Patient sitting in a dental chair reviewing an insurance document with a dentist in a modern dental office

Does Dental Insurance Cover Pre Existing Conditions?

Walking into a dentist's office with a cracked molar or bleeding gums, you might assume that signing up for dental insurance will solve your financial worries. Unfortunately, dental coverage works differently than medical insurance under the Affordable Care Act. Most dental plans treat conditions that existed before your enrollment date with caution, building in restrictions that can delay coverage for months or even exclude certain treatments entirely.

Understanding how insurers handle pre-existing dental issues helps you make smarter decisions about when to enroll, which plan type to choose, and what alternatives might save you money while you wait for full benefits to kick in.

How Dental Insurance Treats Pre Existing Conditions

Dental insurance operates outside the protections that prevent medical insurers from denying coverage based on health status. Unlike your medical plan, which must cover chronic conditions from day one, dental insurers routinely impose waiting periods and exclusions for problems that developed before your effective date.

A pre-existing condition in dental terms means any oral health issue diagnosed or recommended for treatment before your coverage started. This includes obvious problems like cavities requiring fillings, teeth needing crowns, gum disease requiring deep cleaning, or missing teeth you want replaced. It also covers less obvious situations—a tooth your previous dentist noted as "watch" that now needs a root canal, or early-stage periodontal disease that progresses to require surgery.

Most insurers don't require a dental exam before enrollment, but they review treatment dates carefully. If your dentist's records show they identified a problem before your coverage began, the insurer may deny the claim even if you didn't know about the issue. Some plans include a "prior coverage" provision: if you maintained continuous dental insurance without a gap exceeding 63 days, they may waive or reduce waiting periods. This rewards people who kept coverage rather than waiting until problems arose.

Author: Ashley Whitford;

Source: ladylesliebelize.com

The industry justification centers on adverse selection—the risk that people would only buy coverage when facing expensive procedures, then drop it afterward. By imposing waiting periods, insurers ensure they collect premiums long enough to offset the cost of major treatments.

Common Waiting Periods and Coverage Restrictions

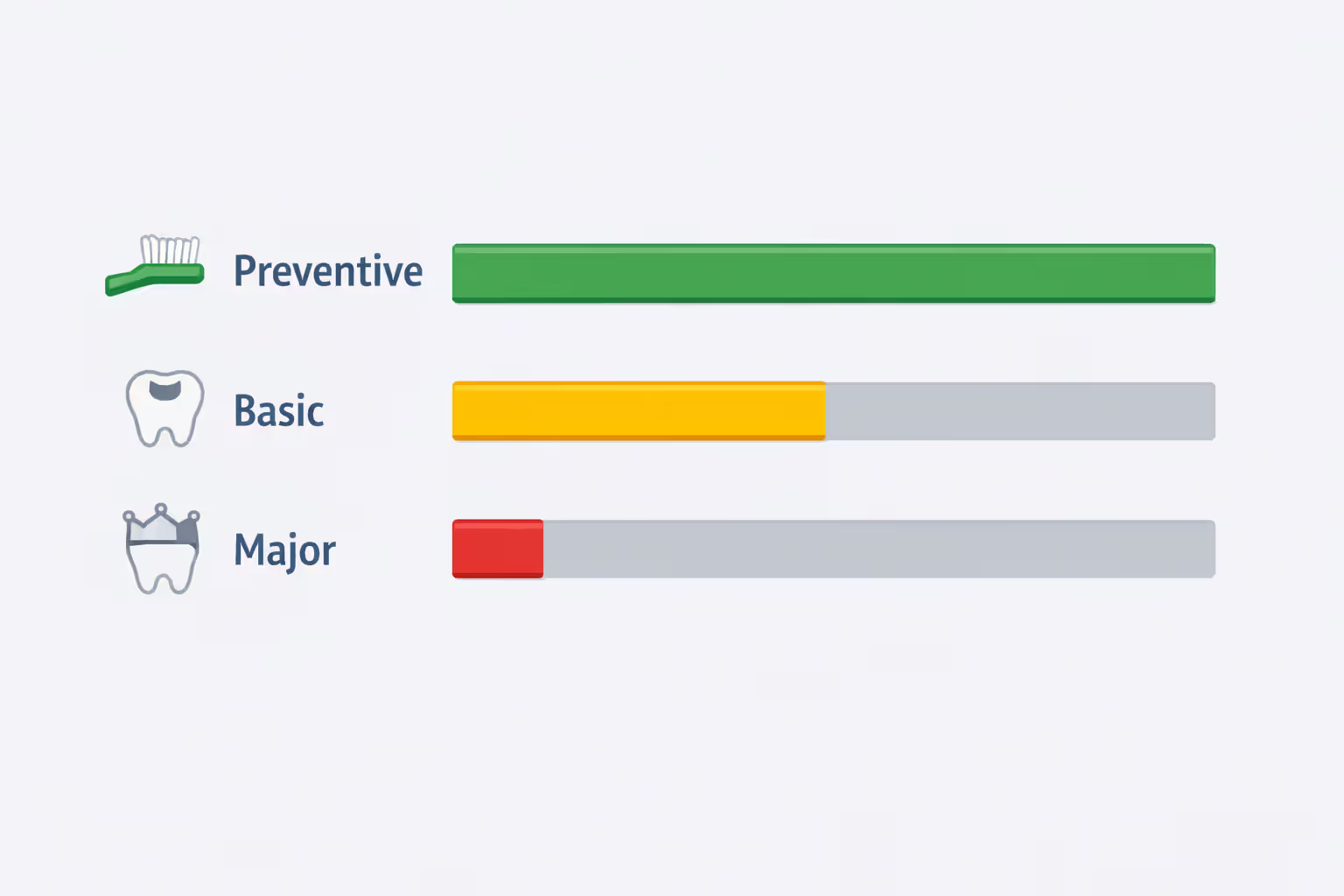

Dental plans typically structure waiting periods in tiers based on procedure complexity. Preventive services like cleanings and exams usually have no waiting period, allowing immediate coverage. Basic procedures—fillings, simple extractions, periodontal maintenance—commonly require a three to six-month wait. Major services such as crowns, bridges, dentures, and root canals often face 12-month waiting periods.

Some plans cap benefits during the first year. You might have a $1,000 annual maximum normally, but only $500 available in year one. This limitation hits hardest when you need multiple procedures to address neglected dental health.

Major Procedures vs. Preventive Care

The gap between preventive and major coverage creates a strategic opportunity. Enrolling in a plan immediately gives you access to cleanings, X-rays, and exams that can stabilize your oral health while you wait out the clock for major work. A hygienist can perform deep cleanings to slow gum disease progression. Your dentist might place temporary fillings to protect teeth until permanent restorations qualify for coverage.

This tiered approach means you're not completely without help during waiting periods. Regular preventive visits cost the plan relatively little but keep small problems from becoming emergencies. Patients who use these benefits strategically often reduce the total treatment needed once major coverage begins.

Missing Tooth Clause Explained

The missing tooth clause represents the strictest pre-existing condition exclusion in dental insurance. This provision states that the plan won't cover replacement of teeth lost or extracted before your coverage effective date. If you're missing a molar that was pulled two years ago, most plans won't pay for an implant, bridge, or partial denture to replace it—ever, not just during a waiting period.

Not every plan includes this clause, and some that do will waive it if you maintained prior coverage. Reading the fine print before enrollment matters enormously if you have missing teeth. Plans marketed through employers sometimes omit the missing tooth clause or apply it less strictly than individual market plans. Asking specifically about this restriction during enrollment prevents expensive surprises later.

Types of Dental Plans That Cover Pre Existing Conditions

Different plan structures handle pre-existing conditions with varying degrees of flexibility. Understanding these differences helps you choose coverage that aligns with your timeline and treatment needs.

Dental PPO plans (Preferred Provider Organizations) offer the broadest provider networks and typically impose standard waiting periods. You can visit any dentist, though staying in-network reduces your out-of-pocket costs. These plans work well if you can afford to wait 6-12 months for major procedures but want comprehensive coverage once waiting periods expire.

Dental HMO plans (Health Maintenance Organizations) require you to choose a primary dentist from a limited network and get referrals for specialists. They often feature lower premiums and sometimes shorter waiting periods than PPOs. However, treatment options may be more restricted, and switching dentists mid-treatment complicates continuity of care.

Discount dental plans aren't insurance at all—they're membership programs offering reduced fees at participating dentists. Because there's no insurance company paying claims, there are no waiting periods or pre-existing condition exclusions. You pay an annual membership fee (typically $100-$200 for individuals, $150-$350 for families) and receive 10-60% discounts on all procedures. For someone needing immediate major work, a discount plan often costs less than paying premiums during insurance waiting periods while receiving no benefits.

Medicare Advantage plans sometimes include dental benefits that traditional Medicare doesn't cover. These benefits vary widely by plan, but some offer coverage for pre-existing conditions with minimal or no waiting periods. If you're Medicare-eligible, comparing Advantage plans during open enrollment might yield better immediate coverage than standalone dental insurance.

Medicaid dental programs for adults vary dramatically by state. Some states offer comprehensive coverage with no waiting periods for pre-existing conditions, while others limit adult benefits to emergency extractions. Eligibility depends on income and other factors. If you qualify for Medicaid, it often provides the most generous coverage for pre-existing dental issues among all options.

How to Get Dental Coverage With Pre Existing Conditions

Author: Ashley Whitford;

Source: ladylesliebelize.com

Getting coverage that actually helps with existing dental problems requires strategic timing and knowing where to look.

Employer-sponsored plans during open enrollment represent your best opportunity. Group plans often waive or shorten waiting periods, especially for employees transitioning from another employer's coverage. Some employers offer multiple plan options—choosing the one with the shortest waiting periods for the procedures you need makes sense even if premiums run slightly higher.

Enrolling during a qualifying life event—marriage, birth of a child, loss of other coverage—lets you access employer coverage outside annual enrollment. If you're planning to marry someone with dental benefits, timing your enrollment to begin immediately after the wedding can be financially smart.

Individual market plans purchased directly from insurers typically enforce the strictest waiting periods and most commonly include missing tooth clauses. These plans make sense for self-employed individuals or those whose employers don't offer benefits, but shop carefully. Compare at least three plans, focusing on waiting period length, missing tooth provisions, and annual maximums.

State and local programs sometimes fill gaps for low-income adults. Community health centers often provide dental services on a sliding fee scale based on income, with no insurance required. Dental schools offer discounted treatment performed by supervised students—procedures take longer, but costs run 30-50% below private practice rates.

Dental savings plans work immediately and don't exclude pre-existing conditions. If you need $3,000 worth of dental work soon, paying a $150 annual membership fee plus discounted procedure costs often totals less than paying insurance premiums for a year while waiting periods expire, then paying coinsurance on top of that.

Financing options through companies like CareCredit offer payment plans for dental work. Some provide 0% interest if you pay the balance within 6-24 months. This approach lets you get treatment now and spread costs over time without waiting for insurance coverage to begin.

What Pre Authorization Means for Your Dental Treatment

Pre-authorization—sometimes called pre-determination or pre-treatment estimate—is a process where your dentist submits a treatment plan to your insurance company before performing the work. The insurer reviews the plan and tells you what they'll cover and what you'll owe out-of-pocket.

This process doesn't guarantee payment. The response is an estimate based on your current benefits and the information submitted. If circumstances change—you hit your annual maximum with other treatments, the procedure happens after your coverage ends, or the dentist's notes differ from what was submitted—the actual payment may differ.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Pre-authorization typically takes 2-4 weeks, though urgent cases can sometimes be expedited. For expensive procedures like crowns, bridges, or implants, getting pre-authorization prevents unpleasant financial surprises. You'll know before treatment whether the insurer considers it covered, medically necessary, or subject to waiting periods.

When dealing with pre-existing conditions, pre-authorization helps identify coverage gaps early. If the insurer denies coverage due to a waiting period or missing tooth clause, you can explore alternatives—delaying treatment, using a discount plan, or negotiating a payment plan with your dentist—before committing to expensive work.

Some plans require pre-authorization for procedures exceeding a certain cost threshold (commonly $300-$500). Proceeding without required pre-authorization can result in claim denial even for otherwise covered services. Your dentist's office typically handles this process, but confirming they've submitted the request and received approval protects you from billing disputes.

Comparing Dental Plan Types and Waiting Periods

| Plan Type | Preventive Coverage | Basic Procedures Wait | Major Procedures Wait | Missing Tooth Clause | Best For |

| PPO Insurance | Immediate | 3-6 months | 12 months | Often included | Long-term comprehensive coverage |

| HMO Insurance | Immediate | 3-6 months | 6-12 months | Sometimes included | Lower premiums, limited networks |

| Discount Plan | Immediate | Immediate | Immediate | Never applies | Immediate treatment needs |

| Medicaid | Immediate | Immediate | Immediate | Never applies | Low-income individuals (where available) |

| Medicare Advantage | Varies by plan | Varies by plan | Varies by plan | Varies by plan | Medicare-eligible seniors |

Real Costs Without Insurance Coverage

Understanding what dental procedures actually cost helps you evaluate whether waiting for insurance makes financial sense or if alternative approaches save money.

Crowns typically cost $800-$1,500 per tooth depending on material and location. With insurance after waiting periods, you might pay 50% coinsurance ($400-$750). Without insurance, some dentists offer 10-15% discounts for cash payment. A dental savings plan might reduce the cost to $600-$1,000.

Root canals range from $700 for front teeth to $1,500 for molars. Insurance usually covers 50-80% after basic or major waiting periods (often 6-12 months). Delaying a root canal risks infection spreading or tooth loss, potentially increasing total treatment costs. In this case, paying out-of-pocket or using a discount plan often makes more medical and financial sense than waiting.

Extractions cost $150-$400 for simple cases, $300-$800 for surgical extractions. Most insurance covers these at 70-80% after a 3-6 month waiting period. For an abscessed tooth causing pain, waiting isn't realistic. Emergency Medicaid in many states covers extractions even for adults with limited benefits.

Implants run $3,000-$6,000 per tooth including the post, abutment, and crown. Many dental plans exclude implants entirely or classify them as cosmetic. Plans that do cover implants typically pay only 50% after a 12-month waiting period and subject to annual maximums ($1,000-$2,000 for most plans). The math rarely favors waiting for insurance—you'd pay premiums for a year, then still owe thousands out-of-pocket.

Periodontal treatment for gum disease ranges from $500-$1,000 per quadrant for scaling and root planing (deep cleaning). Advanced cases requiring surgery cost $1,500-$8,000 depending on extent. Insurance typically covers 50-80% after waiting periods, but delaying treatment allows disease progression that increases long-term costs and risks tooth loss.

Patients often ask if they should wait for insurance coverage to begin before treating serious problems. My answer depends on the urgency. A cavity can sometimes wait six months with careful monitoring. An infection cannot. I've seen people lose teeth trying to save money by waiting for coverage, then face implant costs ten times higher than the original filling would have cost

— Dr. Jennifer Martinez

Frequently Asked Questions About Dental Insurance and Pre Existing Conditions

Dental insurance treats pre-existing conditions differently than medical coverage, with waiting periods and exclusions that can delay or prevent coverage for problems that existed before enrollment. Most plans impose 6-12 month waits for major procedures and may permanently exclude replacement of teeth lost before coverage began through missing tooth clauses.

Your best strategy depends on timing and urgency. Employer plans during open enrollment often offer shorter waiting periods and better terms than individual market policies. If you need immediate treatment, dental discount plans provide instant savings without waiting periods or exclusions, often costing less overall than paying insurance premiums while waiting for coverage to begin.

Preventive care typically starts immediately under most plans, giving you access to cleanings and exams that can stabilize oral health while you wait for major coverage. Using these benefits strategically—getting regular cleanings, addressing small cavities before they need crowns, managing gum disease progression—reduces total treatment costs.

Compare at least three options before committing: employer coverage if available, individual insurance plans, discount plans, and state programs like Medicaid. Calculate total costs including premiums, waiting period duration, and your expected out-of-pocket expenses. For many people facing significant pre-existing dental issues, a combination approach works best—enrolling in insurance for long-term protection while using a discount plan or payment plan to address immediate needs.

The key is matching your coverage choice to your actual situation rather than assuming insurance always provides the best value. Sometimes it does. Sometimes paying cash with a discount, financing through CareCredit, or seeking care at a dental school saves more money and gets you healthier faster.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.