these waiting periods specifically to stop people from buying coverage only when they need expensive work done.

Twelve months represents the middle ground most insurers choose. Throughout that entire year, you're paying monthly premiums but can't access orthodontic benefits. Meanwhile, routine stuff like cleanings and fillings usually become available immediately or after just three months.

Employer plans offer an escape hatch. Enroll during your first eligibility window—typically within 30 days of starting a new job—and many carriers waive the waiting period entirely. The same waiver often applies during annual open enrollment periods. Switch jobs mid-year and move from one employer plan to another? You might bypass the waiting period, though this depends on the specific carrier.

Individual plans you buy on your own almost never waive these waiting periods. No exceptions, no shortcuts. This timing makes them practically worthless if your kid needs braces within the next year.

Some strategic families think ahead. They purchase coverage when their child is seven or eight, letting that waiting period expire while orthodontic issues are still developing. By age 11 or 12, when treatment actually begins, coverage stands ready.

Lifetime Maximum Limits Explained

This lifetime maximum number represents every dollar your insurance will ever pay for orthodontics per covered person. Exhaust this benefit and you're permanently out of orthodontic coverage under that policy.

Real-world lifetime maximums I've seen:

- $1,000 appears in budget-tier plans

- $1,500 shows up in average employer offerings

- $2,000 comes with better corporate benefit packages

- $2,500 to $3,000 exists only in premium plans (these are rare unicorns)

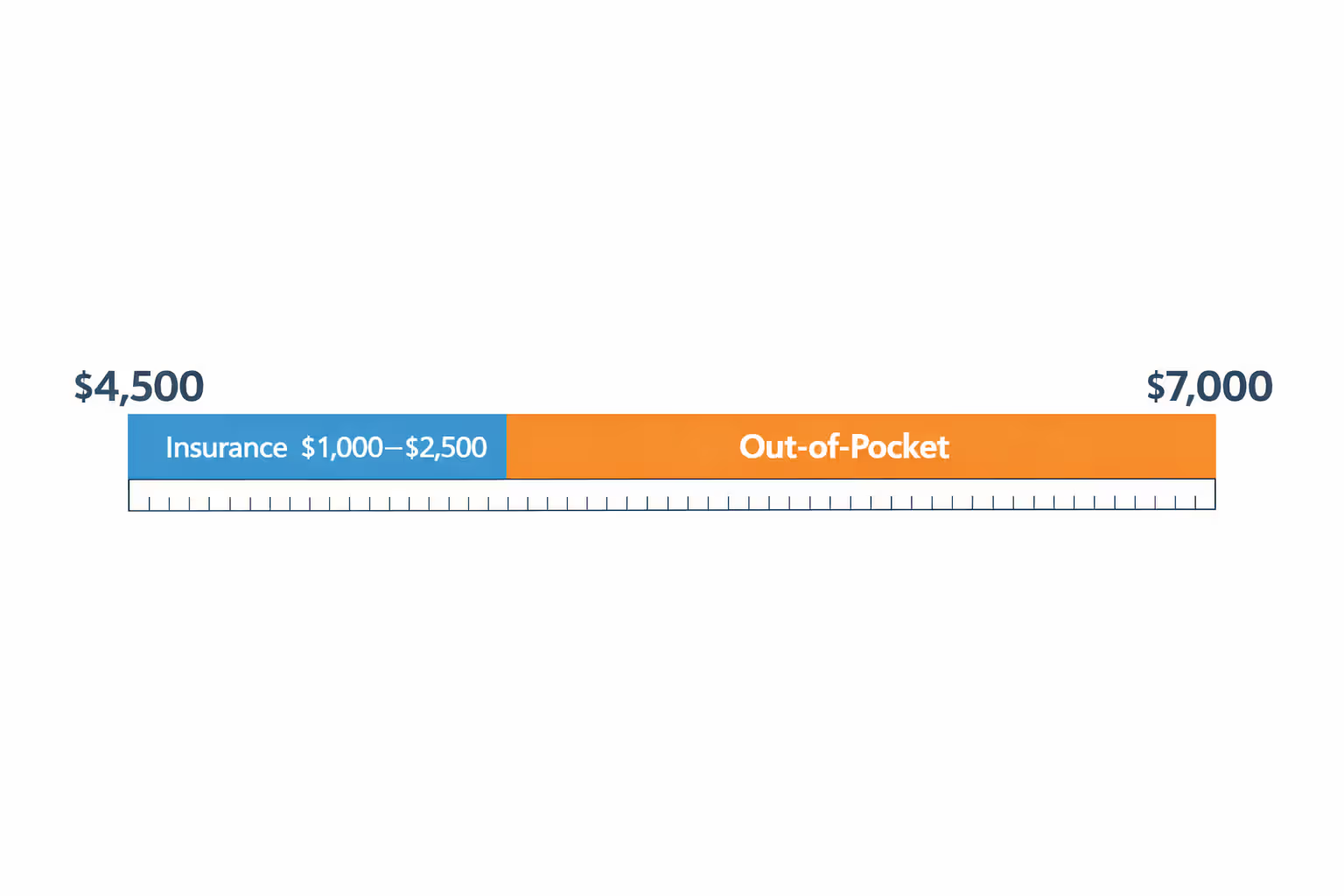

Stack those numbers against actual orthodontic costs running $4,500 to $7,000. Even with a generous $2,000 maximum covering half of a $4,000 treatment, you're still cutting a check for two grand.

This maximum doesn't reset when you switch insurance companies. However—and this matters for families—each person covered under your policy gets their own separate lifetime maximum. Three kids on your family plan with $1,500 per person means $4,500 in total potential benefits, though each child can only claim their individual $1,500.

I've watched parents make a costly strategic error. They use their child's entire lifetime maximum on Phase 1 interceptive treatment around age 8—maybe an expander or partial braces. Then at age 13, when comprehensive braces become necessary, that benefit is gone forever. Coordinate carefully with your orthodontist to maximize when and how you use this one-time benefit.

Author: Daniel Mercer;

Source: ladylesliebelize.com

Types of Dental Insurance Plans That Cover Braces

Plan structure matters as much as whether orthodontic coverage exists at all. Two policies might both advertise braces coverage, but deliver wildly different value.

PPO plans provide maximum flexibility. You can walk into any orthodontist's office in the country. Staying in-network cuts your costs significantly, but out-of-network treatment still receives partial coverage. Typical PPO orthodontic benefits hit 50% of costs up to the lifetime cap. No referrals needed, no permission required—just get pre-authorization and go.

HMO plans trade flexibility for lower premiums. You're locked into a specific network of providers. Pick an orthodontist from the approved list or pay 100% yourself. HMO orthodontic coverage usually runs 35% to 40% rather than 50%, but monthly premiums run $30 to $50 less than comparable PPOs. Whether this tradeoff works depends on whether quality orthodontists participate in that HMO network near you.

Discount dental programs aren't actually insurance—they're membership clubs. Pay $100 to $250 annually for access to discounted rates at participating providers. Braces discounts typically range from 10% to 30% off standard fees. These work well combined with limited insurance or when you're completely uninsured, but don't mistake them for comprehensive coverage.

Indemnity plans have mostly vanished from the modern market, but some still exist. Visit any provider anywhere without network restrictions. You pay the orthodontist upfront, then file paperwork for reimbursement. Orthodontic benefits follow the same percentage and lifetime cap structure as PPOs.

Employer-Sponsored Dental Plans

Group coverage through your job represents your strongest shot at meaningful orthodontic benefits. Employers negotiate package deals and benefit levels individuals can't access.

Recent benefits surveys show roughly 60% of employer dental plans include orthodontic coverage to some degree. Quality varies dramatically. Small businesses—we're talking under 50 employees—often provide basic plans with $1,000 lifetime caps. Large corporations with 500+ employees might offer $2,000 to $2,500 maximums.

Why employer plans win:

- Waiting periods get shortened or eliminated entirely

- Premiums stay lower through group negotiating power

- Lifetime maximums trend higher

- Provider networks include better orthodontists

Check whether your employer offers tiered plan options. The base-level plan might exclude orthodontics completely while the premium tier (costing more monthly) includes substantial coverage. Do the math: a premium plan costing $40 extra per month adds up to $480 annually, but if it includes $1,800 in orthodontic benefits you'll actually use, you're coming out $1,320 ahead.

One trap catches families regularly: dependent coverage definitions vary. Some plans terminate dependent benefits at age 18. Others extend to 19. Some stretch to age 26 for full-time students. Your 17-year-old starting braces needs to remain covered through treatment completion—usually 18 to 24 months. Verify their coverage won't expire mid-treatment.

Individual and Family Plans

Buying dental insurance outside of an employer presents challenges for orthodontic coverage. Benefits are harder to locate and less generous when you find them.

Most individual market plans either skip orthodontics entirely or offer minimal benefits—think $500 to $1,000 lifetime maximums. Those 12 to 24-month waiting periods make immediate treatment impossible.

Monthly premiums for individual plans including orthodontic coverage run $45 to $90 for single coverage, $90 to $180 for family coverage. Calculate the full cost across the waiting period plus treatment duration against the actual benefit received.

Let me run real numbers: A family plan costs $130 monthly with a $1,000 orthodontic benefit and requires 12 months waiting. Over three years (waiting period plus two-year treatment), you'll spend $4,680 in premiums to collect $1,000 in orthodontic benefits plus whatever routine dental care you use. Whether this pencils out depends heavily on how much you'll use those cleanings, fillings, and other basic services.

Marketplace plans through healthcare.gov sometimes bundle pediatric dental coverage including orthodontics, particularly for children under 19. These plans enforce strict medical necessity guidelines but can deliver real value.

Dental Insurance That Covers Braces for Adults

Adult orthodontic coverage is the needle in the haystack. Most policies either explicitly state "orthodontic benefits limited to dependent children under age 19" or remain silent on age, covering anyone meeting medical necessity criteria—but with restrictive age cutoffs that eliminate most adults anyway.

When adult coverage actually exists, prepare for:

- Reduced coverage percentages dropping to 25% to 35% instead of 50%

- Tougher medical necessity standards requiring extensive documentation

- Smaller lifetime maximums hovering around $1,000 to $1,500

- Limited appliance approval—traditional metal braces only, clear aligners denied

Medical necessity requirements tighten considerably for adults. Insurers demand concrete evidence that misalignment creates functional impairment: documented TMJ disorders, measurable difficulty chewing specific foods, excessive tooth wear visible on X-rays, or diagnosed speech impediments. Wanting straighter teeth for confidence or appearance won't clear the bar, regardless of severity.

Clear aligner systems create a coverage paradox. Some insurers categorize products like Invisalign as inherently cosmetic, denying claims even when they'd approve traditional braces for the identical condition. This forces an uncomfortable choice: accept conspicuous metal brackets to access insurance coverage, or pay completely out-of-pocket for discreet clear aligners.

Your employer plan offers the best odds for adult orthodontic coverage. Pull up your Summary of Benefits and scan specifically for age-related restrictions. Language stating "orthodontic benefits available to all covered members regardless of age" or "no age restrictions apply to orthodontic coverage" signals adult inclusion.

A handful of specialized insurers focus on adult orthodontic coverage, but these policies remain rare and often expensive relative to benefits provided. Run the full calculation: premium costs throughout the waiting period plus entire treatment duration versus the total benefit amount received.

Alternative strategy worth considering: maximize FSA (Flexible Spending Account) or HSA (Health Savings Account) contributions if your employer offers them. Pre-tax dollars effectively create 20% to 35% "coverage" through tax savings depending on your bracket. A $5,000 orthodontic bill paid with HSA funds saves $1,250 to $1,750 in taxes.

Author: Daniel Mercer;

Source: ladylesliebelize.com

How to Find Dental Insurance for Braces

Shopping for orthodontic coverage demands systematic detective work. Marketing materials spotlight coverage while burying limitations in fine print.

Step 1: Audit your existing coverage thoroughly. If you currently have employer dental insurance, request the complete policy document—not just the two-page benefits summary. Hunt for:

- "Orthodontia" or "Orthodontic Services" section (might be buried deep)

- Exact lifetime maximum dollar amounts per person

- Any age-based restrictions or cutoffs

- Precise waiting period language and duration

- Percentage of treatment costs covered

- Pre-authorization procedures and timelines

Step 2: Deploy specific questions. When comparing plans or interrogating insurance representatives, use these exact questions to cut through vague marketing speak:

- "What is the exact lifetime maximum orthodontic benefit per covered person?"

- "Does orthodontic coverage impose a separate waiting period from general dental services?"

- "Are adults covered for orthodontic benefits, or only dependent children under a specific age?"

- "What percentage of total orthodontic treatment costs does this plan cover?"

- "Does your plan cover clear aligner systems like Invisalign, or only traditional metal braces?"

- "What's required for pre-authorization, and how long does approval typically take?"

Step 3: Calculate total cost, not just monthly premiums. Build this complete picture:

- Monthly premium × total months from enrollment through treatment completion

- Waiting period duration in months

- Estimated total treatment cost minus insurance benefit

- Your resulting out-of-pocket responsibility

A plan charging $55 monthly with a $1,500 orthodontic benefit might cost less overall than a $38 monthly plan offering only a $1,000 benefit, once you factor in treatment timing.

Step 4: Verify provider network quality. For HMO or PPO plans under consideration, confirm that reputable orthodontists in your area actually participate. Call orthodontic offices directly and ask which insurance plans they accept. Some high-quality providers refuse certain plans due to low reimbursement rates or bureaucratic nightmares.

Step 5: Excavate exclusions buried in fine print. Search for clauses that void coverage:

- Treatment initiated before your coverage effective date

- Services from out-of-network providers (critical for HMOs)

- Specific appliance types the policy excludes

- Conditions categorized as cosmetic rather than medical

One frustrated parent I spoke with discovered their plan excluded "interceptive orthodontics"—which included their child's palatal expander. The orthodontist deemed this $1,900 device medically essential, but insurance refused payment despite advertising orthodontic benefits prominently.

Author: Daniel Mercer;

Source: ladylesliebelize.com

Alternatives When Dental Insurance Won't Cover Braces

When insurance coverage disappoints or doesn't exist, several strategies can reduce your orthodontic financial burden.

In-house payment plans from orthodontists represent standard practice. Most offices provide financing directly with zero interest if you pay throughout treatment duration—typically 18 to 24 months. A common arrangement: $1,200 down payment, then $175 monthly for 22 months. Many orthodontists don't even run credit checks for these payment plans.

Health Savings Accounts and Flexible Spending Accounts let you use pre-tax income for orthodontic expenses, generating savings of 20% to 35% based on your tax bracket. Braces costing $5,000 paid through HSA funds saves $1,250 to $1,750 compared to using after-tax income. FSA funds operate on use-it-or-lose-it annual deadlines, so plan contribution amounts carefully across multiple treatment years.

Orthodontic discount memberships through organizations like Careington or DentalPlans.com charge $100 to $200 yearly for 10% to 30% fee reductions at participating providers. If treatment costs $5,800 and you receive 20% off, you're saving $1,160—substantially more than the membership fee. Confirm your preferred orthodontist participates before purchasing membership.

University dental schools provide braces at 30% to 50% below private practice rates. Orthodontic residents perform treatment under faculty supervision, which extends appointment times and overall treatment duration. Quality generally remains high, though convenience suffers. Schools like University of Pennsylvania, University of Michigan, and UCLA operate respected orthodontic programs.

Third-party medical financing through CareCredit, LendingClub, or similar lenders offers loans designed specifically for healthcare expenses. Interest rates span from 0% promotional periods to 15%+ depending on your credit profile. Read terms meticulously—deferred interest promotions can backfire painfully if you don't eliminate the balance before the promotional period expires, triggering retroactive interest charges.

Supplemental employer benefits sometimes include orthodontic discounts or add-on coverage available during open enrollment. These extras don't always get advertised prominently, so review every available benefit option thoroughly.

One cost management tactic: ask your orthodontist whether extending treatment slightly to spread payments across additional months would reduce your monthly amounts. Most will accommodate this if it secures your commitment as a patient.

Most patients don't realize orthodontic benefits function completely differently from regular dental coverage. I've watched families get blindsided by lifetime maximums and waiting periods because they didn't ask the right questions before starting treatment. Always secure pre-authorization and a detailed breakdown showing what insurance will actually pay versus what you'll owe out-of-pocket. That conversation up front prevents financial surprises down the road

— Dr. Jennifer Martinez

Frequently Asked Questions About Braces and Dental Insurance

Dental insurance that covers braces can slice thousands of dollars off orthodontic expenses, but coverage remains far from universal or straightforward. The financial gap between a plan offering solid orthodontic benefits and one offering nothing can reach $4,000 or more—money that stays in your pocket or disappears.

Before committing to treatment, nail down your exact coverage details: lifetime maximum amounts, waiting period duration, age-based restrictions, and pre-authorization requirements. Don't accept verbal assurances from insurance representatives; demand documentation in writing that you can reference later.

If your current coverage disappoints, explore alternatives including orthodontist payment plans, tax-advantaged HSA or FSA accounts, discount membership programs, or university dental school clinics. Many families successfully afford braces by layering modest insurance benefits with these supplemental strategies.

The costliest mistake people make? Assuming coverage exists when it doesn't, or beginning treatment before understanding their complete financial obligation. Time invested upfront researching and comparing options pays dividends measured in thousands of dollars.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.