Dental Insurance

Dental Insurance No Waiting Period Guide

You wake up with a throbbing toothache. Your dentist says you need a crown and root canal—$2,500 worth of work. You finally decide to buy dental insurance, only to discover most plans won't cover that crown for another six to twelve months. That's where no waiting period dental insurance changes everything.

Traditional dental coverage makes you wait. Three months before they'll pay for a filling. Six months before a crown gets covered. Sometimes a full year before major procedures receive any benefits. Meanwhile, you're stuck with the pain, the problem gets worse, and you end up paying out of pocket anyway.

Plans that eliminate these waiting periods let you walk into the dentist's office next week with full coverage active. But they're not magic—you'll pay for that convenience somehow. Understanding exactly what you're getting (and giving up) helps you avoid expensive mistakes.

What Is Dental Insurance No Waiting Period

Dental insurance no waiting period meaning: Your benefits activate immediately when your policy starts. No three-month countdown for fillings. No six-month delay for root canals. Coverage begins on day one for everything the plan covers.

Here's how traditional plans work: You enroll in January. They'll cover your cleaning right away (every plan does that). But need a filling? Wait until April. Crown? See you in July. Root canal? Maybe next January if you're lucky. Preventive stuff starts immediately everywhere—cleanings, exams, X-rays—but actual treatment gets delayed for months.

What is dental insurance no waiting period in practical terms? It's coverage that treats you like you've already been enrolled for a year. Schedule that root canal next Tuesday. Get the crown prepped next Friday. The insurance company pays their percentage immediately instead of making you wait.

Why do these plans exist? Insurance companies normally use waiting periods to stop "adverse selection"—that's industry speak for people buying coverage only when they know they need expensive work. Someone with a broken tooth enrolls, gets their crown, then cancels. The insurer loses money. Waiting periods prevent this.

No waiting period plans take a different approach. They accept the risk but protect themselves through higher premiums, lower annual maximums, or clauses that exclude problems you already had when you enrolled. You get instant access. They get financial safeguards.

I see patients every week who put off treatment because they're waiting for coverage to kick in. A small cavity becomes a root canal. Gum disease progresses to bone loss. No waiting period plans work beautifully for people who need care now and understand they're paying slightly more for that immediacy

— Sarah Mitchell

The biggest difference from regular insurance? Risk timing. Standard plans assume you'll stay enrolled for years, spreading risk over time. Immediate coverage plans assume some members will use benefits heavily right away, so they build in protections upfront.

How Dental Insurance No Waiting Period Works

How does dental insurance no waiting period work once you actually sign up? You'll complete enrollment through your employer, the insurance marketplace, or directly with an insurer. Pick your plan, pay the first premium, and wait for your start date.

Here's what happens next: Most plans activate on the first of the month after you enroll and pay. Enroll on March 15th, pay your premium, and you're covered starting April 1st. Some employer plans sync with hire dates or use different schedules—check your specific effective date.

Author: Tyler Grant;

Source: ladylesliebelize.com

April 1st arrives. You can now book any covered service. Root canal? Call your dentist. Crown? Schedule it. Multiple fillings? Get them all done. Present your insurance card (or just your policy number if the card hasn't arrived yet), and the dentist's office verifies active coverage in their system.

The office submits the claim. Insurance pays their percentage based on your plan—maybe 50% for major work, 80% for basic procedures. You pay the rest plus any deductible you haven't met.

Eligibility varies widely. Employer plans typically require full-time status or a minimum number of hours per week. Individual marketplace plans might limit enrollment to specific periods, though some insurers sell year-round with coverage starting the following month. Geographic restrictions matter too—you'll need to live or work in areas where the network operates.

The pre-existing condition angle deserves attention. You enroll with a visibly cracked tooth. The insurer can see from your dentist's records (or will discover during your first exam) that this problem existed before coverage started. They'll often exclude that specific tooth from major procedure coverage for six to twelve months. Everything else? Covered immediately. New problems that develop after April 1st? Fully covered.

Watch out for misleading marketing. Some plans claim "no waiting periods" but only mean preventive and basic work start immediately—major procedures still require waiting. Genuine no waiting period coverage means every category (preventive, basic, major) works from day one, though pre-existing exclusions can still apply to individual teeth or conditions.

What Does Dental Insurance No Waiting Period Cover

What does dental insurance no waiting period cover when you actually need treatment? Dental plans divide services into three buckets, each with different coverage levels.

Preventive Services Coverage

Preventive work includes routine exams, professional cleanings, fluoride treatments for kids, X-rays, and sealants. Nearly every dental plan—traditional or immediate coverage—pays 100% for preventive care with zero waiting time. That's industry standard.

Your plan activates April 1st. Schedule a cleaning for April 5th. Walk in, get your teeth cleaned, walk out. Zero copay at most in-network dentists. This category offers no advantage for no waiting period plans because traditional plans already cover it immediately.

Most policies allow two cleanings per year, two routine exams, and one set of X-rays annually. Children often get additional fluoride treatments and sealants included. These limits apply regardless of plan type.

Basic Procedures Coverage

Basic procedures fix common dental problems: fillings for cavities, simple tooth extractions, scaling and root planing for gum disease, emergency treatment for pain. Traditional dental insurance makes you wait three to six months before covering any of this.

No waiting period plans skip that delay. Need a filling April 5th? They'll cover it—usually 70% to 80% after you meet your deductible. Most deductibles run $50 per person, so you'd pay $50 plus 20-30% of the filling cost.

Author: Tyler Grant;

Source: ladylesliebelize.com

This category makes the biggest practical difference. Someone who's been avoiding the dentist for years might have five cavities. Waiting six months means those cavities grow larger, potentially requiring crowns instead of fillings. Immediate basic coverage lets you fix problems while they're still small and cheap.

Major Procedures Coverage

Major work costs serious money: crowns, bridges, dentures, root canals, implants (when covered), periodontal surgery. Traditional plans impose six to twelve-month waiting periods. Many people specifically seek no waiting period insurance to avoid these delays.

Dental insurance no waiting period coverage explained for major procedures: You can schedule a root canal or crown installation the week your coverage starts. Plans typically pay 50% of costs after your deductible. A $1,200 crown means you pay your $50 deductible plus $600 (50% of the remaining $1,150).

The catch shows up in two places. First, annual maximums on these plans often cap at $1,000 to $1,500 instead of the $2,000 to $2,500 you'd see on traditional coverage. Need that crown plus a root canal plus two fillings? You might hit your annual limit fast, leaving you paying full price for anything beyond that.

Second, pre-existing condition clauses target major work. Enroll with a broken tooth visible in your mouth? That specific tooth might be excluded from crown coverage for the first year. Meanwhile, if a different tooth breaks next month, they'll cover it immediately.

| Feature | Traditional Dental Insurance | No Waiting Period Plans |

| Preventive care waiting period | None—starts immediately | None—starts immediately |

| Basic procedures waiting period | Usually 3-6 months | None—starts immediately |

| Major procedures waiting period | Usually 6-12 months | None—starts immediately |

| Typical monthly premium | Individual: $25-$50 | Individual: $35-$60 |

| Annual maximum | Often $1,500-$2,500 | Often $1,000-$1,500 |

| Pre-existing condition clauses | Uncommon | Very common |

| Best for | Healthy teeth needing maintenance only | People who need treatment soon |

Who Should Consider Dental Insurance Without Waiting Periods

Certain situations make immediate coverage worth the extra cost. Others? You're throwing money away.

People with dental pain right now benefit most. You've got a cracked tooth, a throbbing nerve, or obvious decay. Scheduling treatment immediately beats waiting six months while the problem worsens. Paying $15 extra per month for six months ($90) plus your 50% coinsurance costs less than paying full price for procedures.

Job switchers face coverage gaps. You leave an employer with dental benefits. COBRA costs a fortune. Individual traditional plans make you wait months for real coverage. A no waiting period plan bridges that gap, protecting you during the transition.

Author: Tyler Grant;

Source: ladylesliebelize.com

People who've delayed care for years often need several procedures done. You finally commit to fixing your teeth—why wait another year after procrastinating for five? These plans let you start treatment now instead of watching small problems become expensive emergencies.

Families with active kids avoid nasty surprises. Your daughter cracks a tooth skateboarding. Your son develops sudden cavities. Kids need treatment quickly—their teeth are still developing. Waiting periods feel particularly cruel when dealing with children's dental emergencies.

Who should avoid these plans? People with healthy teeth who mainly need cleanings. Since preventive care starts immediately everywhere, you're paying extra for major procedure coverage you won't use. That's like buying flood insurance in the desert.

Young adults with no dental issues and no family history of problems usually save money with traditional plans. Lower premiums for years outweigh the benefit of instant major procedure coverage you probably won't need.

Costs and Limitations of No Waiting Period Plans

Immediate coverage costs extra. Expect to pay $10 to $20 more monthly compared to traditional plans with similar benefits. Individual coverage might run $35 to $60 monthly instead of $25 to $45. Family plans? Figure $100 to $150 monthly compared to $75 to $120 for traditional coverage.

That premium difference adds up. Over a year, you're spending an extra $120 to $240 for the privilege of immediate access. Run the math on your specific situation to see if it's worth it.

Annual maximums create the biggest limitation. Many immediate coverage plans cap benefits at $1,000 to $1,500 yearly. Traditional plans often provide $1,500 to $2,500 annual maximums. Need extensive work? You'll hit that ceiling fast.

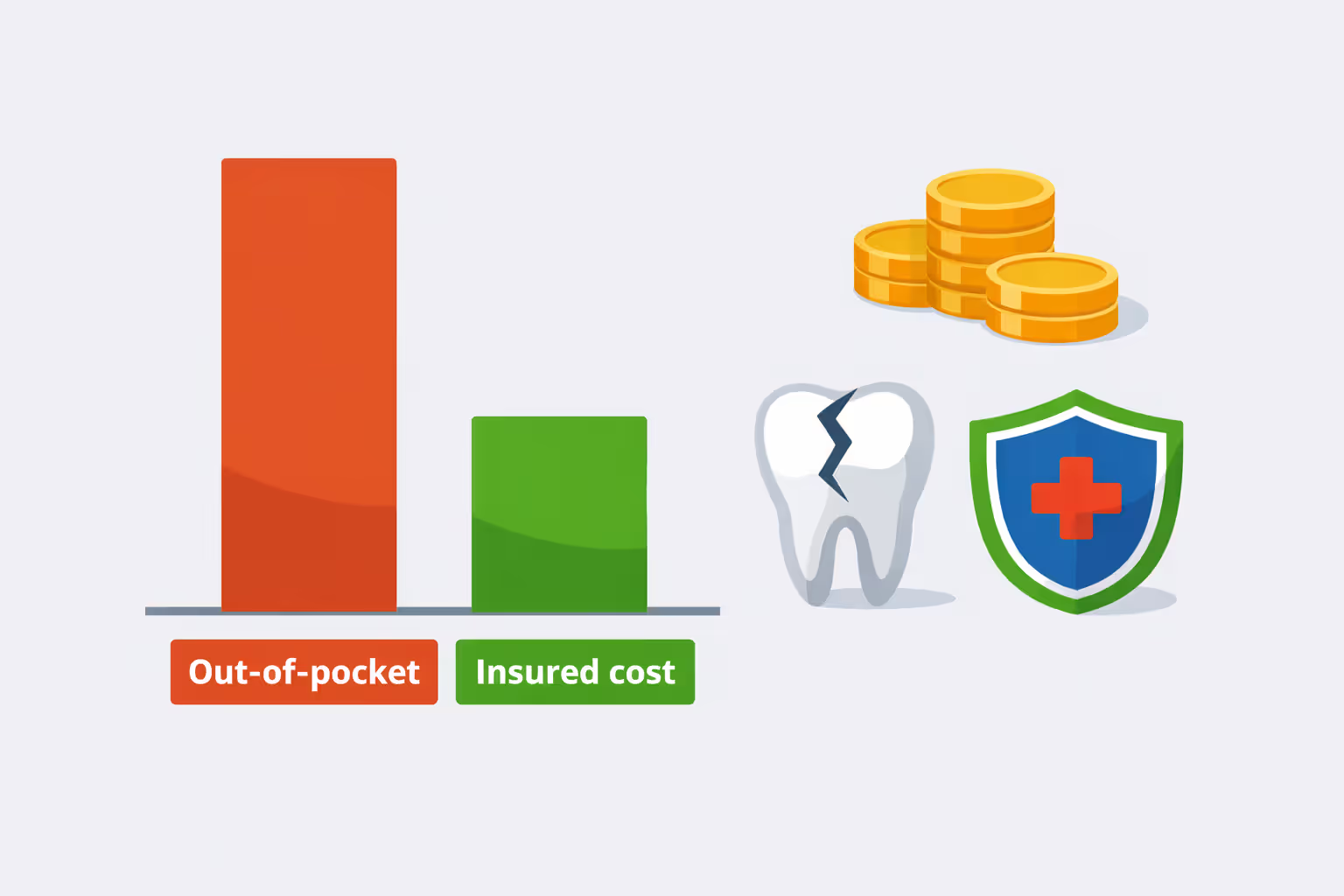

Example: You need two crowns ($2,400) and a root canal ($1,200). Total: $3,600 in dental work. Your plan covers 50% with a $1,500 annual maximum. Insurance pays $1,500. You pay $2,100 out of pocket. A traditional plan with a $2,500 maximum would leave you paying $1,100—saving you $1,000 despite the waiting period.

Author: Tyler Grant;

Source: ladylesliebelize.com

Pre-existing condition clauses appear frequently in these plans. You enroll with obvious dental problems visible to any dentist. The insurer may exclude those specific conditions from coverage for six to twelve months. New problems developing after enrollment? Fully covered. Existing issues? You'll wait anyway.

How they determine "pre-existing": The condition must be diagnosable before your coverage started. A dentist's examination or X-ray from before enrollment showing decay, cracks, or disease triggers the exclusion. Problems developing after your effective date don't count as pre-existing.

Network restrictions sometimes get tighter on no waiting period plans. Your provider options might shrink compared to traditional coverage. Some plans limit you to specific dentists in smaller networks. Out-of-network care might not be covered at all, or covered at significantly reduced rates like 30% instead of 50%.

Before enrolling, verify your current dentist participates. Call their office and confirm they accept the specific plan you're considering. If they don't participate, you'll need to find an acceptable in-network dentist near your home or office.

Common exclusions affect most plans: cosmetic procedures (whitening, veneers for appearance), orthodontics or limited braces coverage, dental implants, treatment for injuries (which your medical insurance might cover instead). Some plans won't cover wisdom tooth extraction unless the teeth are impacted.

Real-world cost comparison: You need one crown immediately. No waiting period plan costs $50 monthly. You pay for six months ($300) plus 50% of a $1,200 crown ($600). Total: $900. Paying full price for the crown without insurance: $1,200. You save $300 by having the plan.

But if you don't need that crown? You've paid $600 yearly in premiums for coverage you didn't use. A traditional plan at $35 monthly costs $420 yearly—you'd save $180 by choosing traditional coverage.

How to Choose a No Waiting Period Dental Plan

Choosing the right plan means comparing features that actually affect what you'll pay when you need care. Don't just pick the cheapest premium or the first plan you find.

Start by listing dental work you anticipate needing this year. Be honest. Do you need two crowns and a root canal? Just routine cleanings? Several fillings? Your anticipated needs determine which plan features matter most.

Coverage percentages vary between plans. One insurer might cover major procedures at 50%. Another offers 60%. That 10% difference on a $1,200 crown equals $120 in your pocket. Check the complete breakdown: preventive at what percentage, basic procedures at what level, major work at what rate.

Annual maximums deserve careful attention. Will a $1,000 cap cover your needs? Calculate: You need $3,000 in dental work. Even with 50% coverage, you'd expect to pay $1,500. But the plan only pays $1,000 maximum, leaving you covering $2,000. A plan with a $1,500 maximum reduces your cost to $1,750—a $250 difference.

Monthly premiums must fit your budget, but the lowest premium isn't always cheapest overall. A plan costing $10 less monthly but offering a $500 lower annual maximum might cost you hundreds more when you actually need work done.

Provider networks determine convenience and savings. Confirm your dentist participates before enrolling. Many insurance companies offer online provider search tools—but don't trust them completely. Call the dentist's office directly and verify they accept the specific plan you're considering. Networks change, and online directories lag behind.

| Feature | Why It Matters | What to Look For |

| Annual maximum | Caps total yearly benefits | $1,500+ if you need extensive work; $1,000 works for minimal needs |

| Coverage percentages | Controls your out-of-pocket costs | Preventive 100%, Basic 80%, Major 50-60% ideal |

| Monthly premium | Your recurring cost regardless of usage | Balance against maximum and coverage levels—not just cheapest |

| Deductible | What you pay before coverage starts | $50 or less preferred; some waive deductibles for preventive care |

| Provider network | Determines which dentists you can visit | Verify your preferred dentist accepts it or find quality in-network options nearby |

| Pre-existing condition clause | Might exclude known problems from immediate coverage | Understand specific exclusions for current dental issues |

| Waiting period details | Confirms actual immediate coverage | Verify preventive, basic, AND major all covered from day one |

Read the policy documents—specifically the Schedule of Benefits and any language about pre-existing conditions. Some plans advertise "no waiting periods" but hide exceptions in footnotes. One plan might truly cover everything immediately. Another only eliminates waits for preventive and basic work.

Call the insurance company with specific questions about procedures you need. Don't rely on sales materials. Ask: "If I need a crown on April 15th and my coverage starts April 1st, will you cover it? What percentage? Does my $50 deductible apply? Is there a pre-existing condition review?"

PPO versus HMO structure affects flexibility. PPOs let you choose any participating dentist and often cover out-of-network care at reduced rates. You might get 60% coverage in-network, 40% out-of-network. HMOs require selecting a primary dentist and getting referrals for specialists. They usually cost less but offer less freedom.

Look for red flags: annual maximums below $1,000, major procedure coverage below 50%, networks with very few dentists in your area, high deductibles ($100+), or vague language about pre-existing conditions.

Get quotes from multiple insurers. The same coverage level can cost significantly different amounts between companies. Three quotes gives you negotiating information and reveals the market rate.

Frequently Asked Questions

Dental insurance without waiting periods fixes a specific problem: the frustrating gap between needing treatment and being able to afford coverage. You're in pain now. Your tooth is broken today. Traditional waiting periods feel absurd when you're dealing with actual dental emergencies.

These plans work beautifully when you face immediate dental needs that would otherwise force you to pay full price or delay treatment for months while counting down waiting periods. They work poorly when you have healthy teeth and you're just looking for coverage "in case something happens."

Your decision depends on three factors: current dental health, anticipated needs in the next year, and your financial situation. Run the actual numbers. Calculate total cost of higher premiums plus your expected coinsurance. Compare that to either paying full price for procedures or choosing traditional coverage with lower premiums.

Real example: You need a crown immediately and two fillings within six months. No waiting period plan costs $50 monthly. You'll pay $300 in premiums for six months, plus $50 deductible, plus 50% of a $1,200 crown ($600), plus 20% of $400 in fillings ($80). Total: $1,030. Paying full price: $1,600. You save $570 by choosing immediate coverage.

Opposite scenario: You have healthy teeth and only need biannual cleanings. No waiting period plan costs $50 monthly ($600 yearly). Traditional plan costs $35 monthly ($420 yearly). You save $180 by choosing traditional coverage since cleanings are covered immediately on both.

Read policy documents thoroughly. Understand pre-existing condition language—exactly which situations trigger exclusions and for how long. Verify provider networks so you're not surprised when your dentist doesn't participate. Confirm annual maximums align with your anticipated needs.

The right plan provides financial protection exactly when you need it most, transforming a potential dental crisis from a $3,000 disaster into a manageable $1,500 expense. The wrong plan wastes money on coverage you'll never use. Choose based on your actual situation, not marketing hype.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.