Dental insurance documents with dental tools, calculator and dollar bills on a light desk, top view

What Is Dental Insurance Reimbursement?

Navigating dental insurance can feel like decoding a foreign language, especially when your dentist's office tells you they don't file claims directly with your insurer. Instead, you'll need to pay upfront and wait for reimbursement. Understanding this payment model saves you from surprise bills and helps you budget for dental care more effectively.

Understanding Dental Insurance Reimbursement

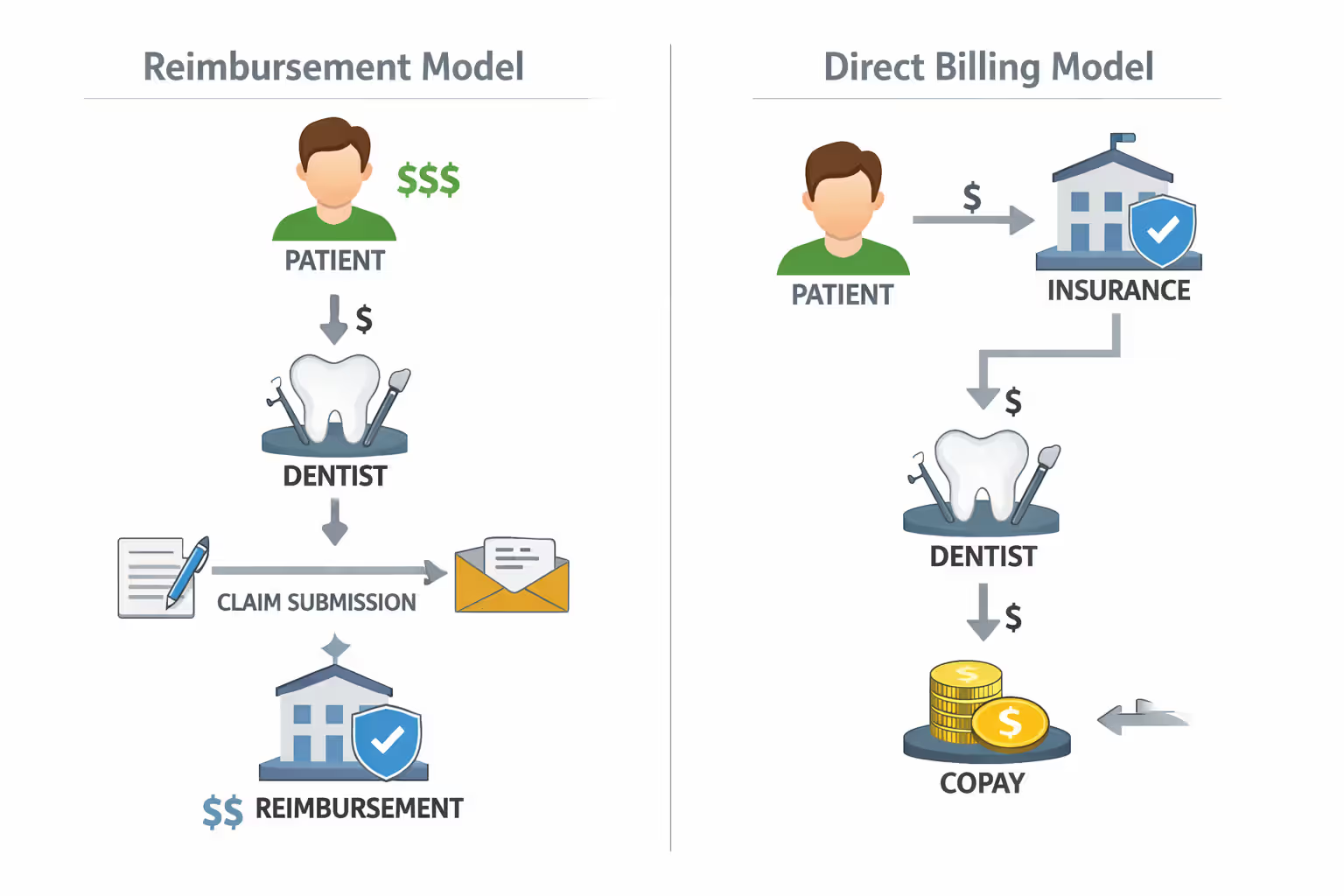

Dental insurance reimbursement meaning centers on a payment model where you, the patient, pay your dentist directly for services, then submit a claim to your insurance company for partial or full repayment. This differs fundamentally from direct payment models, where your dentist bills the insurance company directly and you only pay your portion at checkout.

What is dental insurance reimbursement in practical terms? Think of it like filing an expense report at work. You cover the cost initially, provide documentation proving the expense was legitimate and covered under your policy, then receive money back according to your plan's terms.

The reimbursement model appears most frequently when you visit out-of-network providers. In-network dentists typically have agreements with insurance companies to handle billing directly and accept negotiated rates. Out-of-network dentists have no such contract, meaning they can charge their full fees and aren't obligated to file insurance paperwork on your behalf.

Even with in-network providers, certain situations trigger reimbursement scenarios. Some dental offices require upfront payment for major procedures like crowns or bridges, then help you file for reimbursement afterward. Others use this model for patients with out-of-state insurance plans or less common carriers.

The financial difference between in-network and out-of-network reimbursement can be substantial. In-network providers accept your insurance company's maximum allowable charge as full payment. Out-of-network dentists charge whatever they want, and your insurance reimburses based on their fee schedule—often leaving you responsible for the difference. A crown costing $1,400 might generate a $700 reimbursement check if your insurance considers $1,000 the "usual and customary" rate and covers 70% of major procedures. You'd still owe the dentist $1,400, making your out-of-pocket cost $700 instead of the $300 you'd pay in-network.

Author: Daniel Mercer;

Source: ladylesliebelize.com

How the Dental Insurance Reimbursement Process Works

How does dental insurance reimbursement work from start to finish? The process involves several distinct phases, each with its own requirements and potential delays.

Step-by-Step Reimbursement Timeline

Your reimbursement journey begins at checkout. After your dental appointment, you pay the full bill—either with cash, credit card, or financing. Request an itemized receipt showing procedure codes (called CDT codes), the date of service, your dentist's information, and the total amount paid.

Within a few days, gather your claim form. Most insurance companies provide downloadable forms on their websites, or you can request one by phone. Some insurers accept claims through mobile apps or online portals, eliminating paper forms entirely.

Author: Daniel Mercer;

Source: ladylesliebelize.com

Complete the patient information section carefully. Errors in your policy number, date of birth, or address cause processing delays. Your dentist must complete their section, including their National Provider Identifier (NPI) number, tax ID, and clinical notes justifying the treatment.

Submit your claim via your insurer's preferred method—mail, fax, email, or online portal. Keep copies of everything. This step happens anywhere from the same day as your appointment to several weeks later, depending on how quickly you compile documentation.

The insurance company receives and processes your claim, typically within 2-5 business days of arrival. A claims adjuster reviews the submission for completeness, verifies your coverage was active on the service date, and checks that the procedures fall within your plan's covered services.

Processing time varies by carrier and claim complexity. Simple claims for preventive care might process in 10-14 days. Complex claims requiring review of X-rays or clinical notes can take 30-45 days. If the insurer needs additional information, they'll send a request, pausing the clock until you respond.

Once approved, the insurance company issues payment. Depending on your plan, they might send the check directly to you or to your dentist. If sent to your dentist, you'll receive an Explanation of Benefits (EOB) detailing what was paid. The entire cycle from submission to payment typically spans 2-6 weeks for straightforward claims.

Required Documentation for Claims

Successful reimbursement hinges on complete documentation. At minimum, you need a completed claim form (ADA form for dental claims), itemized receipt from your dentist, and sometimes X-rays or clinical notes.

The itemized receipt must show specific CDT codes—not just descriptions like "filling." Insurance companies need codes like D2391 for a resin-based composite filling on one surface of a posterior tooth. Generic descriptions trigger automatic denials.

For major procedures, insurers often require pre-treatment X-rays, periodontal charts, or narrative explanations from your dentist. A crown claim might need X-rays showing the tooth's condition before treatment and a note explaining why a filling wouldn't suffice.

Keep your EOB from every claim. These documents track your annual maximum usage and deductible status. When filing subsequent claims, you'll know exactly how much coverage remains.

The number one reason reimbursement claims get delayed is incomplete dentist information. Patients forget to have their dentist fill out their section of the form completely, especially the NPI and tax ID numbers. Without these, we can't process the claim at all

— Rebecca Martinez

What Dental Procedures Are Covered Under Reimbursement Plans

What does dental insurance reimbursement cover? Most plans categorize procedures into three tiers, each with different coverage levels.

Preventive care forms the foundation of dental coverage. This category includes routine exams, cleanings (prophylaxis), fluoride treatments for children, and X-rays. Most plans cover preventive services at 100%, though some require a small copay. These services typically don't count against your annual maximum, encouraging regular dental visits.

Basic procedures address common dental problems. Fillings, simple extractions, root canals on front teeth, and periodontal maintenance fall into this category. Coverage usually ranges from 70-80% after you meet your deductible. A $200 filling might cost you $40-60 out of pocket.

Major procedures involve significant restoration or replacement of teeth. Crowns, bridges, dentures, implants (when covered), root canals on molars, and oral surgery belong here. Plans typically cover 50% of major work, and these procedures count heavily against your annual maximum.

Dental insurance reimbursement coverage explained includes understanding what's excluded. Cosmetic procedures like teeth whitening or veneers for aesthetic purposes rarely receive coverage. Orthodontics often requires a separate rider or isn't covered at all on adult plans. Services deemed "not medically necessary" by the insurer won't generate reimbursement, even if your dentist recommended them.

Annual maximums cap total coverage per calendar year, typically ranging from $1,000 to $2,500. Once you've received this amount in benefits, you're responsible for 100% of additional costs until the next year. Some high-end plans offer unlimited preventive care while maintaining maximums for basic and major work.

Reimbursement Rates and Coverage Levels Explained

Insurance companies calculate reimbursement amounts using several methods, and understanding these formulas prevents surprise shortfalls.

Most plans use UCR (Usual, Customary, and Reasonable) fee schedules. The insurance company surveys dental costs in your geographic area and establishes maximum amounts they'll recognize for each procedure. Your dentist might charge $1,500 for a crown, but if the UCR rate is $1,200, your insurance calculates your benefit based on $1,200—not the actual charge.

Percentage-based coverage applies after determining the recognized fee. If your plan covers major procedures at 50% and the UCR rate for your crown is $1,200, your reimbursement check will be $600. You owe your dentist the full $1,500, making your actual cost $900.

Some plans use fixed fee schedules instead of UCR rates. These plans list exactly what they'll pay for each procedure code—say, $500 for a crown regardless of what your dentist charges. This approach creates more predictable reimbursements but often pays less than UCR-based plans.

Deductibles reduce your reimbursement on the first claims of the year. With a $50 deductible, your first filling of the year costs you the deductible plus your coinsurance percentage. Preventive care usually bypasses the deductible.

| Procedure Category | Typical Coverage Percentage | Example Procedures | Average Annual Maximum Impact | Patient Cost Example (out-of-network) |

| Preventive Care | 100% | Cleanings, exams, X-rays, fluoride | Usually excluded from maximum | $0 (if UCR rate matches dentist fee) |

| Basic Procedures | 70-80% | Fillings, simple extractions, sealants | Low to moderate | $60 for a $300 filling (80% plan) |

| Major Procedures | 50% | Crowns, bridges, dentures, implants | High—often exhausts maximum | $900 for a $1,500 crown (50% of $1,200 UCR) |

Common Reimbursement Claim Mistakes to Avoid

Filing deadlines trip up many patients. Most insurance plans require claim submission within 90 days to one year of service. Miss this window and you forfeit reimbursement entirely, even for covered services. Mark your calendar when you pay for dental work and don't procrastinate on filing.

Incomplete forms generate automatic denials or requests for additional information, delaying payment by weeks. Double-check that every required field is filled out. Missing signatures, blank date fields, or omitted procedure codes force the claim back to you for corrections.

Lack of pre-authorization for major procedures can result in denied claims. Many plans require you to submit treatment plans for procedures costing over a certain threshold—often $300-500—before the work is performed. The insurer reviews the proposed treatment and issues a pre-determination of benefits. While not a guarantee of payment, it confirms coverage before you incur the expense.

Author: Daniel Mercer;

Source: ladylesliebelize.com

Not keeping copies of submitted documents leaves you helpless if the insurance company loses your claim. They'll ask you to resubmit, and without copies, you're back to square one. Photograph or scan everything before mailing.

Coordination of benefits errors occur when you have coverage through multiple plans—perhaps your own employer plan and your spouse's. You must indicate secondary coverage on claim forms. The primary insurer pays first, then you submit the EOB to the secondary insurer for additional reimbursement. Filing with both simultaneously causes confusion and delays.

Submitting claims for services received before your coverage effective date or during a lapse in coverage guarantees denial. Verify your coverage status before appointments, especially at the beginning of a new job or after open enrollment changes.

How to Maximize Your Dental Insurance Reimbursement

Timing your claims strategically can increase total reimbursement. If you're approaching your annual maximum in November and need additional work, consider scheduling it for January. This spreads the cost across two benefit years, giving you access to two annual maximums instead of exhausting one.

File claims promptly after service. The sooner you submit, the sooner you receive payment and can apply those funds to other expenses or pay down credit cards used for the initial payment. Waiting months to file means you've essentially given the insurance company an interest-free loan.

Author: Daniel Mercer;

Source: ladylesliebelize.com

When claims get denied, appeal immediately. Insurance companies deny claims for various reasons—some legitimate, others based on misunderstandings. Your dentist can provide additional documentation supporting medical necessity. Appeal letters should be specific, citing your plan's policy language and including supporting clinical evidence.

Track all reimbursements against your annual maximum. Create a simple spreadsheet logging each claim's date, procedure, amount paid by insurance, and remaining maximum. This prevents surprise denials when you think you have coverage remaining but have actually exhausted your benefits.

Use Health Savings Accounts (HSA) or Flexible Spending Accounts (FSA) to pay your dentist initially. These pre-tax dollars reduce your effective cost. When you receive your reimbursement check, you can replenish your HSA or use the funds for other purposes, depending on your account type and plan rules.

Request itemized treatment plans before major work begins. Review these with your insurance company's customer service department to understand exactly what will be covered. Some procedures have multiple coding options, and choosing the right code can mean the difference between coverage and denial.

Consider dental discount plans if you frequently use out-of-network providers. These aren't insurance but offer reduced fees at participating dentists. You might pay less with the discount than you would after reimbursement from insurance, especially for major work.

Frequently Asked Questions About Dental Insurance Reimbursement

Dental insurance reimbursement requires more active participation than direct billing arrangements, but understanding the process puts you in control of your dental care finances. The model works best when you treat it like any other financial transaction—keep detailed records, meet deadlines, and don't hesitate to question denials or discrepancies.

The key to successful reimbursement lies in preparation. Before your dental appointment, verify your coverage details and filing requirements. After your appointment, organize your documentation immediately rather than letting receipts pile up. When you submit claims, track them actively rather than passively waiting for checks to arrive.

Remember that insurance companies are businesses managing risk and costs. They won't automatically pay every claim at the highest possible rate. You must advocate for yourself, ensuring claims are coded correctly, documented thoroughly, and filed properly. When you understand how reimbursement percentages, UCR rates, and annual maximums interact, you can make informed decisions about when and where to receive dental care.

The reimbursement model offers flexibility that direct billing sometimes doesn't—you can choose any dentist regardless of network status and access care immediately without waiting for insurance approvals. The trade-off is upfront cost and administrative effort. For many patients, especially those who value provider choice over convenience, this trade-off makes perfect sense.

Your dental health shouldn't suffer because insurance processes seem complicated. Armed with knowledge about how reimbursement works, what documentation you need, and how to avoid common mistakes, you can confidently navigate the system and receive the benefits you've paid for through your premiums.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.