Senior couple reviewing dental insurance documents at kitchen table with laptop

How Much Does Dental Insurance Cost for Seniors

Most Americans crossing into their retirement years face a frustrating reality: their teeth need more attention just as Medicare stops helping pay for it. Traditional Medicare won't cover your routine cleanings, and it certainly won't help when you need that $1,200 crown replaced. You're left sorting through standalone dental policies, Medicare Advantage plans with dental add-ons, and discount programs that aren't really insurance at all. What you'll actually spend depends on factors beyond the monthly premium—deductibles eat into your budget, annual caps limit what insurers will pay, and waiting periods can leave you paying premiums for a year before coverage kicks in for anything beyond basic cleanings.

Average Cost of Dental Insurance for Seniors in 2026

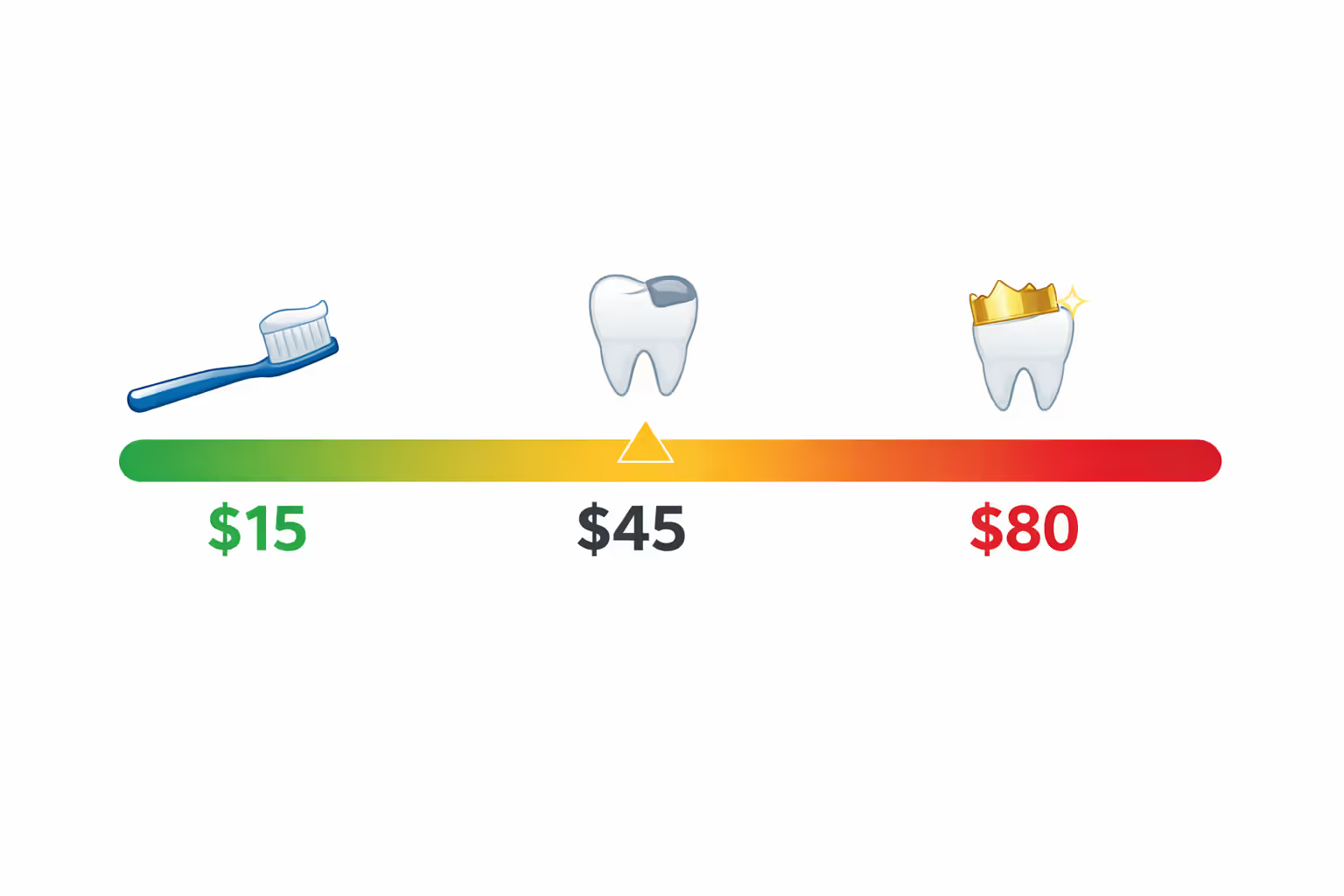

Expect to pay anywhere from $15 to $80 each month for dental insurance designed for seniors. The variation is significant, and it's tied directly to what you're getting. A bare-bones plan at $20-$35 monthly will handle your twice-yearly cleanings and annual X-rays without charging you anything extra, but don't count on help when you need a filling or extraction. Step up to the $40-$60 range, and you'll get partial reimbursement for fillings, basic extractions, and root canals. The premium plans—those $70-$80 monthly policies—reimburse the most for crowns, bridges, and dentures, though you'll still hit a ceiling on annual benefits.

Over a full year, you're looking at $180 to $960 just in premiums. Let's say you pick a middle-of-the-road plan at $45 monthly. That's $540 in premiums by December. Now add your deductible, which runs $50-$100 in most plans. Factor in copayments—you're usually paying 20-50% of the bill for basic and major dental work. And here's the real kicker: most plans cap annual benefits at $1,000-$1,500, so if you need extensive work, you'll blow through that limit and pay everything beyond it yourself.

Medicare Advantage plans bundle dental coverage differently. These plans charge their own premiums—sometimes nothing beyond your standard Part B premium, sometimes as much as $150 monthly. The dental portion varies dramatically between plans. One might only cover preventive visits. Another provides a $500 allowance. A generous plan might give you $3,000 to spend on dental care annually. But you're locked into their medical provider network, which doesn't work for everyone's situation.

Author: Tyler Grant;

Source: ladylesliebelize.com

Standalone dental policies give you flexibility. You're not tied to a specific network for your medical care, and you can match any dental plan with Original Medicare or a Medigap policy. The downside? Most make you wait 6-12 months before they'll cover major procedures like crowns or bridges. If your dentist just told you that old crown needs replacement, buying insurance today won't help until next year.

What Affects the Cost of Senior Dental Insurance

Where you live changes everything. A 68-year-old in rural Mississippi might pay $22 for the same coverage that costs $47 in Manhattan. Cities with expensive dentists and high demand push premiums higher. Smaller markets sometimes offer cheaper premiums, but you'll find fewer dentists who participate in the network.

Your age matters less than you'd think. Yes, some companies charge a bit more once you hit your 70s—maybe $3-$8 extra each month—but it's not a dramatic jump. Your dental history barely factors in. Unlike medical insurance underwriting, dental insurers generally accept anyone regardless of cavities, missing teeth, or gum disease. They protect themselves with waiting periods instead of higher premiums.

Coverage tier creates the biggest price swings. Three basic categories exist: preventive-only plans (cleanings, checkups, X-rays), basic plans (adding fillings, simple extractions, periodontal maintenance), and comprehensive plans (covering crowns, bridges, dentures, root canals). Each jump up roughly doubles what you'll pay. A preventive-only plan might cost $18 monthly. Basic coverage jumps to $38. Comprehensive hits $68.

Author: Tyler Grant;

Source: ladylesliebelize.com

Those annual maximum benefits function as a hidden cost multiplier. Most individual policies cap what they'll pay at $1,000-$1,500 per year. Need a crown at $1,200 and two fillings at $400 in the same year? You've hit $1,600 in dental work. With a $1,500 annual max, you're covering that last $100 entirely on your own, despite paying premiums faithfully. A few higher-premium plans push maximums to $2,000-$2,500, but they're uncommon.

Deductibles span from $0 to $100 yearly. Plans with zero deductibles cost $8-$12 more monthly than identical plans with a $50 deductible. If you're only getting preventive care—typically covered at 100% with no deductible required—you're wasting money paying extra for a zero-deductible feature.

Waiting periods don't change your premium, but they devastate the value proposition. Most standalone policies enforce 3-6 month waits for basic procedures and a full 12 months for major work. Enroll in January when you need a crown? You won't get coverage until the following January—while paying premiums the entire time. Medicare Advantage dental bypasses waiting periods entirely, which makes them attractive if you need work done immediately.

Types of Dental Coverage Options for Seniors

Standalone Dental Insurance Plans

These policies operate completely independently from Medicare. You're buying them from companies like Delta Dental, Cigna, Humana, or Guardian, paying a separate monthly premium exclusively for dental coverage. Standalone plans typically give you the most dentist options, particularly PPO-style plans that let you visit out-of-network providers for reduced reimbursement.

The standard coverage formula follows a 100-80-50 pattern: preventive services get covered completely, basic procedures at 80%, and major work at 50%. That $900 crown? You're paying $450 after insurance covers half (assuming you've cleared your deductible and haven't maxed out your annual benefit). These work well if you want Original Medicare handling your medical needs but want dedicated dental benefits.

Waiting periods remain the major obstacle. Insurance companies protect themselves from people who only buy coverage when they need expensive dental work by making new enrollees wait. A few plans waive waits if you're switching directly from another dental policy without any gap, but if you're buying dental insurance for the first time at 65, expect the full waiting schedule.

Medicare Advantage Plans with Dental Benefits

About 95% of Medicare Advantage plans now include dental coverage—up from 78% just five years ago. What you're getting ranges from minimal (one preventive visit per year) to generous (comprehensive services with $2,000+ allowances). The Medicare Advantage premium you pay incorporates this dental benefit—you're not paying a separate dental premium.

Budget-conscious seniors gravitate toward these all-in-one plans. A $25 monthly Medicare Advantage premium might bundle dental, vision, and hearing benefits with your medical coverage. Waiting periods don't exist; whatever's covered starts immediately when your plan takes effect. Networks run narrower than standalone dental insurance, but most metro areas have adequate provider options.

The major constraint: you're committed to the plan's entire structure. Your dentist might be in-network, but what if your cardiologist isn't covered under the medical side? That creates tough decisions. You can switch Medicare Advantage plans each fall during open enrollment, but constantly changing disrupts your care relationships.

Discount Dental Plans

These aren't insurance. You're paying $100-$200 annually for membership that gives you access to discounted fees at participating dentists. Maybe you'll pay $85 for a cleaning that normally runs $135, or $650 for a crown instead of $1,200. No annual maximum exists. No waiting periods. No paperwork. Just discounted pricing.

Discount plans work best for seniors with predictable, modest dental needs or people who've already maxed out their insurance annual limits. They're also useful right after enrolling in standalone insurance during those waiting periods. The problem: savings fluctuate wildly. Some dentists offer real 20-40% discounts. Others barely reduce fees by 5-10%, meaning the membership cost almost equals your savings.

Medicaid Dental Coverage (State-Dependent)

Seniors with limited income who qualify for both Medicare and Medicaid simultaneously—called dual eligibles—might get dental benefits from their state's Medicaid program. What's covered depends entirely on which state you live in. Fourteen states limit coverage to emergency dental care only. Other states provide comprehensive services including dentures, crowns, and gum disease treatment.

California, New York, and Illinois offer relatively strong Medicaid dental benefits for seniors. Texas, Tennessee, and Florida provide minimal help. If your income hovers near Medicaid eligibility limits, research your state's specific program—coverage can be surprisingly thorough in certain states.

How to Find Low Cost Dental Insurance as a Senior

Author: Tyler Grant;

Source: ladylesliebelize.com

Begin shopping 2-3 months before your 65th birthday. Several insurers discount rates when you enroll before actually needing coverage, and you'll avoid frantically comparing plans while juggling all your other Medicare enrollment decisions. Connect with your state's SHIP (State Health Insurance Assistance Program) counselors, who provide free, unbiased advice on dental coverage alongside Medicare enrollment assistance.

Compare at least five plans from different companies. Premium differences for comparable coverage can hit $20 monthly—that's $240 yearly. A plan charging $52 might offer identical benefits to one costing $32 once you look past brand recognition. Check whether your current dentist accepts each plan's network; switching dentists just to save $15 monthly rarely makes sense when you've built a trusted relationship.

Professional and alumni associations frequently negotiate group dental rates for members. AARP partners with Delta Dental for discounted plans. Teacher retirement associations, union retiree groups, and college alumni organizations often provide dental insurance at 10-25% below individual market rates. Even if the membership fee costs $25-$50 annually, premium savings typically exceed that.

Some state pharmaceutical assistance programs include dental benefits. Pennsylvania's PACE program, for instance, combines prescription help with dental coverage for low-income seniors. These programs operate quietly but deliver substantial value.

Time your enrollment strategically. Standalone dental insurance accepts applications year-round, but starting in January maximizes your annual maximum for that calendar year. Enroll in October, and you only get three months of benefits before the annual maximum resets—you're potentially wasting coverage.

Free dental insurance for seniors essentially doesn't exist outside Medicaid. Charitable organizations sometimes provide limited free care, but genuine zero-cost insurance isn't available. Be skeptical when advertisements promise "free" dental coverage; they're usually promoting Medicare Advantage plans that bundle dental benefits within the premium structure, but the plan itself isn't free—you're still paying that Medicare Advantage premium.

Dental Care Alternatives for Seniors Without Insurance

Author: Tyler Grant;

Source: ladylesliebelize.com

Dental schools deliver care at 30-60% below standard market rates. Students perform procedures under close faculty supervision, producing quality work at reduced prices. That $1,200 crown at a private practice might cost $500-$700 at a dental school. The tradeoff: appointments stretch longer (frequently 2-3 hours instead of one), and scheduling flexibility depends on academic calendars.

Most dental schools prioritize complex cases because they offer better learning opportunities, making them particularly well-suited for seniors needing extensive work like multiple extractions or complete dentures. Simple cleanings may involve longer waits since they're less educationally valuable for students.

Federally Qualified Health Centers (FQHCs) charge based on sliding fee scales tied to income. A senior earning $20,000 annually might pay $35 for a cleaning that costs others $135. More than 1,400 FQHCs across the country provide dental services, though wait times sometimes stretch several weeks for non-emergency care. Find locations through FindAHealthCenter.hrsa.gov.

Private dentists often arrange in-house payment plans for major work. Instead of $3,000 upfront for an implant, you might negotiate $300 monthly for ten months, frequently interest-free. These arrangements work best with dentists you've visited previously who trust your payment reliability.

Dental tourism to Mexico, Costa Rica, or Colombia can slash costs by 50-70%, but carries real risks. A $15,000 full-mouth reconstruction might cost $6,000 abroad, including travel expenses. However, follow-up complications get expensive when you need adjustments after returning home. This option suits seniors with extensive needs, good overall health for travel, and realistic expectations about quality variations.

Mission of Mercy events and charitable dental clinics offer free care on specific dates. These one-day or weekend events serve hundreds of patients on a first-come basis, frequently requiring overnight waits in line. Services emphasize extractions, fillings, and cleanings rather than cosmetic procedures. Check DentalLifeline.org for upcoming events in your region.

Does Dental Insurance Cover Implants and Major Procedures

Many seniors overpay for dental coverage they'll never come close to using fully, while others skip insurance completely and face financial disaster when major work becomes unavoidable.Matching your plan to your actual dental condition is everything. If you haven't had a cavity in 20 years, a basic preventive plan makes sense. But if you're dealing with several old crowns and a history of gum disease, comprehensive coverage—despite higher premiums—typically pays for itself within two years

— Robert Chen

Most dental insurance plans label implants as cosmetic or elective, excluding them completely. Plans that do cover implants typically reimburse at major procedure rates—50% of costs after you've met deductibles, limited by annual maximums. A $3,500 implant might generate $1,750 in insurance benefits if your plan covers implants and you haven't used other benefits that year.

The math rarely supports buying insurance solely for implant coverage. Pay $65 monthly ($780 yearly) for a plan with a $1,500 annual maximum covering implants at 50%—you'll receive roughly $1,750 in benefits for one implant. But you paid $780 in premiums, netting only $970 in actual benefit. Next year you'll pay another $780 for routine coverage, and implants are typically one-time procedures. You'd come out ahead paying cash and negotiating a direct discount.

Waiting periods for implants stretch to 12-24 months on policies that cover them at all. Insurers recognize implants cost $3,000-$5,000 and want to collect two years of premiums before paying benefits. For seniors needing an implant now, insurance provides zero help.

Crowns, bridges, and dentures get better treatment—typically 50% reimbursement after 6-12 month waiting periods. A $1,200 crown costs you $600 after insurance, plus your deductible. Multiple crowns create problems with annual maximums though. Three crowns totaling $3,600 would generate $1,800 in insurance benefits, but if your plan caps at $1,500 annually, you'll only receive that amount and cover the remaining $2,100 yourself.

Root canals fall under either major or basic procedures depending on which insurer you're dealing with. Most cover them at 70-80%, making insurance genuinely valuable for these $800-$1,500 procedures. A $1,000 root canal costs you $200-$300 after insurance—less than you paid in annual premiums, but combined with cleanings and other care, the value equation improves.

Periodontal treatment for gum disease gets inconsistent coverage. Some plans cover deep cleanings and scaling at 80% under basic procedures; others classify them as major work at 50%. Maintenance cleanings following active periodontal treatment may be limited to two per year instead of the standard four cleanings, forcing you to pay full price for additional visits.

Medicare Advantage plans with dental allowances handle major procedures through a different mechanism. Instead of percentage-based coverage, you get a dollar allowance—perhaps $1,500 annually for any dental work. You could apply the full $1,500 toward an implant, multiple fillings, or any combination. Waiting periods don't apply, and you control how to allocate the allowance. The limitation: once you've exhausted your $1,500, you're self-paying until next year.

| Plan Type | Average Monthly Cost | Coverage Level | Best For | Pros | Cons |

| Standalone Preventive | $20-$35 | Cleanings, exams, X-rays fully covered | Seniors with healthy teeth needing only routine maintenance | Affordable premiums, extensive dentist networks, combines with any Medicare option | Zero help with major procedures, waiting periods required |

| Standalone Comprehensive | $60-$80 | Preventive fully covered, basic 80%, major 50% | Seniors expecting crowns, bridges, or substantial dental work | Best reimbursement percentages, $1,500-$2,500 annual maximums | High premiums, 12-month waits for major procedures, annual maximums still restrict coverage |

| Medicare Advantage with Dental | $0-$150 (entire plan premium) | Highly variable; $500-$3,000 yearly allowance | Seniors comfortable with managed care who want bundled benefits | Zero waiting periods, immediate coverage starts, bundles medical/prescription/dental | Required to use plan's medical network, dental networks may be restrictive, allowances differ significantly |

| Discount Dental Plan | $100-$200 yearly | 10-40% fee reductions on all procedures | Seniors with immediate needs during insurance waiting periods or after exhausting annual maximums | Zero waiting periods, no annual limits, inexpensive | Not actual insurance—you pay discounted fees directly, savings inconsistent by provider |

| Medicaid (varies by state) | $0 | Emergency-only through comprehensive, state-dependent | Low-income seniors qualifying for dual Medicare/Medicaid status | Free or minimal cost, comprehensive in certain states | Only available meeting income thresholds, major coverage gaps in numerous states |

Frequently Asked Questions About Senior Dental Insurance

Navigating dental insurance as a senior demands honest assessment of your dental health trajectory and financial priorities. A 65-year-old with excellent dental health might reasonably skip insurance for 5-10 years, banking the premium savings for eventual major work. Someone dealing with a mouthful of aging fillings and crowns should secure comprehensive coverage before problems escalate.

Calculate your personal break-even point by listing anticipated dental needs for the next 12-24 months. Total up the uninsured cost, then compare it to annual premiums plus your out-of-pocket costs with insurance (deductibles, copayments, and anything exceeding annual maximums). If insurance saves you $200+ annually and you expect similar needs continuing, coverage makes financial sense.

Don't ignore the peace-of-mind factor, but don't overpay for it either. Some seniors sleep better knowing unexpected dental costs won't derail their budget, even if insurance technically costs more than paying out-of-pocket. That's a legitimate choice—just make it consciously rather than assuming insurance always saves money.

Review your coverage annually during Medicare's fall open enrollment period. Dental needs shift, new plans enter the market, and better options may surface. A plan that fit perfectly at 66 might be overpriced by 72 if your dental health has stabilized or your dentist has left the network.

The dental insurance market for seniors has improved dramatically, with more choices and stronger benefits than existed even five years ago. Whether you choose standalone coverage, Medicare Advantage dental, discount plans, or self-insure while using safety-net options, understanding the true costs and realistic benefits puts you in control of both your dental health and your retirement budget.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.