Adult patient sitting in a modern dental chair reviewing a treatment plan document with a dentist standing nearby in a bright clinical office

Dental Insurance for Adults Guide

Adult dental coverage isn't like health insurance—and that disconnect trips up nearly everyone who buys it for the first time. You're dealing with yearly benefit caps that haven't budged since the early 2000s (still hovering around $1,500-$2,000 max), mandatory waiting windows before big-ticket procedures get covered, and a labyrinth of exclusions that'll leave you footing thousands in bills if you haven't done your homework.

Here's the reality: most people buy dental coverage thinking it'll handle cleanings and bail them out when something goes wrong. It handles the cleanings fine. But that emergency root canal or the crown you desperately need? Your plan maxes out fast, often before you've even finished addressing what's wrong. A typical crown runs $1,200-$1,800 in most markets—even with 50% coverage, you're paying $600-$900 per tooth. Need two crowns in one year? You've likely exhausted your annual limit entirely. Knowing these constraints before you commit saves you from nasty financial surprises down the road.

What Dental Insurance for Adults Covers

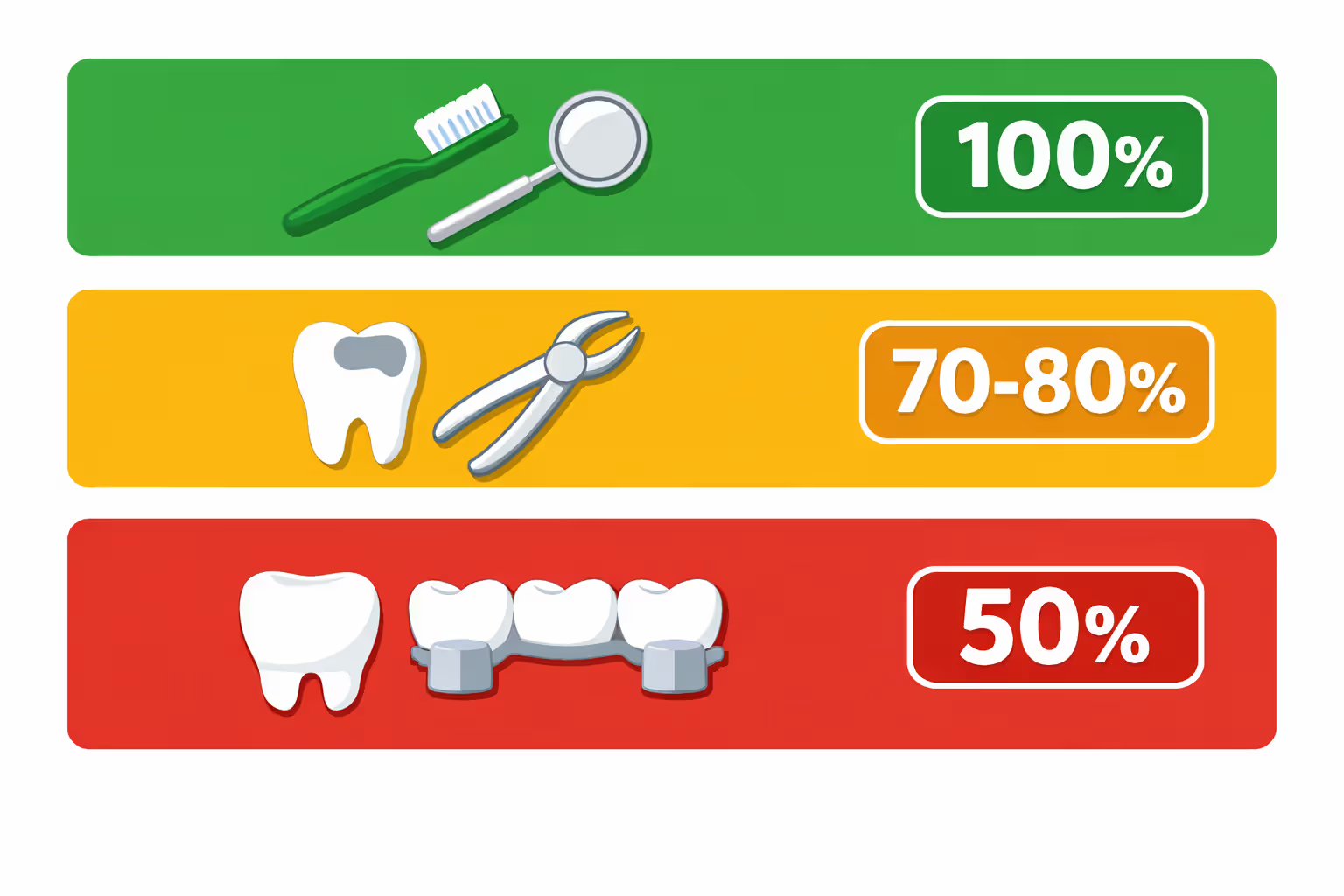

Adult dental plans break down services into three buckets. Preventive work—your twice-yearly cleanings, routine exams, standard X-rays—gets full coverage without any deductible eating into it first. The "twice-yearly" part matters because that's where most policies draw the line; if your hygienist recommends a third or fourth cleaning due to gum issues, you're covering that visit yourself.

Basic services like fillings, routine extractions, and gum maintenance treatments typically get 70-80% coverage once you've cleared your deductible threshold. Major work—root canals, crowns, bridges, partial dentures—usually sits at 50% coverage. Here's where things get dicey: that percentage only helps you until you slam into your yearly maximum. Say you need a $1,400 crown and your plan theoretically covers half. Sounds like you're paying $700, right? Except if you've already burned through $1,000 of your $1,500 annual cap on previous procedures, the plan only kicks in $500 toward that crown. You're now responsible for $900 instead of $700.

Your deductible resets every January 1st—count on paying $50-$150 out-of-pocket each year before your plan contributes anything toward basic or major procedures. Preventive services bypass this hurdle completely, which is why scheduling those cleanings matters even if you're trying to avoid the dentist.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Waiting periods create another headache. Sure, preventive coverage kicks in immediately. But need a filling? Many plans make you wait six months from your enrollment date. Major procedures often require a full year before coverage begins. Orthodontic work—if your plan even covers it for adults—can have two-year waiting periods. Planning to buy insurance because you already know you need that root canal? You'll be paying premiums for months (possibly a year) while covering the procedure entirely out-of-pocket anyway.

Network structures determine which dentists you can visit without financial penalties. PPO arrangements give you the broadest selection of providers. You can see out-of-network dentists if you want, though you'll get reimbursed at a lower percentage. HMO-style plans slash your premiums and eliminate deductibles, but you're locked into choosing one primary dentist and securing referrals before seeing specialists. Indemnity plans—increasingly rare in 2026—let you visit any dentist you like, but you're fronting the entire cost upfront and filing reimbursement paperwork yourself.

Does Dental Insurance Cover Braces and Orthodontics for Adults

Sometimes yes, but prepare for disappointment. Most dental plans either flat-out exclude orthodontic treatment for adults or bury the coverage under so many restrictions that you'll still be financing the bulk of your braces out-of-pocket.

When coverage exists, you're looking at 50% reimbursement capped by a lifetime maximum somewhere between $1,000-$2,000. Adult braces run anywhere from $3,000 on the low end to $8,000+ depending on your location and case complexity. Even maxing out that $2,000 lifetime cap only covers 15-30% of total treatment expenses. And "lifetime" means exactly that—exhaust this benefit once and you'll never see orthodontic coverage from that carrier again, even if you switch employers and re-enroll years later.

Age restrictions catch people off-guard constantly. Plenty of policies advertise "orthodontic benefits" in their marketing materials without making it obvious that those benefits only apply to dependent children under 19. You won't realize adults are excluded until you're deep into the fine print or, worse, when you file a claim after starting treatment.

Waiting periods for orthodontic coverage stretch 12-24 months typically. Buy a plan in February 2026? Don't expect any orthodontic reimbursement until February 2027 at the earliest, possibly not until February 2028. Since most orthodontic treatment spans 18-24 months, you're committing to a 3-4 year timeline between buying coverage and completing treatment that began after your waiting period ended.

Author: Ashley Whitford;

Source: ladylesliebelize.com

What Dental Insurance Covers Orthodontics for Adults

Genuine adult orthodontic coverage typically comes through large employers or union-negotiated benefits packages. Individual plans you'd buy through healthcare marketplaces or directly from insurers? They almost never include meaningful adult orthodontic benefits.

Guardian, Delta Dental, and Cigna occasionally offer plans with adult orthodontic provisions, but availability varies wildly depending on your state and whether you're buying individual coverage versus getting employer-sponsored benefits. Don't assume—you need to explicitly verify that adults qualify, not just children. The customer service rep should confirm in clear language whether a 35-year-old enrollee gets orthodontic coverage.

Discount dental programs—which aren't actually insurance—sometimes deliver better value for orthodontic treatment. You pay a flat yearly fee (typically $100-$200) that unlocks negotiated discounts of 20-40% across all services, orthodontics included. No waiting periods. No lifetime maximums. No claims to file. If you need braces and minimal other dental work, paying the discount plan fee plus the reduced treatment cost often beats insurance premiums plus the uncovered portion of treatment.

How Much Coverage to Expect for Adult Braces

Set realistic expectations here. Your plan says it covers orthodontics at 50% with a $1,500 lifetime cap, and you're choosing treatment costing $5,000. Math doesn't work the way you'd hope—insurance pays $1,500 total, leaving you with $3,500 to cover. That "50% coverage" only applies until you hit the lifetime ceiling.

Many orthodontists run in-house payment arrangements that split costs across 12-24 months interest-free. This often provides more actual financial breathing room than insurance coverage, especially once you factor in premiums paid during waiting periods. Calculate total outlay: paying $50 monthly in premiums for 24 months before coverage activates equals $1,200. Then you receive $1,500 in benefits. Net gain? Only $300 after those two years of premium payments.

FSAs and HSAs let you pay orthodontic expenses with pre-tax dollars. Depending on your tax bracket (22-35% for most people), that's like getting an automatic 22-35% discount on treatment. This tax advantage frequently exceeds the actual benefit you'd extract from dental insurance orthodontic coverage.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Free and Low-Cost Dental Care Options for Adults

Free dental care for adults exists, though eligibility and availability swing wildly based on where you live. Your main options: Medicaid (if your state offers decent adult dental benefits), community health centers, and dental school clinics.

Whether Medicaid covers your dental work depends entirely on which state you're in. Right now in 2026, 19 states offer extensive adult dental benefits through Medicaid—preventive cleanings all the way through crowns and root canals. Another 15 states provide limited benefits, usually just emergency extractions when you're in severe pain. The remaining states? Emergency-only coverage, meaning they'll yank a painful tooth but won't fill the cavity that's causing your pain.

Income thresholds for Medicaid hover around 100-138% of federal poverty level in expansion states. For 2026, that translates to roughly $15,000 yearly for a single adult or $31,000 for a family of four. States that didn't expand Medicaid often set even lower income cutoffs or restrict adult Medicaid eligibility to specific groups like pregnant individuals or those with qualifying disabilities.

HRSA-funded community health centers work on sliding-fee scales tied to your income. These centers can't turn you away based on insurance status or ability to pay. You'll still owe something, but maybe $30-$50 for a cleaning instead of $150-$200 at private practices. Find them by searching "FQHC" plus your city name, or check the HRSA website's center locator tool.

Dental school clinics slash costs 30-50% compared to typical market rates. You're getting treated by dental students who work under direct faculty supervision, which means appointments run longer—sometimes double a standard private practice visit. Quality stays solid because instructors verify every step students take, but you need patience and scheduling flexibility.

Mission of Mercy events and similar charitable clinics offer completely free care on specific dates, usually operating first-come-first-served. These events might treat 500+ patients in a single day, providing extractions, fillings, and cleanings at zero cost. Local dental societies often coordinate these, or search "free dental day" plus your county name to discover upcoming events.

Donated Dental Services connects low-income seniors and permanently disabled adults with volunteer dentists providing free comprehensive treatment. You need to qualify through permanent disability status, age 65+, or medical inability to work, plus household income below 200% of poverty level. Unlike most programs, this covers major procedures like full dentures and bridge work, not just basic cleanings.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Dental Insurance Options for Young Adults

Twenty-somethings hit a weird coverage gap where childhood dental plans end, college wraps up, and career employment hasn't started yet. Thanks to ACA provisions, you can stick with a parent's dental coverage until you turn 26—doesn't matter if you're married, living across the country, or already eligible for employer coverage through your own job. This remains your cheapest option by far, though verify the plan covers services in your current state if you've relocated.

Employer dental benefits typically begin 30-90 days after your start date. That gap leaves you uninsured unless you arrange temporary coverage. Short-term dental discount plans bridge this window without locking you into long contracts.

Marketplace dental plans through healthcare.gov (or your state exchange) operate separately from medical coverage. You can purchase standalone dental insurance during open enrollment—November 1 through January 15 for most states—or within 60 days of losing previous coverage. Plans come labeled "high" or "low" coverage: high coverage means bigger premiums but smaller bills at each visit, while low coverage offers cheaper monthly costs but you're paying more out-of-pocket per appointment.

University student dental plans run about $150-$300 per year and deliver basic coverage with modest annual maximums ($500-$1,000 typically). These handle routine maintenance fine but won't adequately cover major procedures. Coverage terminates when you graduate or leave school, creating yet another gap you'll need to address.

COBRA lets you maintain your employer plan for 18 months after job separation, but you're paying the full premium plus a 2% administrative fee. Since employers usually cover 50-80% of dental premiums, your cost might triple overnight. COBRA only makes sense if you're mid-treatment and need to stay with your current dentist, or if you've got complex dental needs and you've already partially used a high annual maximum that you can't afford to lose.

How to Choose the Right Dental Plan

Start by writing down what dental work you actually need in the next 12 months. Haven't visited a dentist in three years and suspect you've got cavities lurking? Prioritize plans with brief waiting periods for basic procedures. Only need your twice-yearly cleanings? A cheaper premium with limited major coverage probably works fine.

Calculate your total yearly spend, not just monthly premiums. One plan charges $30 monthly ($360 per year) with a $100 deductible and $1,500 annual maximum. Another charges $50 monthly ($600 yearly) with no deductible and a $2,000 maximum. You need $1,800 worth of dental work this year. The cheaper-premium plan costs you: $360 (premiums) + $100 (deductible) + $900 (you pay 50% of $1,800 minus the portion over the $1,500 maximum, which leaves $300 uncovered) = $1,360 total. The pricier plan: $600 (premiums) + $800 (50% of $1,600, since the plan covers up to $2,000 maximum) = $1,400 total. Nearly identical despite the $240 premium difference.

Verify provider networks with your actual dentist. Call their office and ask which specific plans they're currently accepting, or cross-reference the insurer's online directory. Those directories frequently contain outdated information, so phone verification matters. Switching dentists to stay in-network might save money, but weigh that against the value of continuity with someone who knows your dental history and has established trust.

Annual maximums become critical when you need major work. That standard $1,500 ceiling hasn't increased meaningfully in two decades despite dental costs climbing steadily. Some carriers offer $2,000 or $2,500 maximums for an extra $10-$20 monthly—absolutely worth it if you're anticipating crowns, bridges, or multiple procedures within a calendar year.

If orthodontics interests you, scrutinize coverage terms carefully. Don't just read the marketing summary—dig into actual policy documents. Watch for language like "eligible dependents only" or specific age cutoffs. Call the insurance company directly and ask: "I'm 32 years old. Does this specific plan provide orthodontic benefits for me personally, and what's the lifetime maximum in dollars?" Get the answer in plain English before committing.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Common Mistakes When Buying Dental Insurance

The priciest mistake? Ignoring waiting periods. Someone discovers they need a root canal, buys insurance immediately, then learns they're waiting 12 months before coverage begins. You're paying premiums that entire year while receiving zero benefit for the procedure driving your insurance purchase. When you need immediate major work, paying cash or using a discount dental program often costs less than a full year of premiums plus whatever portion remains uncovered after waiting periods finally expire.

Assuming preventive means completely free catches many people. Most plans do cover preventive care at 100%—but they cap you at two cleanings yearly. Your dentist recommends quarterly cleanings because of gum disease? You're paying full freight for visits three and four. Some plans also classify certain X-rays as diagnostic rather than preventive, triggering your deductible and coinsurance.

People underestimate how fast annual maximums get exhausted. You need $4,000 in dental work and your plan maxes out at $1,500 annually. Even with insurance, you're covering $2,500 yourself. Many people discover afterward they should've skipped insurance entirely and negotiated cash-pay discounts directly with dentists, who often knock 15-30% off for immediate payment.

Comparing monthly premiums alone leads to poor value choices. A plan with $15 monthly premiums looks attractive until you discover the $200 deductible, 60% coverage for basic procedures (you pay 40%), and puny $750 annual maximum. You'd pay $180 yearly in premiums, $200 deductible, plus 40% of every basic procedure, while hitting that low maximum almost immediately.

Policy exclusions and limitations create ugly surprises. Lots of plans exclude cosmetic procedures, dental implants, or replacing lost dentures within five years of the previous set. Some restrict crowns to once every five years per individual tooth. Always read the "exclusions and limitations" section before purchasing.

Not reassessing your coverage needs each year means potential overpayment for benefits you're not using. Maybe you bought comprehensive coverage last year anticipating major work—work you've since completed. You could potentially downgrade to a lower-cost preventive-focused plan for the next year or two and bank the premium savings.

The biggest mistake I see patients make is buying dental insurance specifically for orthodontic treatment without reading the fine print. They assume '50% coverage' means the plan will pay half their braces cost, but they miss the lifetime maximum buried in the policy. When they discover their $6,000 treatment will only receive $1,500 from insurance after a two-year wait, they realize they would have saved money by skipping insurance entirely and negotiating a cash discount or payment plan with the orthodontist directly.

— Dr. Jennifer Martinez

Frequently Asked Questions About Adult Dental Insurance

Adult dental insurance operates differently than most people anticipate walking in. Annual maximums stuck in the early 2000s, waiting periods stretching across years, and exclusions targeting common needs like adult orthodontics—all these factors mean you'll frequently pay substantial out-of-pocket expenses despite carrying coverage.

Your best strategy depends on your specific circumstances. Need only routine preventive maintenance? A budget-friendly plan or even a discount dental program might outperform comprehensive insurance financially. Anticipating major work like crowns or bridges? Run total cost comparisons: premiums plus deductibles plus uncovered expenses versus negotiating direct cash-pay discounts with dentists (often 15-30% off for immediate payment).

For orthodontic needs specifically, traditional dental insurance rarely provides meaningful financial relief to adults. Lifetime maximums around $1,000-$2,000 combined with lengthy waiting periods mean you're covering most expenses yourself regardless. Discount dental programs, orthodontist-offered payment plans, or leveraging HSA/FSA tax advantages typically deliver superior results compared to standard insurance.

Before committing to any dental plan, calculate your complete annual outlay including premiums, deductibles, and anticipated out-of-pocket expenses based on your actual dental needs. Read complete policy documents—not just marketing summaries—verify your preferred dentist accepts the plan, and understand waiting periods for services you'll actually need. Sometimes your smartest dental insurance strategy is maintaining no insurance at all—just consistent preventive care paid directly and emergency savings set aside for unexpected procedures.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.