Thoughtful middle-aged person sitting at kitchen table examining dental insurance documents while holding a complete denture in one hand

Dental Insurance That Covers Dentures With No Waiting Period

Here's the frustrating reality: you finally schedule that dentist appointment you've been putting off, and they tell you those cracked, painful teeth need to go. Full dentures. Problem is, when you call insurance companies, they say you'll need to wait 6-12 months before they'll cover anything. That's nearly a year of wincing through meals and avoiding photos.

But here's what most people don't realize—some coverage options let you skip that waiting game entirely. You just need to know where to look and what trade-offs you're making. Because yes, there's always a catch. Maybe higher monthly bills. Perhaps stricter limits on what they'll pay annually. Sometimes both.

This guide walks you through the real options for getting dentures covered fast, what they'll actually cost you, and whether keeping that insurance makes sense after your new teeth arrive.

How Dental Insurance Waiting Periods Work

Insurance companies aren't being cruel when they make you wait—they're protecting themselves from people who only buy coverage right before expensive procedures. Think about it from their perspective: if everyone could sign up Monday, get $3,000 dentures Tuesday, then cancel Wednesday, the whole system would collapse.

So they build in these delays. Here's how it typically breaks down:

Cleanings and X-rays? Usually covered immediately. You can book your first appointment next week.

Fillings and basic extractions? Three months, give or take. Not ideal, but manageable.

Dentures, crowns, bridges—the expensive stuff? Six months minimum. Often a full year. And that's 365 actual days from when your policy kicks in, not when you signed the paperwork.

One guy I know enrolled in February thinking he'd timed it perfectly for his July dentist appointment. Nope. His policy didn't activate until March 1st, which meant his waiting period ended September 1st. Two extra months of waiting because he didn't read the fine print about start dates.

Author: Daniel Mercer;

Source: ladylesliebelize.com

Different carriers calculate this differently too. Some start counting from your first premium payment. Others use the first day of the month after enrollment. A few even reset your waiting period if you let coverage lapse for more than 30 days, so you can't game the system by canceling and re-enrolling.

Now, dental insurance with no waiting period for dentures sidesteps all this headache. You're covered the moment your policy goes live. But—and this is important—insurers make up that risk somewhere else. Higher premiums. Lower yearly maximums. Sometimes both. They're not running a charity.

Types of Dental Insurance Plans That Cover Dentures Immediately

Discount Dental Plans vs. Traditional Insurance

Let's clear up some confusion right away: discount dental plans aren't actually insurance. They're membership clubs. You pay maybe $100-$180 yearly, get a card, and that card gets you 20-50% off at participating dentists. No waiting periods. No claim forms. Just discounted prices.

Sounds great, right? Here's the catch—you're still paying the entire bill yourself, just less of it.

Example: Full dentures normally run $2,400 at your local prosthodontist. Your discount card gets you 35% off. That's $1,560. Still due in full at treatment time. Got $1,560 sitting in your checking account? Great, this works. Don't have it? Well, you're stuck.

Compare that to actual insurance. Yes, you'll probably wait months before coverage kicks in if you buy a standard plan. But once it does, they're paying their share—typically 50% after you meet your deductible. On that same $2,400 denture, you'd pay around $1,200-$1,300 depending on your specific policy details.

The real unicorn? Traditional insurance that waives waiting periods. A few companies offer this, but expect to pay $65-$95 monthly instead of the usual $35-$55. Over twelve months, that extra $30-$40 per month adds up to $360-$480 extra you're spending for immediate access.

Some insurers waive waiting periods if you're switching from another dental policy without any gap in coverage. Leaving your job but COBRA-ing your dental? You might qualify for immediate coverage elsewhere. Just lost your spouse's coverage through divorce? Same deal—special enrollment might get you in without delays.

Medicare Advantage Plans With Dental Benefits

Regular Medicare won't touch dentures. Part A covers hospital stays. Part B handles doctor visits and outpatient care. Dentistry? Not their problem—unless you're in a car accident and need jaw reconstruction or something equally dramatic.

Medicare Advantage flips this script. About 9 out of 10 Medicare Advantage plans now include dental coverage. But—big but here—"dental coverage" ranges from basically useless to genuinely helpful.

Some plans cover two free cleanings yearly and that's it. Zero help with dentures.

Better plans kick in $1,000-$2,500 yearly for major work like dentures, covering around 50% of costs after a short waiting period. We're talking 90 days, maybe six months. Way better than the year-long wait with regular insurance.

The best plans (which cost more, naturally) eliminate waiting periods entirely. You're in a network of approved dentists, but if you're okay with that restriction, you can start treatment almost immediately after your plan activates.

Qualifying requires hitting 65 or meeting disability requirements. You'll need to live within the plan's service area too—these aren't nationwide blanket policies. Enrollment happens during that October 15 to December 7 window everyone talks about, with coverage starting January 1st.

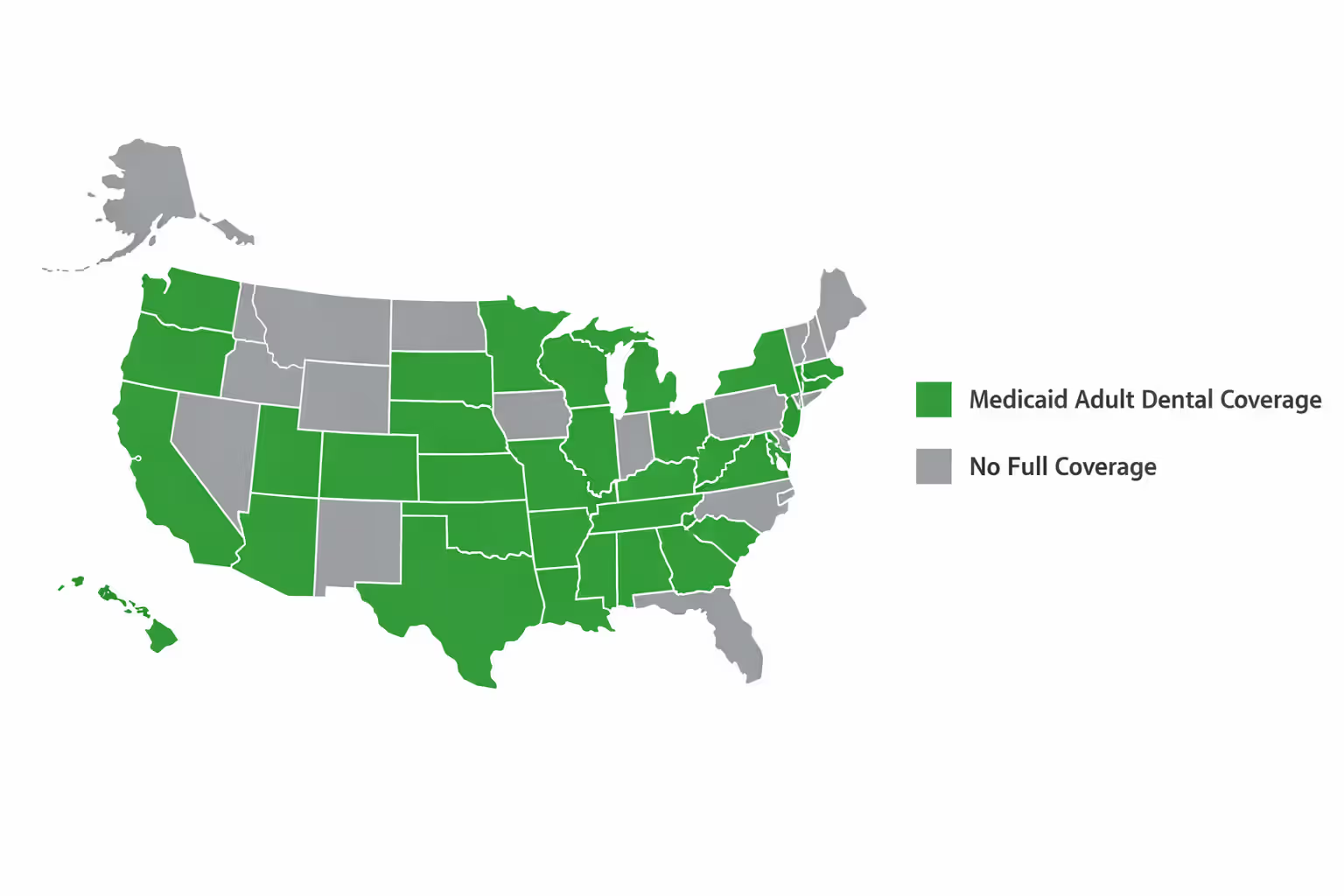

Medicaid Denture Coverage by State

This is where things get wildly inconsistent. Federal law requires states to provide comprehensive dental care to kids on Medicaid. Adults? Totally optional. Each state decides.

California's Medicaid (Medi-Cal) covers complete and partial dentures without waiting periods once you're enrolled. Same with New York and Illinois—pretty comprehensive adult dental benefits.

Florida? Texas? Alabama? Good luck. Emergency-only coverage in many cases, and dentures often don't qualify unless you can prove medical necessity—like cancer treatment destroyed your jaw or a car crash knocked out all your teeth.

Right now, roughly 35 states offer at least some denture coverage for Medicaid adults. "Some coverage" is doing heavy lifting in that sentence though. Might be full coverage. Might be partial. Might be "we'll cover the cheapest option available and you're on your own if you want anything better."

Income limits typically max out around 138% of federal poverty level in expansion states. Non-expansion states set much lower thresholds, sometimes below 50% of poverty level. Parents with kids at home often qualify more easily than childless adults, even at identical income levels.

Application processing takes weeks, but here's the useful part: once approved, your coverage can backdate up to three months. So if you apply in May and get approved in June, your coverage might actually start in March—meaning any treatment you received in March, April, or May could be covered retroactively. Effectively eliminates waiting periods if you time it right.

Author: Daniel Mercer;

Source: ladylesliebelize.com

What Denture Procedures Are Typically Covered

When your dentist says "you need dentures," that's actually code for a bunch of separate procedures. And insurance treats each one differently. Let's break down what you're really looking at.

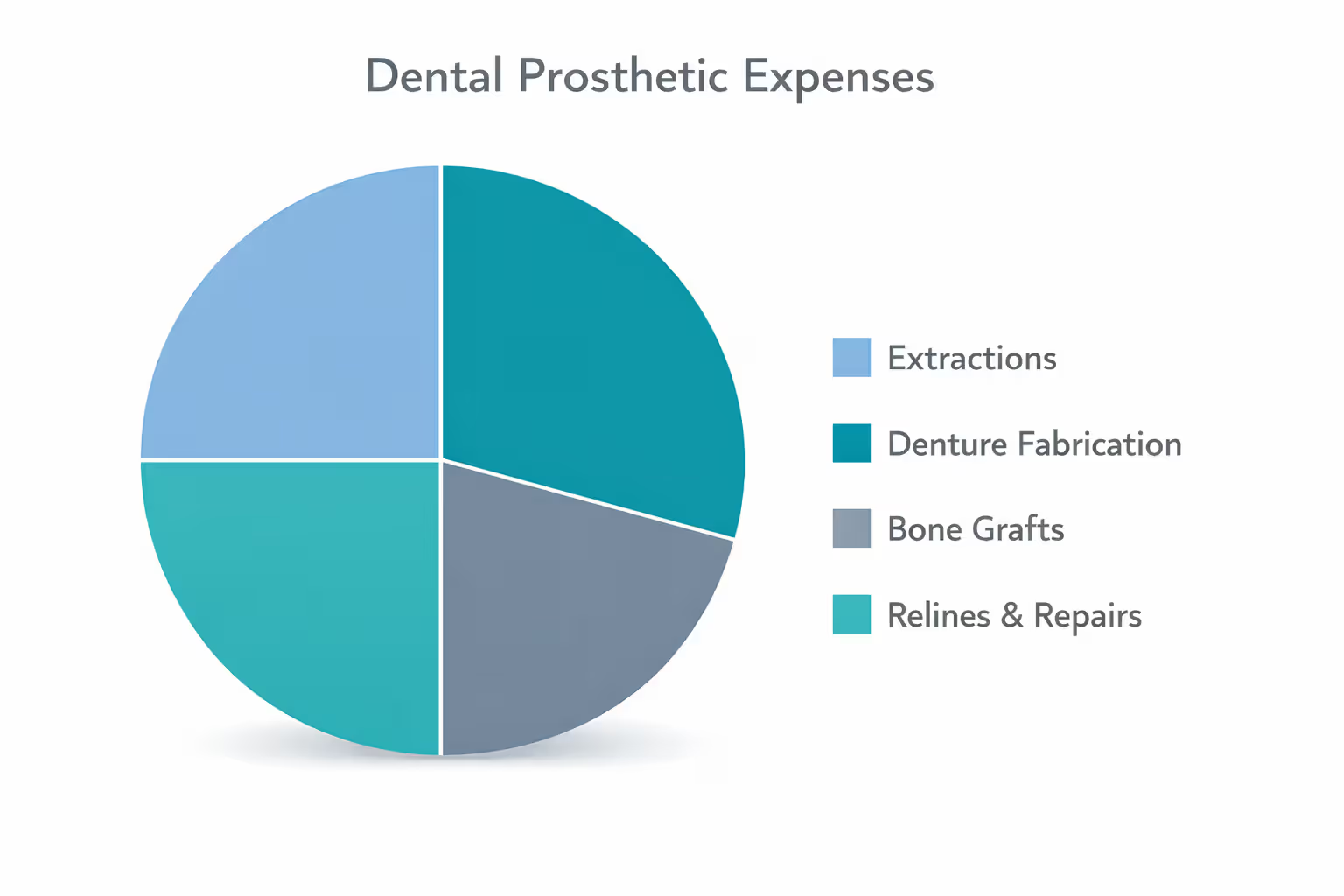

Getting teeth pulled: Most plans that cover dentures will also cover the extractions—they kind of have to, unless they expect you to yank them yourself. Simple extractions where the tooth comes out cleanly? Usually 70-80% covered. Surgical extractions where they're digging out broken roots or impacted teeth? Drops to 50% because they classify it as oral surgery.

Now here's where it gets expensive. Some people need bone grafts or ridge modifications to build up their jaw before dentures will fit properly. Insurance views this as "optional enhancement" most of the time. You're paying full price, maybe $800-$2,000, even with good coverage.

Full sets versus partial dentures: Both typically fall under "major services" at 50% coverage. The difference shows up in your final bill. Full dentures run $1,300-$3,000 per arch (and you might need both upper and lower). Partials cost less, maybe $700-$1,800, because they're replacing fewer teeth and using your remaining natural teeth for support.

Insurance processes upper and lower dentures as two separate procedures. Need both? That's two separate claims eating into your annual maximum. If your policy maxes out at $1,500 yearly and each arch costs $2,000, you're looking at serious out-of-pocket expenses.

The implant question: Does dental insurance cover anchored dentures? Short answer—maybe the denture part, definitely not the implant part.

Here's how this usually plays out: Regular removable dentures get standard 50% coverage. But implant-supported overdentures? Insurance companies say those titanium posts screwed into your jaw are "cosmetic." Never mind that they prevent bone loss and let you actually chew food properly. You're paying $1,800-$3,500 per implant out of pocket.

Some policies will cover the snap-in denture attachment that connects to those implants at the usual 50% rate. So you pay full price for the foundation, get half-off on the house. Makes total sense, right?

A handful of premium policies marketed to seniors include partial implant coverage—maybe $500-$1,000 per post. Monthly premiums on these plans? Often $80-$120, compared to $35-$55 for standard coverage.

Adjustments and repairs: Your gums shrink over time. Bone resorbs. Dentures that fit perfectly today will feel loose in 18 months. Most policies cover relines (adding material to restore proper fit) once every two years at 50%. Repairs when you drop them and crack the base or break a clasp? Usually 50-80% covered.

Those first few adjustments after getting new dentures—tightening a spot that rubs, smoothing a rough edge—typically get bundled into the original fabrication fee. But two years later when you need a major reline? That's a separate $300-$500 procedure where you're paying half.

Understanding dental insurance for extractions and dentures means tracking how each procedure counts against your annual maximum. Get $800 in extractions done in June, and you've only got $700 left of a $1,500 maximum for the actual dentures later that year.

Author: Daniel Mercer;

Source: ladylesliebelize.com

How to Find Low-Cost Dental Insurance for Dentures

Shopping for dental insurance isn't like buying car insurance where you compare five quotes and pick the cheapest. The lowest premium often leaves you paying more in the long run. Here's how to actually find dental insurance that pays for dentures without getting ripped off.

Check your employer first. If your company offers dental benefits, that's probably your best bet. Group plans frequently waive waiting periods or cut them to three months. Plus your employer's picking up part of the tab—you might pay $15-$25 monthly instead of $45-$75 for similar individual coverage.

Even if you're six months from retirement and know you'll need dentures soon, staying on your employer plan through the transition beats buying individual coverage with a new waiting period. COBRA's expensive for medical, but dental COBRA often runs just $30-$50 monthly.

Browse Healthcare.gov and state exchanges. These don't bundle dental with medical plans anymore, but many states sell standalone dental insurance through the same marketplace. Makes comparison shopping easier since everything's standardized. Subsidies for dental are rare—not like the tax credits for medical coverage—but occasionally available for lower-income families.

Get quotes from direct-to-consumer carriers. Companies like Delta Dental, Cigna, Humana, and Guardian sell directly to individuals. Pull quotes from at least three, comparing these specific points:

Annual maximum: That $1,000-$2,000 yearly cap matters more than anything. Full dentures cost $1,300-$3,000. With a $1,000 maximum and 50% coverage, you're paying $1,500-$2,500 yourself even with insurance. A $2,000 maximum policy at $10 more monthly could save you hundreds.

Network restrictions: PPO plans let you see any dentist, but you'll pay less with in-network providers. HMO plans lock you into their network completely—no coverage at all for out-of-network care. HMOs cost less monthly but limit your options.

That reimbursement percentage: Standard is 50% for major work. Budget plans sometimes drop to 40%. On $2,400 dentures, that 10% difference costs you $240.

Look for promotional periods. Some carriers waive waiting periods for new members during specific enrollment windows—usually November through January, competing for the Medicare crowd. Others offer "continuous coverage credits" where your waiting period from your old insurance transfers to your new policy. Switching from Carrier A to Carrier B? If you had coverage for seven months with Carrier A and Carrier B has a six-month waiting period, you're covered immediately.

Consider dental schools. Not insurance, but worth mentioning. Dental students need real patients to practice on under faculty supervision. Dentures at dental schools typically cost 40-60% less than private practice—maybe $800-$1,400 for a full set instead of $2,000-$3,000. Appointments take longer and scheduling's less flexible, but if you're paying cash either way, this beats paying full retail.

Research studies testing new denture materials occasionally offer free or deeply discounted dentures. Universities with dental research programs post these opportunities. You're essentially a test subject, which sounds scarier than it is—everything's IRB-approved and closely monitored.

Author: Daniel Mercer;

Source: ladylesliebelize.com

When you're reading policy documents (actually read them—don't just trust the sales pitch), look for "prosthodontics" in the coverage schedule. That's the technical term for dentures and related appliances. If you don't see it listed, ask specifically before buying.

Common Coverage Limitations and Out-of-Pocket Costs

Does dental insurance pay for dentures in full? Almost never. Even "comprehensive" coverage leaves you with significant bills. Here's what you're really paying.

Annual maximums kill you on expensive procedures. Most policies cap benefits at $1,000-$1,500 yearly. A few generous ones go up to $2,000. Sounds reasonable until you price dentures.

Let's walk through actual math. Your policy has a $1,500 annual max and covers 50% of major procedures. Dentures cost $2,400.

Without the maximum, you'd pay: $2,400 × 50% = $1,200

With the maximum, insurance pays their share UNTIL hitting that $1,500 cap. Since 50% of $2,400 is $1,200, you're under the limit. You pay $1,200.

But what if you needed $600 in extractions earlier that year? Now you've used $300 of your annual maximum already. Only $1,200 remains for dentures. Even though 50% coverage should give you $1,200 off your $2,400 dentures, you only get $1,200 because that's your remaining maximum. You're paying $1,200 out-of-pocket instead of the $1,200 you expected. Wait, same number—bad example.

Better example: Same scenario but dentures cost $3,200. You'd expect to pay 50%, which is $1,600. But you've used $300 of your annual maximum. You get $1,200 coverage, pay $2,000 yourself.

Deductibles hit first. Before insurance pays anything, you're covering that deductible. Usually $50-$100 per person annually. Some policies waive it for preventive care but apply it to major work. On a $2,000 denture with $50 deductible and 50% coinsurance: You pay $50 + ($1,950 × 50%) = $1,025.

Replacement limits frustrate people. Insurance will pay for new dentures once every 5-8 years, period. Seven years is most common. Lose them? Drop them in the toilet? Sit on them? Too bad. Unless you can prove an accident or significant medical changes (major weight loss/gain, cancer treatment affecting bone structure), you're paying full price for replacements before that 7-year window closes.

What insurance won't touch:

- Implant posts (that $6,000-$12,000 for four-implant overdentures is all you)

- Precision attachments for partials beyond basic clasps

- Cosmetic customization—want natural-looking characterization instead of generic chicklet teeth? Your dime

- Backup dentures (insurance covers one set, not two)

- Premium materials like flexible partial frameworks

Real-world costs break down like this:

With insurance: Complete dentures typically cost you $600-$1,500 out-of-pocket after coverage. Partials run $300-$900.

Without insurance: Complete dentures cost $1,300-$3,000. Partials cost $700-$1,800.

Geographic variation matters hugely. Rural Alabama? Lower end of those ranges. Manhattan? Double it.

| Plan Type | Waiting Period | What They Cover | Annual Max | Monthly Cost | Who This Fits |

| Discount Membership | None—immediate access | 15-50% fee reduction at member dentists | No limit (not insurance) | $8-$18 | People with cash in hand who need treatment now |

| Medicare Advantage with Dental | 0-6 months depending on plan | 50% of denture costs | $1,000-$2,500 | $0-$100 (varies by plan) | Anyone 65+ or qualifying disability |

| Medicaid (Participating States) | None after qualifying | Full coverage or small copay | Set by state rules | $0 | Income-qualified individuals in expansion states |

| No-Wait Individual PPO | None—immediate coverage | 50% of denture costs | $1,000-$1,500 | $60-$95 | People needing dentures within 6 months willing to pay more monthly |

| Standard Individual PPO | 6-12 months | 50% of denture costs | $1,000-$2,000 | $30-$55 | People planning ahead who want lower premiums |

Do You Still Need Dental Insurance After Getting Dentures

Lots of people cancel their dental coverage the minute they walk out with new dentures. "I've got fake teeth now—what do I need insurance for?" Seems logical. Sometimes it is. Often it isn't.

Do i need dental insurance if i have dentures depends entirely on your situation. Let's run the numbers.

Ongoing maintenance costs more than you think. Dentures need relines every 2-4 years as your gums shrink and jaw bone resorbs. Cost: $200-$500 per arch. Repairs when clasps break or teeth chip: $100-$300 per incident. Adjustments as your mouth changes: $50-$150.

Over ten years, you might spend $1,500-$3,000 maintaining your dentures. Seems like a lot, right?

Now compare insurance costs. You're paying $40 monthly—that's $480 yearly, $4,800 over ten years. Your insurance covers 50% of maintenance, saving you $750-$1,500. Net cost: $3,300-$4,050 MORE with insurance than without.

But wait—that insurance also covers:

- Yearly cancer screenings (oral cancer's no joke, especially for former smokers)

- Treatment for denture stomatitis, fungal infections, or tissue irritation

- Care for any remaining natural teeth if you wear partials

- Emergency repairs that might otherwise hit you with a $300 bill at the worst possible moment

Replacement timing matters. Dentures don't last forever. Seven to ten years is typical before they're worn out, stained beyond salvaging, or fit so poorly they're unusable. New dentures cost the same as the originals—$1,300-$3,000.

If you keep insurance continuously, there's no waiting period when replacement time arrives. Drop it now, decide you want coverage again in year six? You're waiting another 6-12 months before benefits kick in.

Quick math exercise:

Keeping coverage 5 years: ($45 monthly premium × 60 months) + (estimated $800 maintenance × 50% your share) = $2,700 + $400 = $3,100

No coverage 5 years: $800 maintenance fully out-of-pocket = $800

Keeping insurance costs you $2,300 more over five years. But if you need replacement dentures in year five at $2,400 each, insurance saves you $1,200, cutting your net loss to $1,100.

Who should keep coverage:

- People with partial dentures and remaining natural teeth needing maintenance

- Anyone with tight budgets who can't absorb surprise $300-$500 bills

- People in poor health with higher infection/complication risks

- Those approaching the 7-year replacement window

Who can safely drop it:

- Complete denture wearers with no remaining teeth

- Healthy people who can handle unexpected repair costs

- Those with $3,000+ saved for eventual replacement

Some folks split the difference—drop comprehensive coverage but keep a discount membership plan. Pay $120 yearly, get 20-30% off maintenance and repairs, no monthly premiums.

I see this mistake constantly in my practice. Someone gets dentures, feels great, cancels insurance immediately. Twenty months later they're in my office with a cracked denture base, needs repair urgently, can't afford the $380 bill. Dentures require consistent professional maintenance. Your jawbone shrinks faster than most people realize, especially in the first two years. Even basic coverage that pays half of reline procedures transforms what could be a financial crisis into a manageable copay

— Dr. Patricia Mendez

Frequently Asked Questions About Dental Insurance and Dentures

Finding the right dental insurance for dentures without waiting periods comes down to timing. Need dentures in the next six months? Paying extra for no-wait coverage or using discount plans makes financial sense. Can comfortably wait a year? Standard policies with waiting periods cost less long-term.

Do actual math on five-year costs including premiums, deductibles, coinsurance, and out-of-pocket maximums. Compare at least three different plan types—traditional insurance, Medicare Advantage if you qualify, discount memberships, and Medicaid if income-eligible.

Read actual policy documents. Not brochures. Not summaries. The real contract. Look specifically at the prosthodontics section for exact denture coverage language.

Lowest premium rarely equals best value. A plan charging $35 monthly with a $1,000 yearly maximum might ultimately cost you more than a $55 monthly plan with a $2,000 maximum when you factor in out-of-pocket expenses for extensive dental work.

Think beyond just dentures too. What about your other dental needs? Cleanings? Fillings? Treatment for gum disease? Evaluate your complete oral health situation when making coverage decisions.

Right coverage protects your health and finances simultaneously. You get necessary treatment without bankrupting yourself. Spending time now researching options prevents expensive mistakes and keeps you smiling confidently for years ahead.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on dental insurance topics, including coverage options, premiums, deductibles, waiting periods, annual maximums, claims processes, and procedures that may be covered by insurance such as implants, braces, crowns, dentures, and preventive care. The information presented should not be considered medical, dental, financial, or professional insurance advice.

All articles and explanations published on this website are for informational purposes only. Dental insurance policies may vary between providers, and details such as coverage limits, exclusions, reimbursement rates, waiting periods, and eligibility requirements can differ depending on the insurer, plan, and individual circumstances.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness or reliability of the content. Use of this website does not create a professional relationship. Visitors should review official policy documents and consult with licensed dental or insurance professionals before making decisions regarding dental care or insurance coverage.