Modern dental office with dental chair and two insurance policy documents on a desk symbolizing primary and secondary dental coverage

Secondary Dental Insurance with No Waiting Period Guide

Dental expenses can quickly overwhelm even the most generous insurance plan. A single root canal or crown often exceeds what primary coverage will pay, leaving patients with bills that run into hundreds or thousands of dollars. Secondary dental insurance offers a way to close these gaps, but most plans force you to wait weeks or months before accessing benefits for major procedures. Understanding how to secure secondary dental insurance with no waiting period can mean the difference between delaying necessary treatment and getting the care you need immediately.

What Is Secondary Dental Insurance?

Secondary dental insurance is a supplemental policy that pays benefits after your primary dental plan has processed a claim. Think of it as a backup layer of coverage designed to reduce or eliminate the out-of-pocket costs your first insurance doesn't cover.

When you visit the dentist, your primary insurance pays first according to its coverage rules and benefit limits. The secondary plan then reviews what remains unpaid—deductibles, coinsurance, amounts exceeding annual maximums—and pays a portion or all of that balance based on its own policy terms.

Dental secondary insurance differs from primary coverage in one critical way: it never acts as the first payer. The coordination of benefits (COB) rules embedded in insurance contracts determine which plan is primary and which is secondary. These rules prevent double-dipping, where someone might collect more than the actual cost of care by filing the same claim with multiple insurers.

Most people encounter secondary dental coverage through a spouse's employer plan. If both you and your partner have dental insurance through your respective jobs, one plan becomes primary and the other secondary. The birthday rule typically determines order: the plan belonging to the person whose birthday falls earlier in the calendar year usually pays first for dependent children. For the policyholder themselves, their own employer's plan is always primary.

Understanding what is secondary dental insurance helps you realize it's not about having twice the coverage—it's about filling the gaps your primary plan leaves behind.

How Primary and Secondary Dental Insurance Work Together

The coordination process follows a specific sequence. Your dentist submits the claim to your primary insurer first. That company processes it according to its fee schedule, deductible requirements, coinsurance percentages, and annual maximum limits. Once the primary insurer issues an Explanation of Benefits (EOB) showing what they paid and what you owe, the dental office then submits the remaining balance to your secondary insurance.

The secondary plan doesn't simply pay whatever is left. It calculates what it would have paid if it were the primary insurer, then subtracts what the primary plan already paid. You receive the difference, up to the remaining balance of your bill.

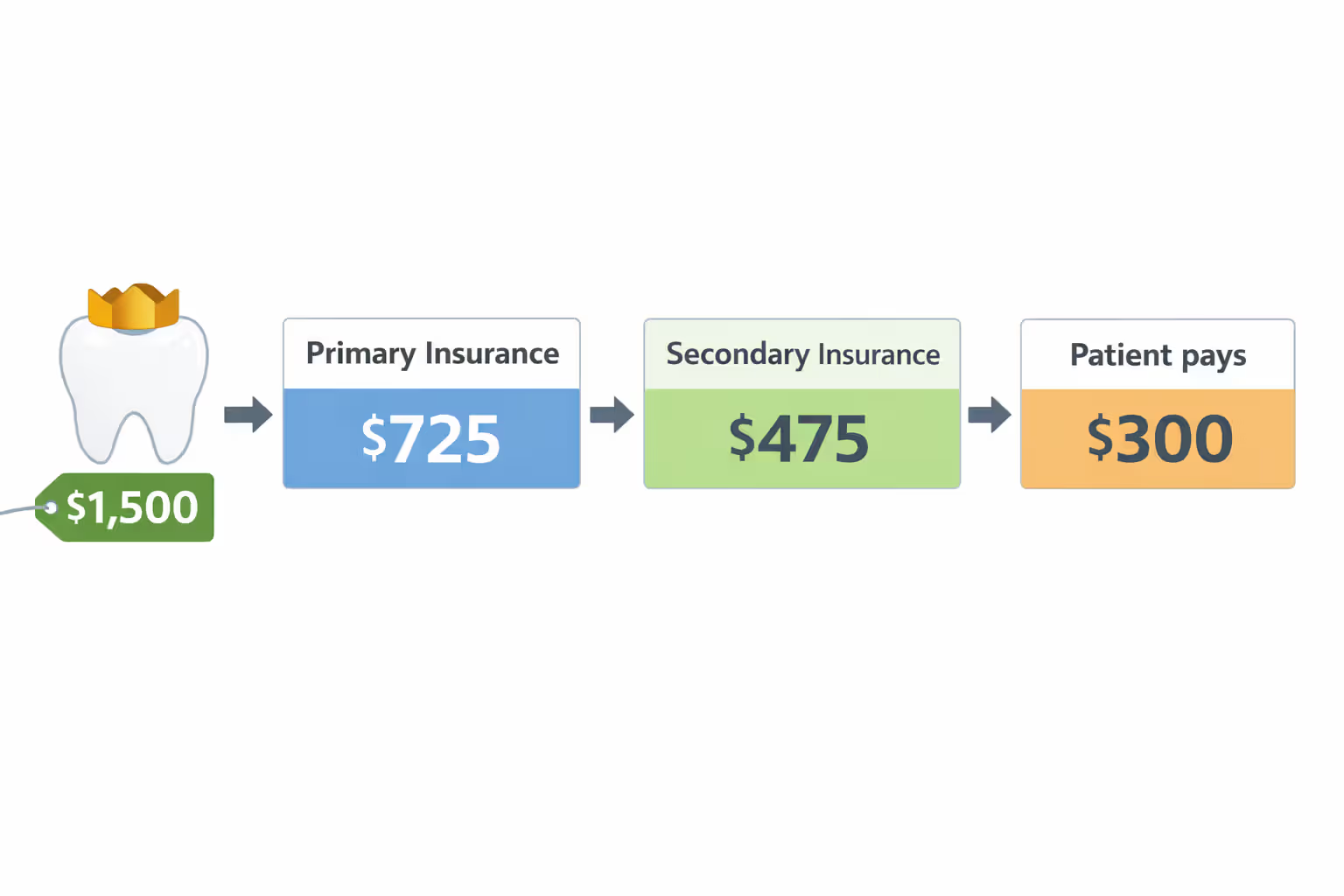

Here's a concrete example: You need a crown costing $1,500. Your primary insurance covers 50% of major procedures after a $50 deductible, paying $725. You still owe $775. Your secondary plan covers 80% of major work with no deductible. It calculates 80% of $1,500 ($1,200), subtracts the $725 your primary plan paid, and sends you $475. Your final out-of-pocket cost drops from $775 to $300.

Author: Tyler Grant;

Source: ladylesliebelize.com

Primary and secondary dental insurance rules vary by state and contract, but the payment order remains consistent: primary always pays first, secondary fills gaps within its own coverage limits.

Common Coordination of Benefits Scenarios

When both plans come from employer group coverage, coordination is straightforward. The insurers communicate directly, and your dentist's office handles most of the paperwork. The process takes longer—expect 30 to 60 days for full reimbursement instead of the usual two weeks—but requires little effort on your part.

Complications arise when one plan is employer-sponsored and the other is an individual policy. Some individual dental plans explicitly exclude coordination of benefits or refuse to act as secondary coverage. Read the policy documents carefully before purchasing an individual plan as secondary insurance for dental needs.

Medicare creates another scenario. Original Medicare (Parts A and B) doesn't cover routine dental care. If you have a Medicare Advantage plan with dental benefits and a separate dental policy, the Advantage plan typically pays first because it's considered primary health coverage. Your standalone dental plan becomes secondary, but again, check whether it accepts this arrangement.

Coverage Limits and Out-of-Pocket Costs

Each plan maintains its own annual maximum, usually between $1,000 and $2,000. Having secondary dental insurance coverage doesn't double these limits. If your primary plan has a $1,500 annual maximum and your secondary has $1,200, you can't access $2,700 in benefits. Instead, once your primary maximum is exhausted, your secondary plan may cover additional expenses up to its own maximum—but only if its policy terms allow this.

Some secondary plans include a "non-duplication of benefits" clause. This provision prevents the secondary insurer from paying anything if the primary plan's coverage meets or exceeds what the secondary plan would have paid. These clauses effectively neutralize secondary coverage in many situations, making them poor value for the premium cost.

Understanding Waiting Periods in Dental Insurance

Waiting periods are time delays between when your coverage starts and when you can use certain benefits. Insurers impose them to prevent adverse selection—the practice of buying insurance only when you know you'll need expensive care soon.

Preventive services like cleanings and exams typically have no waiting period. You can use these benefits immediately after your effective date. Basic procedures such as fillings usually require a three to six-month wait. Major services like crowns, bridges, and root canals often carry 12-month waiting periods. Orthodontic coverage may require waiting 12 to 24 months.

These delays significantly impact access to care. If you need a crown and enroll in a new dental insurance secondary plan with a 12-month waiting period, you'll either pay the full cost out-of-pocket or postpone treatment for a year. For urgent dental problems, neither option is acceptable.

Insurers use waiting periods to ensure they collect more in premiums than they pay out in claims during the first policy year. Without these restrictions, people would sign up right before scheduled procedures, collect benefits, then cancel coverage—a pattern that would make dental insurance financially unsustainable.

The impact extends beyond immediate care needs. Waiting periods reset if you let coverage lapse. Missing a premium payment by even a few days can restart the clock, forcing you to wait another full year for major services.

How to Get Secondary Dental Insurance Without Waiting Periods

Finding secondary dental insurance no waiting period requires targeting specific enrollment opportunities and plan types. Start by checking whether your employer offers multiple dental plan options during open enrollment. Some companies provide both a basic and a premium plan. Enrolling in the premium option during your initial eligibility period or annual open enrollment typically waives waiting periods.

Spousal coverage through a partner's employer represents the most common path to secondary dental coverage without delays. When you gain eligibility due to a qualifying life event—marriage, birth of a child, loss of other coverage—insurers often waive waiting periods. You must enroll within 30 to 60 days of the qualifying event to receive this benefit.

Author: Tyler Grant;

Source: ladylesliebelize.com

Individual dental plans rarely waive waiting periods for new enrollees, but exceptions exist. Some insurers offer "immediate coverage" plans with higher premiums that provide full benefits from day one. These plans cost 30% to 50% more than standard policies but make financial sense if you have known dental needs.

Professional associations and alumni groups sometimes negotiate group dental plans for members. These plans may feature reduced waiting periods or none at all because the group's collective bargaining power and larger risk pool allow insurers to relax restrictions.

The enrollment process requires gathering documentation: proof of primary coverage, identification, and payment information. Most insurers now offer online enrollment, but speaking with a licensed insurance broker can reveal options you won't find through direct consumer websites.

Types of Plans That May Waive Waiting Periods

Dental Health Maintenance Organizations (DHMOs) frequently eliminate waiting periods. These plans require you to choose a primary dentist from a network and get referrals for specialist care. The trade-off for immediate coverage is reduced flexibility and potentially lower reimbursement rates.

Discount dental plans aren't insurance but membership programs that provide reduced fees at participating dentists. They have no waiting periods because they don't pay claims—you pay the dentist directly at a discounted rate. These plans cost $100 to $300 annually and can serve as effective secondary coverage if your primary insurance has reached its annual maximum.

Indemnity plans, also called traditional dental insurance, sometimes waive waiting periods for employer groups. These plans let you visit any dentist without network restrictions. Premiums run higher, but the flexibility and immediate access to benefits justify the cost for people who need extensive dental work.

Employer-Sponsored vs. Individual Plans

Employer-sponsored plans almost always waive waiting periods during initial enrollment or qualifying events. Group coverage spreads risk across many employees, allowing insurers to offer immediate benefits without excessive financial exposure. If you have access to dental insurance through your job and your spouse has coverage through theirs, you've found the most straightforward path to secondary dental insurance with no waiting period.

Individual plans require more careful evaluation. Most impose standard waiting periods, but a few carriers offer immediate-coverage options. Expect to pay premiums 40% to 60% higher than standard individual plans. Run the numbers: if you need $3,000 in dental work and an immediate-coverage plan costs $80 per month versus $50 for a standard plan with a 12-month waiting period, you'll pay an extra $360 annually but gain access to benefits worth potentially $1,500 or more after your primary insurance pays its share.

When Secondary Dental Coverage Makes Financial Sense

Secondary coverage justifies its cost in specific situations. If your primary plan has a low annual maximum—say $1,000—and you anticipate needing more than that in care, a secondary plan can prevent large out-of-pocket expenses. Calculate your expected dental costs for the year, subtract what your primary plan will pay, then compare that gap to the annual premium cost of secondary coverage.

Families with children facing orthodontic treatment benefit significantly from dual coverage. Braces cost $5,000 to $7,000, and most primary plans cover only 50% up to a lifetime maximum of $1,500. A secondary plan that covers another 50% up to its own maximum can save thousands.

Author: Tyler Grant;

Source: ladylesliebelize.com

People with chronic dental issues—gum disease, frequent cavities, previous extensive dental work requiring maintenance—should strongly consider secondary dental insurance. Your dentist can provide a treatment plan with cost estimates for the coming year, giving you concrete numbers for comparison.

The math works less favorably for healthy adults who need only preventive care. If you visit the dentist twice yearly for cleanings and exams, your primary insurance likely covers 100% of these services. Adding secondary coverage would cost $300 to $600 annually with no benefit.

Common mistakes include buying secondary coverage too late. If you wait until you need expensive dental work, you'll face waiting periods that negate the policy's value. The time to secure coverage is when you don't immediately need it—during open enrollment periods or qualifying life events when waiting periods are waived.

Another error is failing to verify coordination of benefits. Some policies explicitly state they won't coordinate with other dental coverage or will only act as primary insurance. Reading the policy documents before purchasing prevents expensive surprises.

Comparing Secondary Dental Insurance Options

Secondary dental coverage works best when you secure it before you need it.The clients who benefit most are those who enroll during employer open enrollment periods or right after marriage, when waiting periods are waived. Trying to add secondary coverage after learning you need a crown or bridge means paying premiums for a year before accessing benefits—a strategy that rarely makes financial sense

— Jennifer Martinez

Evaluating dental secondary insurance requires examining several factors beyond premium cost. Coverage percentages matter significantly: a plan that covers 80% of major procedures provides more value than one covering 50%, even if the premium is slightly higher.

Annual maximums create a ceiling on benefits. A plan with a $2,000 maximum might seem generous, but if your primary plan already has a $1,500 maximum and you need $4,000 in dental work, you'll still face substantial out-of-pocket costs. Look for plans with maximums of at least $1,500 to $2,000 to ensure meaningful gap coverage.

Network size affects convenience and cost. Preferred Provider Organization (PPO) plans offer the best balance: you can visit any dentist, but staying in-network reduces your costs. Verify your current dentist accepts the secondary plan you're considering. Switching dentists to accommodate insurance rarely makes sense unless you're dissatisfied with your current provider.

Claim filing requirements vary. Some insurers handle coordination of benefits automatically once they receive the primary plan's EOB. Others require you to submit claims manually, a time-consuming process that can delay reimbursement by weeks or months.

Deductibles on secondary plans add another variable. A plan with no deductible provides more immediate value than one requiring $50 or $100 out-of-pocket before benefits begin, especially for basic procedures.

Here's a comparison of common secondary dental insurance plan structures:

| Plan Type | Waiting Period | Monthly Premium Range | Major Procedures Coverage | Best For |

| Employer Group (Spouse) | Usually waived at enrollment | $15–$40 | 50%–80% after primary | Families with dual employer coverage |

| Individual PPO (Standard) | 12 months for major | $30–$60 | 50% after primary | Healthy adults planning ahead |

| Individual PPO (Immediate) | None | $50–$90 | 50% after primary | People with known upcoming needs |

| DHMO | None | $10–$25 | 50%–80% after primary | Budget-conscious with flexible provider preferences |

Frequently Asked Questions About Secondary Dental Insurance

Secondary dental insurance with no waiting period provides immediate financial protection against gaps in primary coverage, but securing this benefit requires strategic timing and careful plan selection. Employer-sponsored coverage accessed during open enrollment or qualifying life events offers the most reliable path to waiving waiting periods. Individual plans with immediate coverage exist but command premium prices that make sense only when you face known dental expenses in the near term.

The coordination of benefits between primary and secondary plans follows predictable rules, yet the actual value depends on coverage percentages, annual maximums, deductibles, and non-duplication clauses that vary widely among insurers. Running the numbers based on your specific dental needs—not generic assumptions—reveals whether dual coverage justifies its cost.

For families facing orthodontic expenses, people with chronic dental problems, or those whose primary plans carry low annual maximums, secondary coverage delivers measurable savings. Healthy adults who need only preventive care typically gain little value from the added expense. The key is matching coverage to actual needs, securing it when waiting periods can be waived, and understanding exactly how your two plans will coordinate before you need expensive dental work.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.