Dental insurance card on a table next to a calculator, dental mirror, and toothbrush with a blurred dental office in the background

How to Verify Dental Insurance Coverage Before Treatment?

You schedule what seems like a straightforward dental appointment—maybe a filling or cleaning. Then weeks later, a bill arrives that's triple what you expected. Sound familiar? This scenario plays out in dental offices nationwide because patients skip a crucial step: confirming what their insurance actually covers before treatment begins.

Most people think having dental insurance means they're protected from major expenses. But insurance cards don't tell the whole story. Your actual benefits depend on dozens of factors that change throughout the year—how much you've already spent, which procedures your specific plan excludes, whether your dentist participates in your network, and timing restrictions you've never heard of.

Getting ahead of these complications isn't complicated, though it does require some homework. You'll need to collect specific details about your policy, track down the right people to ask, and know which questions actually matter. Skip these steps, and you're essentially gambling with your wallet.

Why Verifying Your Dental Insurance Matters

Here's what nobody tells you when you receive that insurance card: the benefits listed in your packet represent maximums, not guarantees. The actual payment your insurer makes depends on factors most people discover only after receiving an unexpected bill.

Think about Sarah, who needed a crown. Her benefits booklet said major procedures were covered at 50%. She calculated her cost based on the $1,200 the dentist quoted. But her insurance paid only $400 because they based their 50% on their "usual and customary" rate of $800—not the dentist's actual $1,200 charge. Sarah owed $800 instead of the $600 she'd budgeted. This happens constantly with out-of-network providers.

Claims get rejected for reasons that seem random until you understand insurance logic. Maybe you had a filling on that same tooth 18 months ago, and your plan won't cover another one for two years. Perhaps your policy excludes composite fillings on back teeth, covering only amalgam. Or you switched jobs in July, and your new policy has a six-month waiting period for anything beyond basic cleanings.

The financial impact compounds quickly. A routine year might include two cleanings ($200 each), a filling ($250), and some X-rays ($150)—total around $800. Without verification, you might discover your deductible is $100, you've already used $600 of your $1,000 annual maximum, and suddenly that "covered" filling costs you $200 out-of-pocket instead of the $50 you anticipated.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Treatment delays cause additional problems. When claims get denied or patients can't cover unexpected costs, necessary dental work gets postponed. That minor cavity you could've filled for $250? Give it six months without treatment, and now you need a $1,500 root canal and crown. Understanding what "verify dental insurance" actually means—confirming real numbers before committing to treatment—prevents these cascading problems.

What Information You Need to Verify Coverage

Insurance companies won't give you accurate information if you call unprepared. They need specific details, and missing even one piece means getting vague answers that prove useless when the bill arrives.

Grab your insurance card and look for the policy number—not your member ID, though many cards list both. These numbers serve different purposes. The policy number connects you to your specific benefit structure, which might differ substantially from other policies the same insurance company sells. Your member ID just identifies you personally within that policy.

The group number tells which employer or organization provides your coverage. This matters more than most people realize. Two employees at different companies might both have "Cigna dental insurance," but Group 12345 might cover implants while Group 67890 excludes them entirely. Different groups operate under completely different benefit structures, even with the same insurance carrier.

You'll need the subscriber's personal information—the actual policyholder's name, birth date, and sometimes Social Security number. If you have coverage through your spouse's employer, they're the subscriber. Insurance companies match eligibility records using the subscriber's details, not yours, even though you're the patient receiving treatment.

Your dentist's National Provider Identifier matters because contracted rates vary by provider. This ten-digit number determines whether your dentist qualifies as in-network. Dr. Smith might be in-network with your plan, while Dr. Johnson down the street isn't—resulting in drastically different out-of-pocket costs for identical procedures. Call your dental office to get their NPI before contacting insurance.

Procedure codes eliminate guesswork. Don't ask whether your insurance covers "a filling." That question yields useless answers. Instead, ask about specific CDT codes: "What percentage do you cover for D2392?"—that's a two-surface composite on a back tooth. Different codes carry different coverage levels, and amalgam versus composite fillings often get reimbursed at different rates.

The service date influences everything. Your benefits status on March 15th looks nothing like your status on November 15th if you've already had significant dental work. After $900 in claims, you're approaching your annual maximum. Before any treatment, your deductible still applies. Always verify based on when treatment will actually occur, not just whenever you happen to call.

Step-by-Step Process to Verify Dental Insurance

You've got three paths to get your benefits confirmed. Each works differently depending on whether you want detailed explanations, quick digital access, or prefer someone else handle the legwork entirely.

Contacting Your Insurance Provider Directly

Calling the customer service number on your card gives you direct answers from people who can look up your exact account status. Expect to spend 20-40 minutes on this call, including hold time. That's not wasted time if it saves you $500 in surprise bills.

Before dialing, write out your questions. "Does my plan cover crowns?" gets you nowhere. Instead: "I need code D2740 on tooth #14. What's my coinsurance percentage? What's my remaining annual maximum? Have I met this year's deductible?" See the difference? Specific numbers for specific procedures.

Get a reference number before hanging up. Every insurance company tracks customer service calls in their system. When representatives provide benefit estimates, they're noting that information in your account file. If something goes wrong later—if they told you 80% coverage but only paid 50%—that reference number is your evidence. Write down the date, time, representative's name, and reference number.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Document your conversation in detail the moment you hang up. Scribble notes about percentages, dollar amounts, limitations discussed, special conditions mentioned. Your memory will fail you in three weeks when you're trying to remember whether she said "after deductible" or "including deductible." Those two words cost you $100.

One critical warning: phone estimates aren't guaranteed payments. Customer service representatives tell you what your plan typically covers based on the codes and information you provided. When your actual claim gets processed weeks later, additional limitations might surface that nobody mentioned. Always ask, "What could cause the final payment to differ from this estimate?" Their answer reveals potential complications.

Using Your Insurer's Online Portal or App

Most major dental insurers now run digital platforms where you can check benefits without calling anyone. These portals give you 24/7 access to your coverage details, though they work better for straightforward questions than complex scenarios.

Setting up your account requires your policy number and identity verification—usually answering security questions or entering a code they text to your phone. First-time setup takes about ten minutes. Once you're in, bookmark the login page and store your password somewhere you'll remember it. Writing it in a notebook that stays in your desk drawer works better than digital password managers if you're not tech-savvy.

Look for sections labeled "My Benefits," "Coverage Summary," or "Plan Details." Portal layouts vary wildly, but most show your key numbers prominently: deductible status, remaining annual maximum, basic coverage percentages. You can see at a glance that you've used $627 of your $1,500 maximum, or that you still owe $43 toward your $50 deductible.

Some advanced portals let you enter procedure codes for custom estimates. Type in "D2740" and it calculates your expected cost based on your current benefit status. These estimates often beat phone estimates for accuracy because the system automatically accounts for your remaining maximum, deductible status, and frequency limitations.

Download your benefits summary as a PDF. Having written documentation of your coverage helps when discussing treatment costs with your dental office. These summaries include effective dates too, confirming your policy is actually active and not lapsed due to a missed premium payment.

Check when the system was last updated. Some portals show real-time information; others refresh overnight or weekly. If you had a major claim processed yesterday, today's portal might not reflect that change yet. Look for "as of [date]" timestamps on your benefit displays.

Having Your Dental Office Verify for You

Patients constantly mix up benefit verification and pre-authorization, thinking they're interchangeable. They're not. When I verify benefits, I'm asking what the patient's plan generally covers. When I get pre-authorization, the insurance company commits in writing to covering this specific treatment plan for this specific patient. For anything complicated or costly, skip the verification shortcut and get pre-authorization. Yes, it delays treatment by a couple weeks, but it also eliminates billing arguments later

— Jennifer Martinez

Many dental practices employ staff specifically trained to navigate insurance systems—treatment coordinators who handle benefit verification all day, every day. They know exactly which questions to ask and which red flags indicate potential coverage problems.

Hand over your insurance card when you schedule your appointment, not when you arrive for treatment. The front desk needs time to call your insurance company and gather information. Last-minute verifications on the day of your appointment often produce incomplete information because staff are juggling multiple patients.

Understand that offices verify as a courtesy to help you plan financially. They're not guaranteeing what your insurance will pay. The actual contract exists between you and your insurance company, period. If the insurance pays less than estimated, you're still responsible for the balance. Dental offices relay the information insurance companies provide, but they can't control how claims get processed weeks later.

Request a written treatment plan showing estimated costs. After verifying your benefits, the office should give you a breakdown: total cost $800, insurance estimated to pay $600, your estimated portion $200. Study this estimate. If something looks wrong or confusing—maybe you thought your coinsurance was 20% but they calculated 30%—ask immediately. Clearing up misunderstandings before treatment beats arguing about bills afterward.

For expensive work, don't settle for verbal verification alone. Crowns, root canals, periodontal surgery, anything over $500—these procedures warrant pre-authorization. Your dentist submits detailed treatment plans and X-rays to your insurance company before starting work. The insurer reviews everything and issues a formal determination of benefits. This process adds one to three weeks but removes guesswork from major expenses.

Key Coverage Details to Confirm

Knowing your policy number means nothing if you don't know what questions to ask. These coverage elements directly determine how much you'll pay out-of-pocket, yet most patients never think to ask about them.

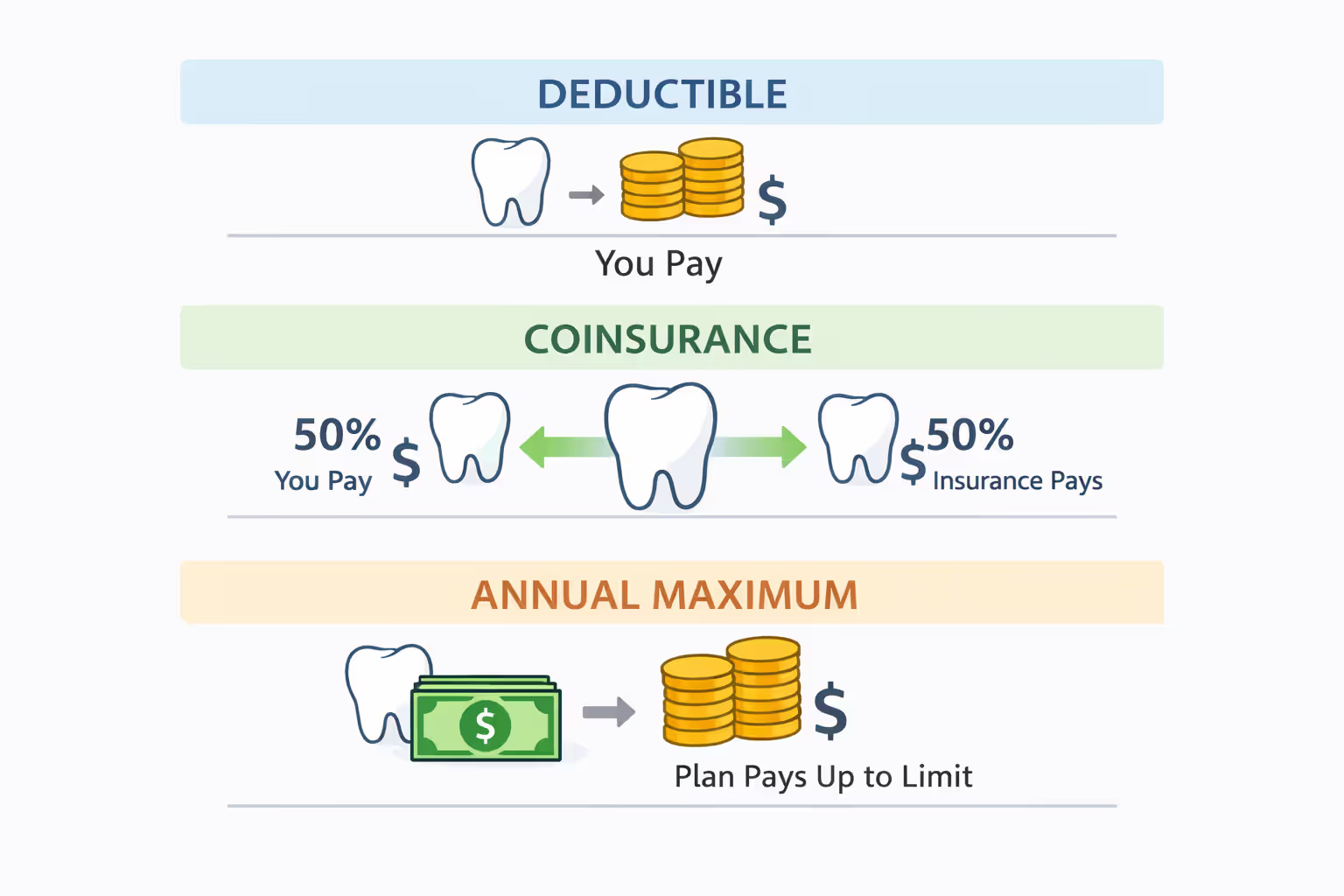

Annual maximums cap what your insurance pays each year—usually $1,000 to $2,000, though some generous employer plans go higher. Once you hit that ceiling, you're paying 100% of everything else until your plan year resets. If you've already spent $1,400 of your $1,500 maximum and need a $600 crown, your insurance pays $100. You pay $500. Ask two questions: "What's my total annual maximum?" and "How much remains available right now?"

Author: Ashley Whitford;

Source: ladylesliebelize.com

Deductibles force you to pay a set amount before coverage kicks in. Your plan might require you to spend the first $50 or $100 each year before insurance pays anything. Some plans have one deductible for the whole family, others have individual deductibles per person. Occasionally, preventive services like cleanings skip the deductible while other work requires meeting it first. Nail down whether you've already satisfied your deductible this year.

Coinsurance means you split costs with your insurance company by percentage. The insurance covers 80%, you cover 20%. That's coinsurance. Most dental plans use this structure, with different splits for different service categories: preventive work gets 100% coverage, basic procedures get 70-80%, major work gets 50%. These percentages apply after you've met your deductible. Some plans use co-pays instead—flat fees like $25 per visit—but that's less common for dental coverage. Clarify which cost-sharing method applies and what the percentages or amounts are.

Waiting periods block coverage for certain services when your policy is new. Switch jobs and get new dental insurance? That's great, except major services like crowns, bridges, and root canals might have 6-12 month waiting periods. Basic services might have 3-6 month waits. Preventive care usually starts immediately. If you recently changed coverage or just enrolled for the first time, ask point-blank: "Do any waiting periods apply to the procedures I need?"

Frequency limitations restrict how often you can get specific treatments. Insurance covers two cleanings per year, meaning every six months minimum between appointments. Full mouth X-rays? Once every three years, maybe five years depending on the plan. Fluoride treatments for adults? Many plans say no, or once per year at most. Trying to schedule your third cleaning this year? Don't expect insurance to pay for it.

In-network versus out-of-network makes or breaks your budget. In-network dentists have contracts with your insurance company agreeing to charge specific rates. These contracted rates are usually lower, plus your coinsurance percentage is typically better—maybe 80% in-network versus 60% out-of-network. Out-of-network dentists charge whatever they want, and your insurance bases their payment on "usual and customary" rates that might be substantially lower than the actual bill. The same crown might cost you $300 in-network but $700 out-of-network.

Missing tooth exclusions trip up people who get insurance to fix existing problems. Lost a tooth before your coverage started? Many plans won't pay to replace it, arguing that tooth was "missing prior to the effective date of coverage." This clause prevents people from buying insurance only after they need expensive work. If you're hoping insurance will cover an implant or bridge for a tooth you lost years ago, verify this specifically. The answer might disappoint you.

Common Verification Mistakes to Avoid

Even careful patients make verification errors that cost them money. These mistakes are surprisingly common, and knowing about them helps you dodge problems others stumble into repeatedly.

Never assume basic coverage equals comprehensive coverage. Having "dental insurance" doesn't mean everything is covered. Plans routinely exclude cosmetic procedures—teeth whitening, veneers for appearance only, gum reshaping. Adult orthodontics? Most plans exclude it or severely limit coverage. Implants? Some plans cover them, many don't. TMJ treatment? Often excluded. Every single procedure needs individual verification, especially if it's anything beyond routine cleanings and fillings.

Skipping pre-authorization on major work is budget suicide. That $2,500 crown or $1,800 root canal deserves more than a five-minute benefits call. Pre-authorization means your dentist submits the complete treatment plan, X-rays, and clinical notes to your insurance company before starting. The insurer reviews everything and tells you exactly what they'll pay. This step takes extra time—usually two weeks—but eliminates surprise bills on expensive procedures. For anything over $500, insist on pre-authorization no matter how confident your dentist's office seems about coverage.

Accepting verbal confirmations without written backup creates problems when memories conflict. You remember the representative saying 80% coverage; they claim you were told 60%. Who's right? Without documentation, you're stuck. Always get benefit information in writing—portal screenshots, emailed confirmations, or at minimum detailed notes with a reference number. Written records beat memory every time in billing disputes.

Forgetting to check effective dates causes preventable claim denials. Your coverage might not start until the first day of the month following your hire date. Or maybe you submitted the enrollment paperwork late, delaying your effective date. If you schedule treatment for September 20th but your coverage doesn't begin until October 1st, you're paying out-of-pocket. Confirm your policy is active on the specific date of your scheduled treatment.

Ignoring coordination of benefits when you have dual coverage wastes money. Both you and your spouse have dental insurance through your respective employers? Fantastic—but you need to understand which plan pays first (primary) and how the second plan (secondary) processes claims. Sometimes the secondary plan covers what the primary didn't, dramatically reducing your out-of-pocket costs. Other times, coordination of benefits rules limit the total combined payment to less than you'd hope. Ask how your multiple policies work together.

Accepting vague, general answers instead of demanding specifics gives you useless information. "Your plan covers crowns"—okay, but at what percentage? After the deductible? On any tooth or just certain ones? How much of my annual maximum is left to apply toward it? Is my dentist in-network for this procedure? Keep pushing until you have actual numbers and clear limitations. Vague answers protect nobody when the bill arrives.

What to Do If Coverage Is Denied or Unclear

Sometimes verification delivers bad news—your procedure isn't covered, or the coverage is far less generous than you expected. Sometimes you go ahead with treatment and then face a claim denial. You've got options beyond just accepting the decision and paying the full bill.

Demand a written Explanation of Benefits (EOB) if you receive verbal denial or confusing information. The EOB document spells out exactly what the insurance company paid, what they denied, and the specific reason for denial. This isn't a bill—it's an official statement from your insurance company showing how they processed the claim. The EOB includes denial codes that explain the problem: procedure not covered under your plan, frequency limitation exceeded, missing pre-authorization, provider out-of-network. You can't fight a denial effectively without understanding the specific reason behind it.

Learn your appeal rights and deadlines. Every denial notice includes information about filing an appeal, usually giving you 180 days from the denial date. Missing this deadline often means losing your appeal rights entirely. Appeals require submitting additional documentation—typically a letter explaining why you believe the claim should be covered, along with supporting materials from your dentist.

Author: Ashley Whitford;

Source: ladylesliebelize.com

Recruit your dentist's office to help with appeals. They handle insurance denials constantly and often keep template appeal letters and supporting documentation ready to go. Your dentist can write a letter explaining the clinical necessity of the treatment, attach X-rays showing the problem, include clinical notes documenting the issue, and cite treatment guidelines supporting their recommendation. Insurance companies take these professional appeals more seriously than patient letters alone. Many initially denied claims get approved when a dentist provides thorough clinical justification.

Explore financing if insurance won't budge and you need the treatment anyway. Many dental offices offer in-house payment plans—pay $100-200 monthly until the balance is covered, often with no interest if you complete payments within a set timeframe. Third-party companies like CareCredit provide healthcare credit cards with promotional financing periods (6-24 months interest-free if you pay the balance off during that period). Some dentists offer modest discounts—5-10%—if you pay the entire bill upfront in cash.

Check whether your secondary insurance might cover what your primary denied. Having two insurance policies doesn't guarantee the second one will pay what the first rejected, but it's worth checking. Submit the EOB from your primary insurance to your secondary carrier along with the original claim. The secondary insurance processes the claim according to their own coverage rules, which might differ from your primary plan.

Consider timing adjustments if you're bumping against annual maximums or haven't met your deductible yet. Near your $1,500 maximum in November? Waiting until January when your benefits reset might mean full coverage instead of minimal payment. Haven't touched your deductible but need multiple procedures? Scheduling everything within the same few weeks means you meet the deductible once rather than paying small amounts repeatedly throughout the year.

Verify correct procedure coding before assuming a legitimate denial. Sometimes claims get rejected because of coding errors, not actual coverage limitations. Perhaps your dentist coded a D2391 when the correct code should've been D2392—one character difference, potentially different coverage. Your dental office can review the coding with your insurance company and resubmit with corrections if appropriate. This simple fix resolves many "denials" that weren't really about coverage at all.

Verification Methods Compared

| Method | Time Investment | Accuracy Level | Documentation You Receive | Works Best When |

| Calling Insurance Directly | 20-45 minutes including hold times and conversation | Depends heavily on rep's knowledge and how detailed your questions are | Just a reference number; requires you to take detailed notes | You need complex explanations, want to ask follow-up questions immediately, or have unusual coverage situations |

| Online Portal or Mobile App | 5-15 minutes once account is set up | Excellent for straightforward benefit checks; limited for complicated scenarios | Downloadable PDF summaries showing coverage details | You want quick confirmation of basic benefits, deductible status, or remaining annual maximum |

| Dental Office Handles It | No time required from you—handled before your appointment | Generally high because experienced coordinators know which questions matter | Written treatment estimate with cost breakdown | You prefer someone experienced handle the details, have a complex treatment plan, or find insurance confusing |

Frequently Asked Questions About Verifying Dental Insurance

Spending 30 minutes confirming your dental coverage before committing to treatment ranks among the simplest ways to avoid healthcare billing nightmares. The effort requires gathering specific policy details, knowing which questions actually matter, and recording the answers you receive. Whether you handle verification personally by calling or using digital tools, or you rely on your dental office to manage this for you, the goal remains identical: get real numbers and clear limitations before treatment starts.

Choose your verification approach based on how comfortable you are with insurance terminology, how complex your upcoming treatment is, and how much time you have before your appointment. Quick portal checks work fine for confirming your deductible status before a routine cleaning. Major procedures—anything involving substantial cost or complexity—deserve deeper investigation through phone calls where you can probe for details and request pre-authorization.

Remember that even thorough verification provides estimates, not ironclad payment guarantees. Insurance companies make final determinations when they process actual claims, sometimes discovering limitations that weren't obvious during initial verification. However, careful verification dramatically reduces surprise bills and gives you documentation if the final claim processing contradicts what you were originally told.

Your oral health matters too much to let insurance confusion block you from necessary care. By learning the verification process, you remove financial uncertainty and focus on what truly matters—maintaining healthy teeth and gums. That half-hour investment in understanding your benefits can save you hundreds or thousands of dollars and eliminate hours of frustration arguing about unexpected charges.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.