Two different dental insurance cards lying on a wooden desk next to a tooth model, dental mirror, and calculator, top-down view

Is It Illegal to Have Two Dental Insurance Plans?

Let me clear this up right away: carrying multiple dental insurance policies violates zero laws. The question itself reveals a common misunderstanding about how insurance actually works in the United States.

Right now, somewhere between 8-12 million Americans maintain dual dental coverage. Your employer might provide a basic plan while your spouse's company offers premium benefits—so you're on both. Some people buy marketplace policies to supplement workplace plans that barely cover anything. Others inherit coverage from divorced parents or layer Medicare Advantage dental benefits with standalone policies.

State insurance departments don't just allow this—they've spent decades developing coordination of benefits frameworks specifically because dual coverage happens constantly. Insurance commissioners created these standardized rules so carriers know exactly how to handle situations where someone files claims against multiple policies.

The real questions worth asking: Will two policies actually reduce what you pay out of pocket? How do insurance companies decide which one pays first? When does maintaining dual coverage waste money instead of saving it?

Can You Legally Have Multiple Dental Insurance Policies

Federal law stays completely silent on limiting how many dental policies one person can carry. State insurance regulations don't restrict it either. You could theoretically maintain five separate policies if you somehow qualified for that many and wanted to burn money on premiums.

Most people land in dual coverage scenarios without actively planning for it:

Marriage creates the most common situation: Let's say you work for a hospital system with decent dental benefits. Your partner works for a tech company that also provides dental insurance. You each enroll in your own employer's plan for individual coverage. During open enrollment, your partner adds you as a dependent spouse. You just became dual-covered without thinking about it.

This exact scenario affects roughly 7 million married couples across the country, based on benefits enrollment data from large employers.

Workplace plans that barely function: Your small company offers dental insurance with a laughable $800 annual maximum. You know you need three crowns this year at $1,300 each. Some people respond by purchasing individual policies through the ACA marketplace or directly from carriers like Delta Dental or Cigna. The workplace plan pays first, the individual policy picks up additional costs after the first plan maxes out.

Children splitting time between divorced parents: Family court judges routinely order both parents to maintain dental coverage for their kids. The child ends up covered under Mom's employer plan and Dad's employer plan simultaneously until they turn 26. Nobody's breaking laws—the judge specifically mandated this arrangement.

Retirees supplementing Medicare gaps: Traditional Medicare doesn't touch dental care except in rare medical emergencies. Medicare Advantage plans sometimes include dental, but the coverage often caps at $500-$1,000 annually with limited networks. Retirees frequently buy standalone dental policies to access better benefits and broader provider choices.

Could you really juggle three active policies? Sure. I've seen it happen when someone had employer coverage, got added to their spouse's better plan, but forgot to drop their individual marketplace policy from before they got married. The third carrier processes claims dead last, after the first two have already paid. By then, you've usually hit 100% of covered costs anyway—meaning you're literally throwing premium dollars into a shredder.

Here's where legality actually matters: disclosure requirements. Every single insurance company on your roster needs to know about every other insurance company. Your dentist's billing office needs the complete list. Attempting to collect $1,200 from Carrier A and another $1,200 from Carrier B on the same $1,200 root canal constitutes fraud.

Not "aggressive claims filing" or "maximizing benefits"—actual prosecutable fraud. Carriers share information through clearinghouses and the National Association of Insurance Commissioners. Getting caught means policy cancellations, getting blacklisted from coverage, demands to repay every fraudulent claim, and potential criminal charges depending on the dollar amounts involved.

How Coordination of Benefits Works with Two Dental Plans

Insurance companies use coordination of benefits—everyone in the industry just says "COB"—to establish a payment pecking order when someone carries multiple policies. The entire system exists to prevent you from profiting off dental claims by collecting $2,000 in insurance payments for a $1,000 procedure.

One carrier gets designated primary, the others fall into secondary positions (or tertiary if you've somehow accumulated three plans). These assignments follow rigid rules, not arbitrary decisions by insurance adjusters having a bad day.

Which Plan Pays First

Author: Ashley Whitford;

Source: ladylesliebelize.com

The hierarchy works like this:

Birthday rule for dependent children: Take both parents' birthdates—just the month and day, completely ignore which year they were born. Whichever parent celebrates their birthday earlier in the calendar year holds the primary coverage for the kids.

Example: Mom was born September 22nd. Dad's birthday falls on March 9th. Dad's dental plan pays all claims first because March comes before September. Doesn't matter that Mom's Fortune 500 employer offers way better benefits than Dad's small business plan.

Custody agreements from divorce proceedings can override this birthday rule if the judge specifically designated which parent's insurance is primary. That court order trumps standard coordination rules.

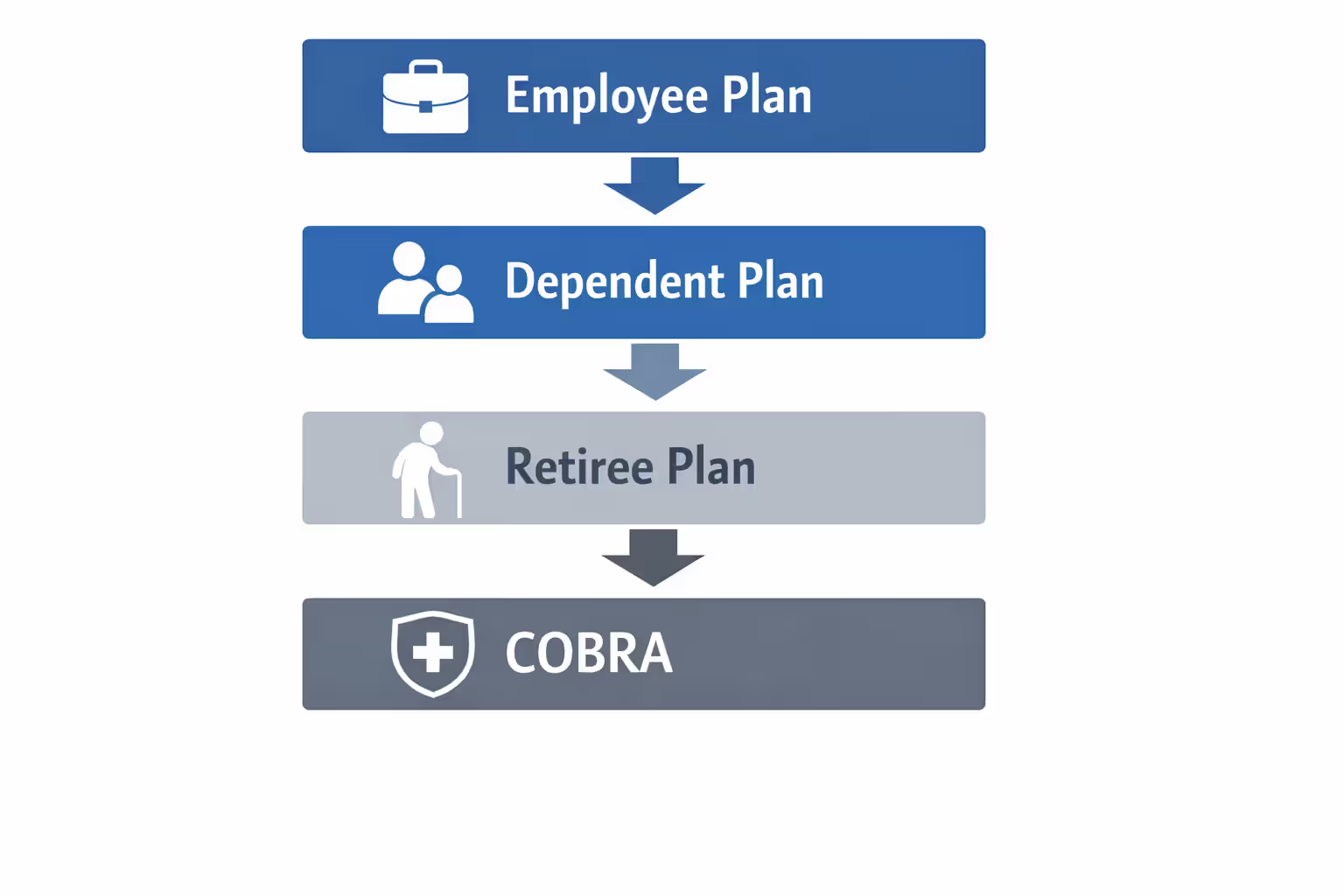

Your own employment beats dependent status every single time: Even if being added to your spouse's employer plan would give you access to amazing benefits while your own workplace plan is mediocre, your direct employment coverage still pays first. Insurance regulations prioritize the plan where you're the actual employee over plans where you're listed as someone's dependent spouse.

Active employment trumps retirement benefits: Still working part-time at 68 while collecting retirement benefits from your previous employer? Your current job's coverage takes primary position. Retiree plans almost always slide into secondary status when active group coverage exists.

COBRA creates weird situations: If you're continuing your old employer's coverage through COBRA after leaving that job, then you start a new job with benefits, the new employer's plan immediately becomes primary. COBRA nearly always processes as secondary insurance when any active group coverage exists.

Here's what actually happens when you file a claim: Your primary insurer evaluates everything exactly as if you were uninsured elsewhere. They apply their fee schedules, their coverage percentages, their plan rules. The existence of your backup insurance doesn't reduce what they pay by one penny—they literally cannot factor your other coverage into their payment calculation.

What the Secondary Plan Covers

After your primary plan pays and generates an Explanation of Benefits statement, you send that EOB to your secondary carrier along with documentation of what you still owe. Now the backup insurer evaluates the remaining balance.

Their payment equals whichever amount is smallest among these three figures: - The difference between what the primary paid and what the dentist actually charged - The amount they would have sent you if they'd been processing this claim as primary insurance - Whatever amount brings your total insurance reimbursement to 100% of the allowed charge for that procedure

Let me walk through a real scenario: Your dentist bills $1,400 for a root canal. Your primary plan considers $1,100 "reasonable and customary" for that procedure and covers 60% of major services, sending you a check for $660. You're staring at a $740 bill.

Your secondary insurance also pays 60% for major work but sets their allowed charge at $1,200 for root canals. If they'd been primary, they would have paid $720 (60% of their $1,200 allowed amount). The unpaid portion of your dentist's bill currently sits at $740. Your secondary insurer cuts you a check for $720—the lower figure between what they'd pay as primary versus what you still owe. You end up paying $40 from your own pocket.

Notice you didn't achieve 120% coverage despite carrying two separate 60% policies. Coordination prevents that outcome. You'll rarely see 100% reimbursement, particularly when dentists charge above what both insurers consider reasonable for that zip code.

When Having Two Dental Insurance Plans Makes Sense

Dual coverage saves specific people real money in specific circumstances. For everyone else, it's like paying $50 monthly for a premium streaming service you never watch.

Situations where doubling up delivers value:

Facing major dental expenses in the next twelve months: Your orthodontist quoted $6,500 for your daughter's braces. Your son needs two crowns and a bridge totaling $4,200. You're getting dental implants for $3,800. Most dental plans tap out between $1,000-$2,000 per person annually.

With just one plan, you might see $1,500 in coverage against $14,500 in total family dental costs—you're paying $13,000 out of pocket. Two plans give you access to two separate annual maximums. If each plan covers $1,500, you're getting $3,000 in insurance payments instead of $1,500. Your out-of-pocket just dropped from $13,000 to $11,500. That $1,500 in additional coverage easily justifies dual plan premiums.

Secondary coverage costs almost nothing: Your spouse's employer charges $18 monthly to add you as a dependent—that's $216 yearly. Even if that backup plan only saves you $350 in out-of-pocket costs over the year, you're $134 ahead. When the premium-to-benefit math clearly favors dual coverage, take it.

Eliminating cost-sharing on preventive care: Some people deal with periodontal disease requiring more frequent cleanings than the standard twice-yearly schedule. Others need additional X-rays due to complicated dental situations. Two plans working together can eliminate any patient responsibility for these preventive services, even if each individual plan would normally charge you something.

Situations where it's burning money:

You only need basic preventive care: Your dental routine consists of two cleanings yearly, occasional X-rays, maybe a filling every few years. Your teeth are fundamentally healthy. Why pay $700 annually in additional premiums for a secondary plan when your primary coverage already pays 100% of cleanings and basic preventive care? You're literally subsidizing other people's dental work.

The secondary plan costs more than it could possibly save: Some employers charge $95 monthly for dependent coverage—that's $1,140 per year. Unless you consistently max out annual limits or face major procedures, you won't recoup those premiums through reduced out-of-pocket costs. You'd need roughly $1,900 in dental work just to break even on that premium.

Two nearly identical plans with duplicate coverage levels: Carrying two policies with the same 80/50 coverage structure and identical $1,500 annual maximums provides minimal value. Your secondary plan becomes relevant only after you've exhausted the primary plan's yearly maximum—which happens rarely unless you need major work.

Calculate this for your own situation: What did your household spend on dental care last year? Add up your total bills. What portion did insurance cover versus what you paid directly? Now estimate what you would have paid out-of-pocket with secondary coverage. Compare that potential savings against the annual premium for adding the second plan. Sometimes the numbers reveal uncomfortable truths about wasted money.

Author: Ashley Whitford;

Source: ladylesliebelize.com

How to Find Out If You Have Dental Insurance

Some people legitimately don't know whether they currently carry dental coverage. Maybe benefits got bundled together when you started your job five years ago. Maybe a family member added you to their plan. Here's how to find out:

Scrutinize your paystub for deductions beyond medical insurance: Dental premiums often appear as tiny separate line items—sometimes just $7 or $15 per paycheck. Some employers bundle medical and dental into one combined deduction labeled "health insurance," which means you'll need to dig deeper into benefits documents.

Search through that enrollment paperwork from your first week at work: Remember those packets you signed during new hire orientation or last October's open enrollment? Those summaries list every benefit you elected. You might discover a dental benefits booklet still sitting unopened in your desk drawer.

Make one phone call to your HR department: Five minutes on the phone with your benefits administrator answers the question definitively. They'll confirm whether you elected dental coverage, identify your carrier by name, and provide your policy number. This beats three hours of searching through filing cabinets.

Empty your wallet and check every card: Insurance cards hide behind credit cards, membership cards, or get mistaken for old gift cards. Some carriers issue combination medical-dental cards with both benefits listed on one card. Others mail dental cards separately, sometimes in different envelopes arriving weeks apart.

Access your company's benefits platform online: If your employer uses Workday, ADP, BambooHR, or similar systems, log in and view all active benefits. You can usually download digital insurance cards immediately, even if you lost the physical copies months ago.

Contact your dentist's billing department directly: Had an appointment within the past year? The office already has your insurance information filed in their patient management system. Their billing staff can tell you exactly which carrier they've been submitting claims to and whether those claims have been paying.

Have a conversation with family members: Under 26? Your parents might have added you to their employer plan without mentioning it. Recently married? Your spouse might have enrolled you during their open enrollment period last fall. A quick text message can reveal coverage you didn't know existed.

Scan bank statements for automatic payments: Bought an individual policy through healthcare.gov or directly from an insurer? You'll see monthly automatic withdrawals to Cigna, Delta Dental, Guardian, Humana, or whichever company you purchased from. Search your statements for these company names going back 3-4 months.

Retirees should dig out pension paperwork—many employers continue dental benefits into retirement as part of the overall pension package. Medicare beneficiaries should verify whether their Medicare Advantage plan includes dental. Roughly 84% of them do according to 2024 data, though coverage varies dramatically from basic preventive-only to comprehensive benefits.

How to Determine What Dental Insurance Plan You Have

Confirming you have insurance differs completely from understanding what that insurance actually covers. Here's how to nail down your plan's specifics:

Locate your physical or digital insurance card: That piece of plastic or PDF contains critical information. The carrier's name appears prominently—Delta Dental, Aetna, Cigna, MetLife, United Healthcare, Guardian, Humana, or dozens of regional carriers. The group number identifies your employer's specific plan design with that carrier. The member ID is your unique personal identifier. Customer service phone numbers connect you to representatives who can explain your specific benefits.

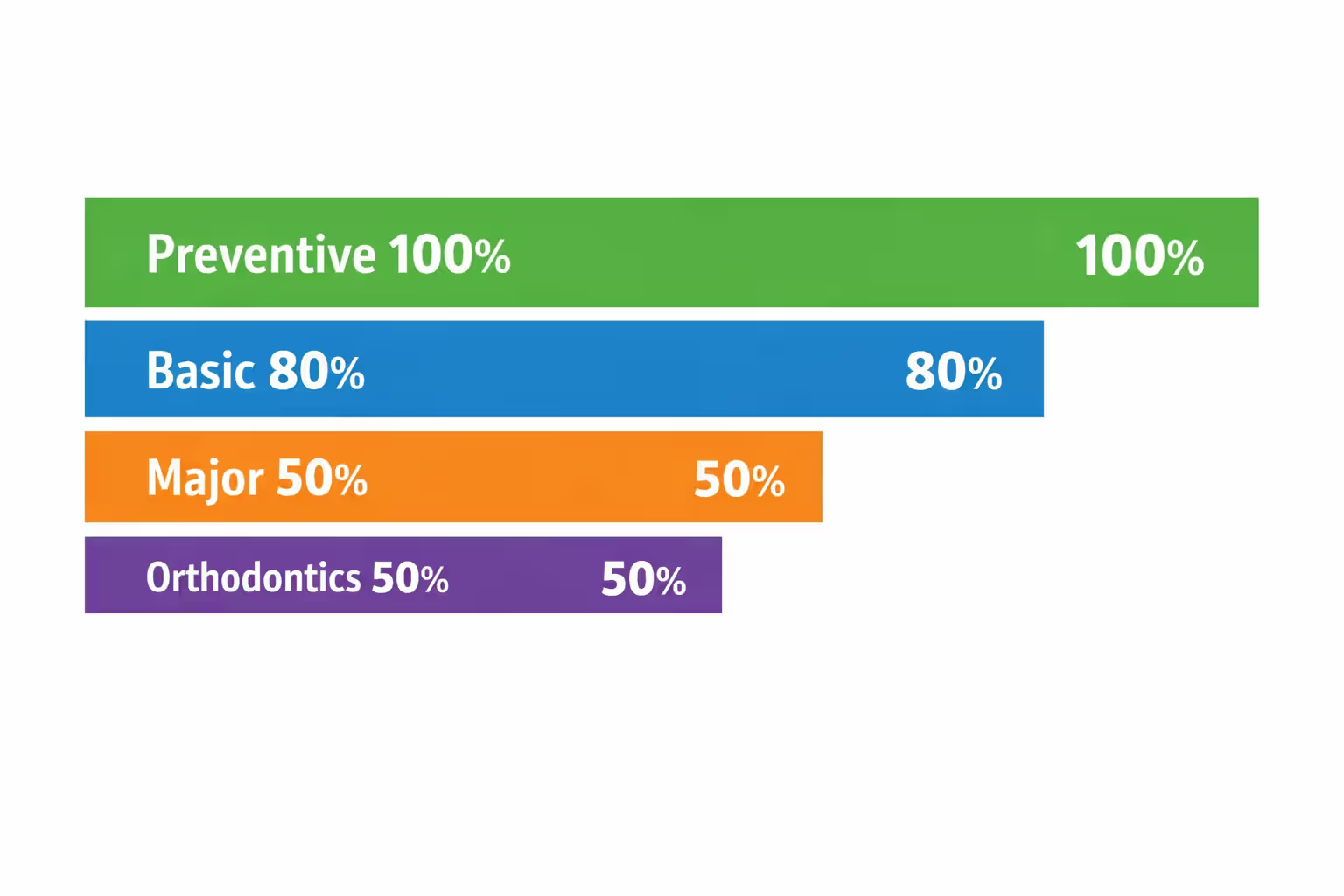

Read your Evidence of Coverage or Summary Plan Description: Federal ERISA regulations require employers to provide these documents. They break down coverage into distinct categories—preventive care, basic procedures, major services, orthodontics. You'll see the coverage structure spelled out: preventive might be covered at 100%, basic procedures at 80%, major work at 50%. The document lists your annual maximum (commonly $1,500 or $2,000 per person), your deductible (typically $50 per individual or $150 per family), and any waiting periods before major work gets covered.

Log into your insurance carrier's member portal: Every major carrier maintains dedicated websites. Create an account using your policy number and date of birth. Once you're in, you'll find: - Remaining balance on your annual maximum - Whether you've satisfied your deductible for this year - Detailed breakdowns showing exactly what procedures are covered at which percentages - Searchable directories of in-network dentists by specialty and location - Complete claims history showing every service you've received - Downloadable insurance cards and benefits summaries

Use the customer service number on your card: Those representatives exist to clarify confusing policy language. Wondering whether your specific plan covers dental implants? Whether you need pre-authorization before getting a crown? How much your plan will actually pay toward your teenager's $5,800 orthodontic treatment? They'll translate insurance jargon into plain English.

Ask your dentist's office to run a benefits verification: Before scheduling major treatment, request that the billing department verify your benefits directly with your insurer. They'll contact your insurance company, confirm active coverage, and generate a detailed treatment estimate showing expected insurance payment versus your responsibility. This "pre-determination" or "pre-authorization" isn't a payment guarantee, but it's typically accurate within $50-100.

Figure out which plan type you have:

PPO plans (Preferred Provider Organizations) give you freedom to see any dentist you want but incentivize staying in-network through better reimbursement rates. You might get 80% coverage when using in-network providers but only 60% when seeing out-of-network dentists.

HMO plans (sometimes called DHMO—Dental Health Maintenance Organization) require choosing a primary care dentist from a restricted network. You'll need referrals for specialists. These plans charge lower premiums in exchange for less flexibility and smaller provider networks.

Indemnity plans provide complete freedom to choose any dentist but typically reimburse based on "usual, customary, and reasonable" charges in your geographic area—which might fall below your dentist's actual fees, leaving you to pay the difference.

Standard coverage tiers in most plans: - Preventive services (cleanings, routine exams, standard X-rays, fluoride treatments): Usually covered at 100% with no deductible applied - Basic restorative work (fillings, simple extractions, emergency palliative care, non-surgical periodontal work): Commonly covered at 70-80% after you've met your deductible - Major procedures (crowns, bridges, root canals, dentures, surgical extractions): Generally covered at 50% after deductible - Orthodontics (braces, Invisalign, retainers): Around 50% coverage with a separate lifetime maximum, typically $1,500-$2,000 per person

Author: Ashley Whitford;

Source: ladylesliebelize.com

Options When You Don't Have Dental Insurance

Lacking insurance shouldn't mean ignoring your oral health. Multiple pathways exist for accessing affordable dental care:

Dental savings plans operate completely differently than insurance: You pay an annual membership fee, usually $85-$200 for individuals or $150-$350 for entire families. In return, participating dentists agree to charge you predetermined discounted rates—often 20% off basic procedures, 30% off major work, sometimes 50% off cosmetic treatments like teeth whitening or veneers. No waiting periods exist. No annual maximums limit your savings. No claim forms to file. You simply pay the reduced rate directly to the dentist at your appointment. These plans work particularly well for people who need immediate major dental work and can't wait through traditional insurance waiting periods that often run 6-12 months for crowns or bridges.

Federally Qualified Health Centers charge based on your income: These community health centers receive federal grants requiring them to serve patients regardless of ability to pay. They use sliding fee scales based on your household income and family size. Someone earning $28,000 annually might pay $25 for a cleaning that normally costs $140. Services include everything from routine exams to extractions, fillings, root canals, and dentures. The Health Resources and Services Administration maintains a search tool at findahealthcenter.hrsa.gov—enter your ZIP code to locate nearby centers.

Dental schools need patients for students to practice on: Accredited dental programs require supervised clinical hours for their students. You'll save 30-70% compared to private practice fees. Appointments take significantly longer because dental students work methodically under constant faculty supervision. But you're receiving thorough care with multiple licensed dentists reviewing your treatment. These schools also operate specialty clinics—periodontics, prosthodontics, orthodontics, endodontics, oral surgery—all at substantially reduced rates. Some schools even offer emergency dental clinics.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Payment plans through dentist offices or third-party financing: Many practices offer in-house financing arrangements—pay $125 monthly over twelve months instead of $1,500 upfront for that crown. Third-party medical credit cards like CareCredit, LendingClub, or Lending point provide promotional financing periods. Some offer 6, 12, 18, or 24-month interest-free terms if you pay the full balance before the promotional period expires. Read the terms carefully—deferred interest can hit brutally hard if you miss the deadline by even one day, applying retroactive interest to the entire original balance.

Medicaid provides coverage for qualifying low-income individuals: Eligibility thresholds vary dramatically by state, but if you qualify, you gain access to dental care. Coverage for adults ranges from comprehensive benefits in some states to emergency-only extractions in others. Children enrolled in Medicaid receive extensive dental benefits through EPSDT (Early and Periodic Screening, Diagnostic and Treatment), covering everything necessary to maintain healthy teeth—fillings, cleanings, fluoride, sealants, extractions, space maintainers, even medically necessary orthodontics in most states.

Free dental clinics and charitable events operate year-round: Organizations like Mission of Mercy, Remote Area Medical, and Donated Dental Services host weekend or week-long clinics where volunteer dentists provide free care on a first-come, first-served basis. No income verification, no paperwork, no questions asked. Local health departments sometimes sponsor free dental days. Churches and community centers occasionally coordinate screening events that connect uninsured people with volunteer providers or reduced-cost programs.

Direct negotiation with dentists for cash discounts: Paying cash at the time of service? Many practices discount fees 10-30% when you eliminate billing costs, collection risks, and insurance company administrative headaches. Simply ask the office manager or dentist directly: "What cash discount can you offer if I pay in full today?" Many practices, particularly smaller independent offices, will negotiate—especially for larger treatment plans.

The biggest misconception I see repeatedly is patients assuming dual coverage equals double coverage—like two 50% plans automatically combine to give them 100% coverage on everything. The coordination of benefits calculation is far more nuanced than simple addition, and patients frequently still owe out-of-pocket costs, particularly when their dentist's fees exceed the allowed amounts both carriers recognize for that procedure. I tell every patient with multiple policies to request a detailed benefits verification before scheduling major treatment. Those estimates prevent shocking bills and help them understand what dual coverage will realistically provide versus what they're imagining it will provide based on assumptions

— Jennifer Martinez

Frequently Asked Questions About Multiple Dental Insurance Plans

Understanding dental insurance—whether you're managing dual policies, discovering forgotten coverage, or finding care without insurance—puts you in control of oral health expenses instead of letting surprise bills control you.

Dual dental coverage operates within completely legal frameworks and makes solid financial sense for certain people at certain times. Coordination of benefits processes prevent overpayment while helping you access maximum available resources. But "available" doesn't automatically mean "valuable." Carefully evaluate whether additional premiums deliver actual value based on your family's real dental needs over the coming year, not theoretical worst-case scenarios that may never materialize.

Uncertain about your current coverage situation? Invest an hour investigating. Check paystubs for deductions. Call your HR department. Log into benefits portals. Those 60 minutes prevent both missed opportunities to use existing benefits and devastating bills from assuming coverage where none actually exists.

Uninsured doesn't mean helpless. Dental savings plans, federally qualified health centers, dental school clinics, and flexible payment options keep preventive care and even major treatment financially accessible. Regular cleanings and checkups now prevent emergency room visits for dental abscesses later—ER visits that can cost $2,000-5,000 while solving nothing. Find an affordable option rather than avoiding the dentist entirely until you're in crisis.

The biggest mistake isn't having too much or too little insurance—it's failing to understand and fully leverage whatever coverage you actually possess. Review your benefits carefully every year, particularly before open enrollment deadlines when you can make changes. Coordinate properly when multiple plans are involved. Ask questions whenever confusion arises. Your teeth need to last 70-80 years, and understanding your insurance options makes that lifetime of dental care financially manageable rather than financially devastating.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.